My Shadow

It's time to make a start

To get to know your heart Time to show your face Time to take your place In every speck of dust In every universe When you feel most alone You will not be alone Just shine a light on me Shine a light I'll shine a light on you Shine a light And you will see my shadow On every wall And you will see my footprints On every floor It only takes a spark To tear the world apart These tiny little things That make it all begin Just shine a light on me Shine a light I'll shine a light on you Shine a light And you will see my shadow On every wall And you will see my reflection In your freefall Ooooooooh Ooh ooh Ooooooooh Ooooh ooh Just shine a light on me Shine a light I'll shine a light on you Shine a light Cuz when your back's against the wall That's when you show no fear at all And when you're running out of time That's when you hitch your star to mine We won't be leaving by the same road That we came by We won't be leaving by the same road That we came by We won't be leaving by the same road That we came by We won't be leaving by the same road That we came by |

Thursday, September 11, 2014

Keane - My Shadow

Italy's Ferrari reports record first-half revenues

Rome (AFP) - A day after Ferrari said its head was leaving after more than two decades, the Italian sports car brand on Thursday posted record revenues in the first half of 2014.

Net profits jumped 9.8 percent in the first six months of the year to 127.6 million euros ($165.1 million), the luxury automaker said in a statement.

And revenue surged 14.5 percent from the same time a year ago to an "absolutely unprecedented" 1.35 billion euros, helped by higher sales in the US, Japan, Australia and Britain, it added.

"It is a huge satisfaction for all of us at Ferrari to continue to achieve record economic results," outgoing president Luca di Montezemolo said in the statement.

"I'm sure that in a few months we will close an extraordinary year without precedent."

Ferrari on Wednesday announced Montezemolo would step down in October after 23 years at the helm, just weeks before the company floats in the US as part of its parent group Fiat Chrysler.

The top job at the biggest name in Formula One racing will be taken over by the head of parent group Fiat, Sergio Marchionne.

The two men had clashed over strategy, with Montezemolo reportedly hoping to keep the brand exclusive by limiting sales to some 7,000 cars a year and Marchionne pushing for higher sales.

Ferrari said Thursday it sold 3,631 cars in the first half of 2014, down 3.6 percent from a year earlier.

