by Jeff Miller

In last week's prediction for the week ahead I guessed that it would be "all about earnings. From a market perspective that was mostly accurate despite some competing stories: charges against SAC Capital, fresh speculation about the new Fed Chair, and the arrival of Prince George.

This week will be quite different with three distinct focal points:

- The FOMC announcement – continuing speculation about tapering of QE purchases;

- GDP news – which some will seize as evidence of recession; and

- Another big week for earnings announcements.

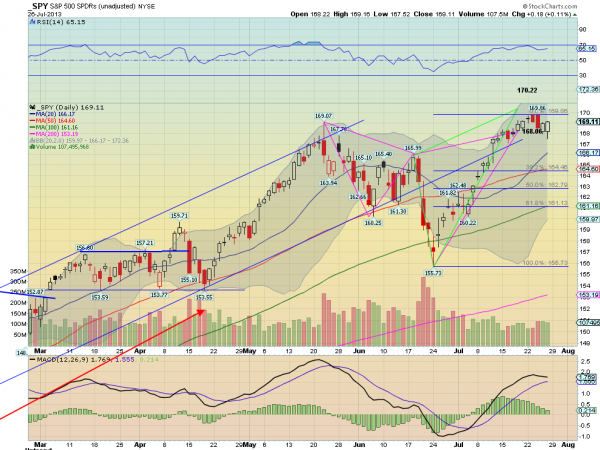

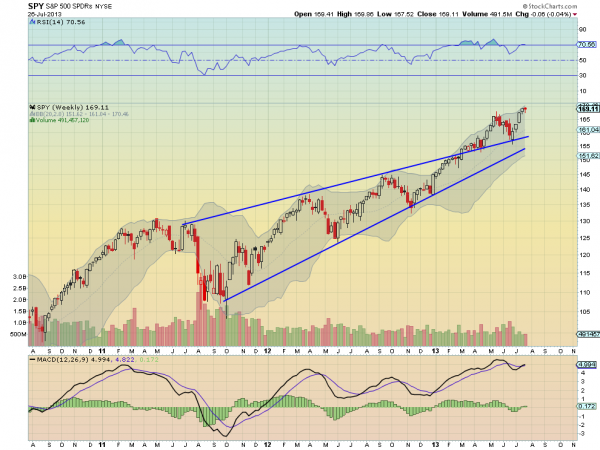

This occurs within a technical backdrop that could facilitate a stock market breakout in either direction. Charles Kirk has returned from his annual vacation and his weekly chart show (small annual subscription, and well worth it) shows the tendencies for each of several time frames. Regular readers know that I love this approach – helpful for almost everyone, but without oversimplifying the story. Charles sees resistance in the current consolidation range, but plenty of room to move if there is a breakout. Most would be surprised by the possible range, especially the next upside target (not what will happen, but what might happen.)

The end of July often starts a very quiet time. Even (!!) Congress will be taking off.

Unless the various factors point in different directions, we could have a surprisingly large move in stocks next week.

Are you ready for action?

I have some thoughts on preparing for next week which I will discuss further in the conclusion. First, let us do our regular update of last week's news and data.

Background on "Weighing the Week Ahead"

There are many good lists of upcoming events. One source I regularly follow is the weekly calendar from Investing.com. For best results you need to select the date range from the calendar displayed on the site. You will be rewarded with a comprehensive list of data and events from all over the world. It takes a little practice, but it is worth it.

In contrast, I highlight a smaller group of events. My theme is an expert guess about what we will be watching on TV and reading in the mainstream media. It is a focus on what I think is important for my trading and client portfolios. Each week I consider the upcoming calendar and the current market, predicting the main theme we should expect. This step is an important part of my trading preparation and planning. It takes more hours than you can imagine.

My record is pretty good. If you review the list of titles it looks like a history of market concerns. Wrong! The thing to note is that I highlighted each topic the week before it grabbed the attention. I find it useful to reflect on the key theme for the week ahead, and I hope you will as well.

This is unlike my other articles at "A Dash" where I develop a focused, logical argument with supporting data on a single theme. Here I am simply sharing my conclusions. Sometimes these are topics that I have already written about, and others are on my agenda. I am putting the news in context.

Readers often disagree with my conclusions. Do not be bashful. Join in and comment about what we should expect in the days ahead. This weekly piece emphasizes my opinions about what is really important and how to put the news in context. I have had great success with my approach, but feel free to disagree. That is what makes a market!

Last Week's Data

Each week I break down events into good and bad. Often there is "ugly" and on rare occasion something really good. My working definition of "good" has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially -- no politics.

- It is better than expectations.

The Good

This was a pretty good week for news and data.

- Voters want more compromise from Congress. While poll results have a partisan flavor, the message seems more important for Republicans. Check it out via the interactive charts.

- The Europe story continues to improve. Frank Holmes of U.S. Global Investors cites three themes and also some stock ideas. His Europe economic surprise chart is below. Sober Look is not one for irrational exuberance, but cites a number of elements providing "glimmers of hope."