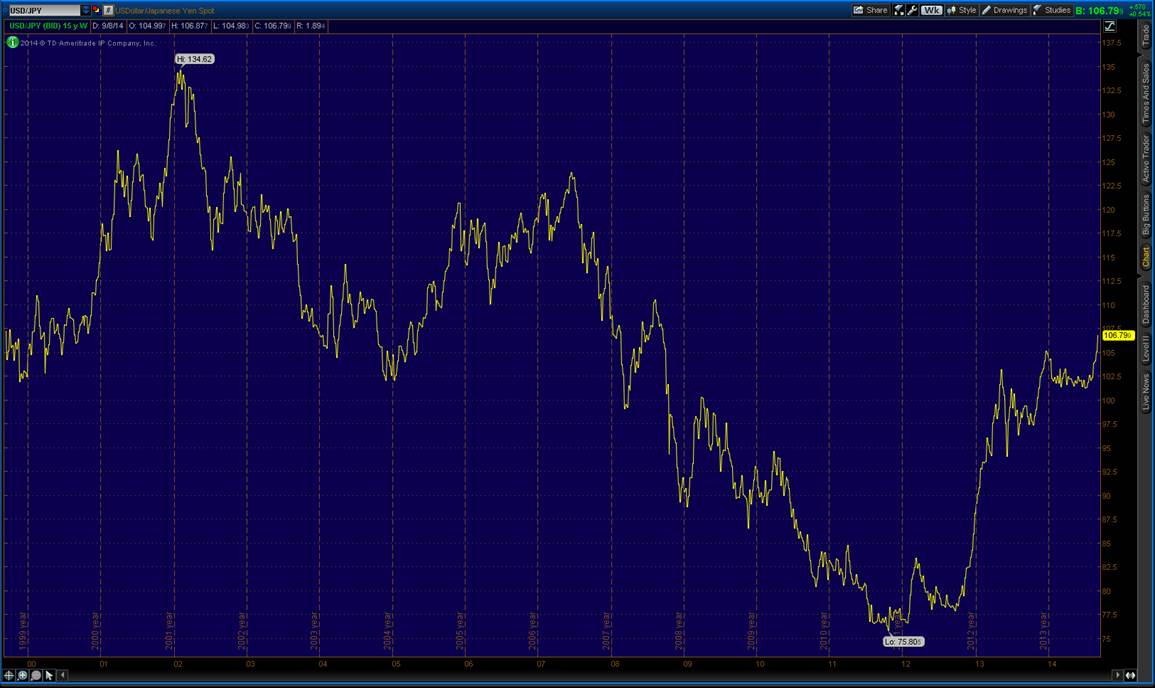

Round 2 for the Japanese Yen

By: Chris Tell

Today’s article is compliments of our friend Mark Schumacher at ThinkGrowth. Mark has been a reader and subsequently become a regular bouncing board for us with respect to publicly traded equities, market sentiment and the like. I always value his thoughts and it is a rare occasion that we disagree. Enjoy!

As our portfolio clients are well aware, we have been long the US dollar vs. the Japanese yen (USD/JPY) via a sizable position in YCS – purchased in the mid $40s – for almost two years beginning around the time Shinzo Abe was elected Prime Minister after running on his three arrows platform:

- Monetary stimulus

- Fiscal stimulus

- Structural change

He promised large doses of each to invigorate the Japanese economy and I took him at his word knowing it meant a much weaker yen.

Arrow #3 WILL work but it is politically very difficult to implement as it requires near term pain during the adjustment phase to produce the positive long-term benefits of improved productivity and more efficient allocation of resources; labor and capital. Progress on arrow #3 has been dismal, and to my knowledge nothing significant is in the pipeline. I would not hold my breath on this one.

He has delivered on the first two arrows by inflating the money supply, lowering interest rates and expanding government budget deficits. The longer arrows #1 and #2 are implemented the weaker the yen and later JGBs (Japanese government bonds) will ultimately become. The hope is that the weaker yen will stimulate exports and somehow provide a net boost to the country even though Japan is a large importer especially of energy, commodities and labor-intensive manufactured components.

The theories and policies underlying arrows #1 and #2 are founded on fairy dust. It is an academic pipe dream to believe currency debasement and government debt are shortcuts to prosperity. Yet the dream lives on… not just in Japan either.

Post Abe’s election the USD/JPY exchange rate rapidly appreciated from the low 80s to the high 90s and we benefited nicely with YCS appreciating about $20 into the mid $60s. Since then the exchange rate has been in a narrow range with the yen losing some value and YCS being flat through the first eight months of this year.

However, post this consolidation period, it looks like a second round of yen weakness is now occurring and there appears to be an identifiable catalyst. Notice how YCS (a long USD short JPY fund) is moving sharply higher again in the two year chart below.

2-Year Chart of YCS

The Yen’s Second Wave of Weakness Begins

The catalyst for the next wave of yen weakness is the most recent release of Japanese economic data which was worse than expected. In Q2 the Japanese economy as measured by GDP shrank 7.1% due to a fall in both consumer spending and capital investments.

After 18 months of Abe’s massive monetary and fiscal stimulus the economy is not gaining meaningful traction to say the very least. I see this as another demonstration of how these policies cannot expand the size of the economic pie because they do not create wealth or economic prosperity, in fact, they destroy it by unnaturally skewing incentives and therefore behavior.

In a world run by rational minds, the weak Q2 data along with a string of other weak Japanese economic data would be an impetus to ditch arrows #1 and #2 and focus on #3 in which case there would be no compelling reason for us to be short the yen.

Rather than question the cause-and-effect assumptions underlying their monetary and fiscal policies in the face of a failure of results, policy makers almost always conclude that the problem was either the size or timing of their programs. This may be counter intuitive to your logical mind, but the longer Abe’s policies fail to deliver the hoped-for economic results, the more intensely they will be implemented… bad for Japan, good for our investment in YCS.

Expect more yen weakness over the coming year as the exchange rate heads back towards where it was pre-2008′s financial crisis.

15-Year Chart of USD vs. JPY

As you can see, Mark is a sharp thinker. We have previously published some of his musings on portfolio diversification, buying out of favor stocks and market volatility, and I encourage you to read them.

Commodities Drop to 5-Year Low With Abundant Corn to Oil Supply

By: Bloomberg

Commodities fell to a five-year low on speculation abundant supplies and slowing economic growth outside of the U.S. will curb demand for raw materials.

The Bloomberg Commodity Index declined 1.2 percent by 5:06 p.m. in London to the lowest since July 2009. Brent oil traded at the cheapest since 2012, wheat, corn and soybeans retreated to four-year lows and gold slumped to a seven-month low.

Weak economic growth in Europe and Japan is leading to lower energy prices and interest rates in the U.S. at a time when the U.S. corn crop is a record high and U.S. oil production is poised to be the most in 45 years. The euro-area recovery stalled in the second quarter and Japan contracted by the most in more than five years. Food prices fell to the lowest in almost four years as costs of milk and and cooking oils tumbled, the Food & Agriculture Organization said today.

"We have had disappointing growth data," Kevin Norrish, an analyst at Barclays Plc in London, said today by phone. "Growth now looks a bit less promising and supplies in many commodities are quite robust."

Brent declined for a sixth day, falling as much as 1.4 percent to $96.72 a barrel, the lowest since July 2, 2012. Copper retreated 0.5 percent to $6,833.50 a metric ton and wheat fell to the lowest price since July 2010.

‘Buying Opportunity’

"It may be a buying opportunity for consumers," said Jodie Gunzberg, global head of commodities at S&P Dow Jones Indices, part of McGraw Hill Financial Inc., in an interview in London yesterday. "The question going forward is have supplies been replaced for agriculture and energy enough to create a persistent excess?"

Prices have come down as stockpiles declined, leading to the buying opportunity, she said. Copper inventories in warehouses monitored by the London Metal Exchange dropped 57 percent this year. "Demand from companies for commodities should pick up," she said.

Gold futures dropped as much as 0.8 percent to $1,235.30 an ounce on the Comex in New York, the lowest since Jan. 23. Prices have declined 11 percent from this year’s high as the U.S. economy gained traction. Demand for a haven declined after tensions in Ukraine and the Middle East eased. Global holdings in ETPs backed by gold declined in four of the past five months. Silver slumped 1.9 percent to the lowest since June 2013.

Dollar Strength

"The strong wall of dollar strength and prospects of a rate hike are pushing gold lower," Ira Epstein, the president of his namesake division at the Linn Group Inc. in Chicago, said in a telephone interview. "The outlook for gold is very weak in the absence of an escalation of violence" in Ukraine or the Gaza Strip, he said.

An index of 55 food items dropped 3.6 percent to 196.6 points, the lowest since September 2010, the United Nations’ Rome-based FAO said. The agency’s gauge of dairy prices slumped 11 percent and the vegetable-oil price index declined 8 percent to the lowest since November 2009, the FAO said.

Cotton, soybean, corn and wheat prices fell into bear markets this year as farmers in the U.S., the largest grain grower, prepare to collect what the government predicts will be record harvests. In the past three years, all agricultural values on the Bloomberg Commodity Index other than cattle and hogs have declined, led by corn, soybean oil and sugar.

Grains Outlook

"I don’t think we’ve seen the bottom yet," Abdolreza Abbassian, a senior economist at the FAO, wrote in an e-mailed reply to questions. "Grains could fall further."

The food index is down 3.9 percent from a year earlier, led by a 19 percent drop in dairy values and a 12 percent slide for the FAO’s grain-price index.

World wheat reserves before the 2015 Northern Hemisphere harvest will be 2.002 billion bushels, the U.S. Department of Agriculture said today, topping analyst forecasts for 1.995 billion bushels.

"The weather in most of the U.S. remains wonderfully grain productive," economist Dennis Gartman wrote in his daily newsletter. "The trends still remain downward and relentlessly so."

U.S. stocks headed for further drops?

By Paul Dobson and Callie Bost

U.S. stocks dropped after Brent crude sank to a two-year low amid signs of excess supply. The ruble slid to a record and European equities fell a fifth day as officials said new sanctions against Russia will come into force tomorrow.