- Durable goods orders showed impressive growth. Steven Hansen at GEI takes a deep look at monthly changes, year-over-year changes, and inflation adjustments.

- The oil price spike might be ending, since the gap between WTI and Brent has been closed. (Via Christopher Swann at BreakingViews). (See also NDD at The Bonddad Blog where oil and gas prices are among the high frequency indicators that they track each week).

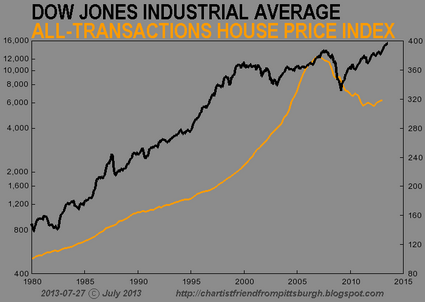

- New home sales were strong. Calculated Risk remains bullish on the housing story. A key distinction is between new and existing sales. Read the entire post, but the chart below illustrates the significance of the narrowing gap.

- Consumer confidence from the University of Michigan hit a post-recession high. Calculated Risk notes that the trend has been solidly upward except when "Congress threatened not to pay the bills in 2011. Doug Short's fine chart is the best for relating this to the overall economy:

The Bad

There was a little bad news. Feel free to add in the comments anything you think I missed!

The Noteworthy

Maria Bartiromo might be leaving CNBC. Fans will certainly be able to see her somewhere, but it is "no comment" all around so far.

Meredith Whitney states (during a CNBC interview, on the day of the publication of her op-ed in the FT, that she does not want media exposure.

The Indicator Snapshot

It is important to keep the current news in perspective. I am always searching for the best indicators for our weekly snapshot. I make changes when the evidence warrants. At the moment, my weekly snapshot includes these important summary indicators:

- For financial risk, the St. Louis Financial Stress Index.

- An updated analysis of recession probability from key sources.

- For market trends, the key measures from our "Felix" ETF model.

Financial Risk

The SLFSI reports with a one-week lag. This means that the reported values do not include last week's market action. The SLFSI has recently edged a bit higher, reflecting increased market volatility. It remains at historically low levels, well out of the trigger range of my pre-determined risk alarm. This is an excellent tool for managing risk objectively, and it has suggested the need for more caution. Before implementing this indicator our team did extensive research, discovering a "warning range" that deserves respect. We identified a reading of 1.1 or higher as a place to consider reducing positions.

The SLFSI is not a market-timing tool, since it does not attempt to predict how people will interpret events. It uses data, mostly from credit markets, to reach an objective risk assessment. The biggest profits come from going all-in when risk is high on this indicator, but so do the biggest losses.

Recession Odds

I feature the C-Score, a weekly interpretation of the best recession indicator I found, Bob Dieli's "aggregate spread." I have now added a series of videos, where Dr. Dieli explains the rationale for his indicator and how it applied in each recession since the 50's. I have organized this so that you can pick a particular recession and see the discussion for that case. Those who are skeptics about the method should start by reviewing the video for that recession. Anyone who spends some time with this will learn a great deal about the history of recessions from a veteran observer.

I have promised another installment on how I use Bob's information to improve investing. I hope to have that soon. Meanwhile, anyone watching the videos will quickly learn that the aggregate spread (and the C Score) provides an early warning. Bob also has a collection of coincident indicators and is always questioning his own methods.

James Picerno asks, Can the Fed Prevent the Next Recession? He interviews Bob for part of the answer, but also adds his own look at the data. He is asking the right questions in this thoughtful analysis.

I also feature RecessionAlert, which combines a variety of different methods, including the ECRI, in developing a Super Index. They offer a free sample report. Anyone following them over the last year would have had useful and profitable guidance on the economy. RecessionAlert has developed a comprehensive package of economic forecasting and market indicators, well worth your consideration.

Georg Vrba's four-input recession indicator is also benign. "Based on the historic patterns of the unemployment rate indicators prior to recessions one can reasonably conclude that the U.S. economy is not likely to go into recession anytime soon." Georg has other excellent indicators for stocks, bonds, and precious metals at iMarketSignals.

Unfortunately, and despite the inaccuracy of their forecast, the mainstream media features the ECRI. Doug Short has excellent continuing coverageof the ECRI recession prediction, now over 18 months old. Doug updates all of the official indicators used by the NBER and also has a helpful list of articles about recession forecasting. His latest comment points out that the public data series has not been helpful or consistent with the announced ECRI posture. Doug also continues to refresh the best chart update of the major indicators used by the NBER in recession dating. Here are his latest observations:

"Here are two significant developments since ECRI's public recession call on September 30, 2011:

- The S&P 500 is up 44.9%, hovering just below its most recent all-time high.

- The unemployment rate has dropped from 9.0% to 7.6%."

The average investor has lost track of this long ago, and that is unfortunate. The original ECRI claim and the supporting public data was expensive for many. The reason that I track this weekly, emphasizing the best methods, is that it is important for corporate earnings and for stock prices. It has been worth the effort for me, and for anyone reading each week.