The Standard & Poor’s 500 Index retreated 0.3% at 9:34 a.m. in New York. Brent (NYMEX:SCV14) slid to the cheapest since 2012, sending the Bloomberg Commodity Index to a four-year low. Russia’s currency (CME:R6V13) declined 0.8% to 37.57 per dollar, weakening for a fourth day, while the Micex index dropped 1%. The Stoxx Europe 600 lost 0.3%, while the The MSCI Emerging Markets Index headed for a sixth straight loss. The yield on 10-year Treasury notes fell to 2.51%.

The International Energy Agency cut its global oil demand forecasts a day after OPEC lowered its supply outlook. Initial claims for jobless insurance in the U.S. unexpectedly rose last week. EU countries agreed to implement plans to bar some Russian state-owned defense and energy companies from raising capital in the bloc, while an opinion poll damped bets Scotland would vote for independence. President Barack Obama pledged more air strikes on Islamic State extremists. China’s consumer inflation eased to a four-month low in August.

“All of this goes under the umbrella that any slowing overseas could impact the U.S. economy,” Todd Salamone, senior vice president of research at Cincinnati-based Schaeffer’s Investment Research, said via phone. “Mainly with IEA cutting oil demand forecasts, China with a four-month low in its consumer price index number, and additional sanctions in Russia, it seems like the knee-jerk reaction from a technical and headline perspective is to sell.”

Jobless Data

The S&P 500 (CME:SPZ14) halted a two-day slide yesterday as a rally in Apple Inc. boosted technology shares as investors continued to speculate on the timing of Federal Reserve interest-rate increases. Policy officials next meet Sept. 16-17.

The unexpected gain in jobless claims today interrupted a steady decrease to the lowest level since before the last recession and may boost Chair Janet Yellen’s assertion that slack remains in the labor market.

Energy stocks tumbled for a fourth day, as West Texas Intermediate (NYMEX:CLV14) slid to a 16-month low. Chevron Corp. and Exxon Mobil Corp. dropped at least 0.9%.

The IEA cut its global oil demand forecasts for 2015 and said Saudi Arabia exported the least in almost three years amid slowing purchases from China and Europe. Crude prices are poised to drop next year as U.S. production climbs to a 45-year high, the Energy Information Administration said Sept. 9.

Relentless Campaign

Obama yesterday pledged a “relentless” campaign to destroy Islamic State extremists in Iraq and Syria, with Middle Eastern allies such as Saudi Arabia and Jordan playing crucial supporting roles. The conflict in Iraq, the second-biggest OPEC producer, has spared oil facilities in the south, home to about three-quarters of its crude output.

Treasury 10-year notes (CBOT:ZNZ14) climbed for the first time in six days, pushing yields down from a five-week high. German bonds of similar maturity were little changed, with yields at 1.04%. Spanish securities fell for a fourth day, sending the yield three basis points higher to 2.29%.

“Geopolitical tensions are supporting demand for the least-risky assets,” said Alessandro Giansanti, a senior rates strategist at ING Groep NV in Amsterdam. “Concerns over the growth outlook in China and in Europe, as well as their global implication, also underpin safe-haven demand.”

China Inflation

Chinese consumer prices increased 2% in August, compared with a 2.3% gain in July, and estimates for a 2.2% advance, according to data released today. Chinese producer prices fell 1.2%, more than the 1.1% slip forecast in Bloomberg surveys of analysts.

The Shanghai Composite Index dropped 0.3% and the Hang Seng China Enterprises Index of mainland companies listed in Hong Kong slid 0.8%, declining 3.3% in two days, the biggest back-to-back retreat since February.

The MSCI Emerging Markets Index slid 0.5%, headed for the longest losing streak since November as the ruble weakened amid renewed EU sanctions on Russia.

The EU agreed to implement plans to bar some Russian state- owned defense and energy companies from raising capital in the bloc, three EU officials said under condition of anonymity in Brussels. EU governments voted for the sanctions on Sept. 5, delaying their implementation as the cease-fire between Ukraine and Russian-backed separatists began to take hold.

Still Negative

Russia will respond appropriately to the sanctions, Foreign Ministry spokesman Alexander Lukashevich said at a briefing in Moscow.

“The decision was expected, but is still negative,” Dmitry Dorofeev, a money manager from BCS Financial Group in Moscow, said in e-mailed comments on the Russian sanctions. “This may lead to counter-sanctions from the Russian side, as well as a new interest-rate hike.”