Readers might also want to review my Recession Resource Page, which explains many of the concepts people get wrong.

Our "Felix" model is the basis for our "official" vote in the weekly Ticker Sense Blogger Sentiment Poll. We have a long public record for these positions. A few weeks ago we briefly switched to a bearish position, but it was a close call. Three weeks ago we switched back to neutral, which was also a close call. Last week Felix turned bullish, again by a small margin. The indicators are more positive this week.

These are one-month forecasts for the poll, but Felix has a three-week horizon. Felix's ratings have improved quite a bit. The penalty box percentage measures our confidence in the forecast. A high rating means that most ETFs are in the penalty box, so we have less confidence in the overall ratings. That measure remains somewhat elevated, so we have a bit less confidence in short-term trading.

[For more on the penalty box see this article. For more on the system ratings, you can write to etf at newarc dot com for our free report package or to be added to the (free) weekly ETF email list. You can also write personally to me with questions or comments, and I'll do my best to answer.]

The Week Ahead

This week brings plenty of data!

The "A List" includes the following:

- FOMC announcement (W). No policy change, but words will be parsed for hints about tapering.

- Employment report (F). People will speculate in advance that the Fed had the number on Wednesday.

- GDP for Q2 (W). All estimates have been reduced and there is also a major revision of past data. Briefing.com is forecasting a negative print!

- ISM index (Th). One of the best concurrent economic reads.

- Initial jobless claims (Th). Employment will continue as the focal point in evaluating the economy, and this is the most responsive indicator.

The "B List" includes the following:

- Conference Board sentiment (T). While I prefer the Michigan approach, the Conference Board method usually has a very similar results.

- Case-Shiller home prices (T). Slower than other sources but widely followed.

- ADP Employment data (W). A good estimate of private sector employment changes.

- Chicago PMI (W). Mostly interesting as the best guess for the national ISM number.

- Auto sales (Th). This is of special interest for overall consumption trends.

There are also several lesser reports – plenty to analyze. Also, after the announcement the "blackout" on Fedspeak will end, so speechifying will resume with Bullard on Friday.

But mostly – Earnings!

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a "one size fits all" approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has turned bullish and we are fully invested in trading accounts. The positions include USO (oil) as well as foreign and domestic equity ETFs. While we may well change holdings during the week, we expect to remain fully invested. Felix did well with a short bond position and also the USO trade (so far). The jury is out on the recent switch to a bullish posture. Felix did well to avoid the premature correction calls that have been prevalent since the first few days of 2013, accompanied by various slogans and omens.

Insight for Investors

The most important current theme for investors is what some call the "great rotation." I have called this a potential market turning point. The story continues, so my recent themes are still quite valid.

Josh Brown has a great post summarizing the data and calling the rotation "undeniable."

If you have not been following this section recently, please find a little time to give yourself a checkup. You can follow the steps below:

Let us start with the most dangerous investments, especially those traditionally regarded as safe. Interest rates have been falling for so long that investors in fixed income are accustomed to collecting both yield and capital appreciation. An increase in interest rates will prove very costly for these investments. It has already started.

- Find a safer source of yield: Take what the market is giving you!

For the conservative investor, you can buy stocks with a reasonable yield, attractive valuation, and a strong balance sheet. You can then sell near-term calls against your position and target returns close to 10%. The risk is far lower than for a general stock portfolio. This strategy has worked well for over two years and continues to do so. (I freely share how we do it and you can try it yourself. Follow here, and scroll to the bottom).

There is always risk. Investors often see a distorted balance of upside and downside, focusing too much on news events and not enough on earnings and value. You need to understand and accept normal market volatility, as I explain in this post: Should Investors be Scared Witless?

Too many long-term investors try to go all-in or all-out, thinking they can time the market. There is no reason for these extremes. There are many attractive stocks right now – great names in sectors that have lagged the market recovery. Ignore all of the talk about the Fed and focus on stocks.

And finally, we have collected some of our recent recommendations in a new investor resource page -- a starting point for the long-term investor. (Comments and suggestions welcome. I am trying to be helpful and I love feedback).

Final Thought

Each week I prepare for action by considering what might happen and how I plan to react. For our enhanced yield program we have some positions where we plan to sell calls on a rally. There are also new positions that would be more attractive to start on a dip. Either way, you can plan for the trade.

For long-term investors you should have a shopping list. When we get new accounts we implement long-term programs gradually. For those who have been in cash (or in poor holdings) you do not need to change everything on day one. Start by selling the worst positions and getting started with your "buy" list.

The most important story might be the GDP report. If it is weak enough, the recessionistas will be out in force. After a two-month absence, we might even see an appearance from the ECRI. None of the important economic data series signal recession, nor do any of my best sources. That will not stop the doomsters if the report is weak enough. Since there are new measurements involved, there will be plenty of spin potential.

Operating without a plan leaves you like a deer in the headlights. You will be unwilling to chase stocks higher on a rally and afraid to buy on a dip.

Volatility is the friend of the trader, but it can be the same for the long-term investor. It starts with having a plan for action.

See the original article >>