The Stoxx Europe 600 Index slipped 0.2%. Royal Bank of Scotland Group Plc advanced 1.4% as a Survation poll yesterday showed weaker support than other surveys had for Scottish nationalists’ bid for independence. Lloyds Banking Group Plc added 1.1% after saying it has a contingency plan for setting up new legal entities in England.

The pound (CME:B6Z14) strengthened against all of its 16 major counterparts, gaining 0.3% to $1.6254.

The Bloomberg Commodity Index of 22 raw materials dropped as much as 0.7% to the lowest since June 2010. Brent declined for a sixth day, falling as much as 1.4% to the lowest since July 2012. Copper slumped 0.9% to $6,810 a metric ton and wheat (CBOT:ZWZ14) fell to the lowest price since July 2010.

Super Mario is Dusting Off his Monetary Bazooka: What’s Next?

by Sprout Money

The long-expected meeting of the European Central Bank last Thursday was followed very closely by economists and investors. After the additional stimulus measures taken in June, the ECB once again lowered its main interest rates and the deposit interest even decreased into negative territory.

The benchmark rate was lowered to 0.05% (vs 0.15% previously) and the deposit interest decreased to -0.2% whilst the lending rate was lowered to 0.3%, coming from 0.4%. On top of that, the ECB will pump an additional 1,000 billion euro into the Eurozone’s economy which will enhance the liquidity as the ECB will purchase asset-backed securities and covered bonds with the money. The requirements and conditions for these purchases will be announced in the next monthly meeting in October.

This news doesn’t really come as a big surprise as the markets already realized in August that the ECB was changing its strategy after the comments made by president Mario Draghi in Jackson Hole. The deflation-threat as well as the disappointing credit numbers in the Eurozone needed to be dealt with. However, there are also some opposing arguments predominantly from the ‘real’ economy as not a lot of households notice an influence in their daily life. The problem is that this dirt-cheap money is being invested on the capital markets rather than being used to help those who need it the most. So even though a 1,000 billion euro blank cheque sounds impressive, it’s absolutely not certain that the this will lead to an increased lending activity in the private sector which should boost the inflation or inflation expectations.

And that’s the problem. You can lead the horse to the water, but you cannot make it drink. The unemployment rate in the Eurozone is 11.5% which is still very high and this situation is quite different from the situation in the USA where 200,000 new jobs are being created every month. Additionally, the inflation rate decreased further and by August it had shrunk to just 0.3%.

The most important victim of the new ECB policy will be the EUR/USD exchange rate. As the next chart shows, the Euro sank immediately after the announcement and at this moment, the Euro is at its lowest level versus the US Dollar in 14 months. The ‘expensive’ Euro has been a cause of concern of policy makers for quite a while now as it undermines the competitiveness of the European industry and mainly the net exporting companies and countries. The EUR/USD exchange rate has now decreased by approximately 7% since the May high.

Another important element we will have to keep an eye on is the balance sheet of the ECB. Mario Draghi hinted at the possibility to expand the balance sheet once again to the level of 2012. This would be an increase of 1,000 billion euro, and the impact of the recently announced measures on the balance sheet of the ECB remains uncertain.

After the introduction of the LTRO’s in June several market spectators were quite positive, but the expected impact of that specific measure was relatively small. And even with the most recently announced measures, the ECB is still trailing the other central banks on the liquidity creation-level. As you can see on the next chart from Bloomberg, the total balance sheet of the ECB has shrunk by 35% compared to the summer of 2012. Meanwhile, both the Federal Reserve and the Bank of Japan have increased their respective balance sheets.

However, the ECB has now clearly understood that the low inflation was reaching a very risky territory at the current rate of 0.3%, but it’s clear that there’s a long way to go before the ECB’s balance sheet will be at the same level of its international counterparts. Additionally, there’s an internal twist going on as the vote to expand the balance sheet wasn’t unanimous. It’s important to note that the president of the Deutsche Bundesbank, Jens Weidmann, is resisting against the current low yield environment and the various stimulus programs. That’s not really a big surprise as the Germans have historically always been cautious about inflation.

So what’s the main takeaway for investors? It’s clear that the conservative investor with just a savings account will be off the worst because the interest rates will very likely continue to decrease. Investors are actually being forced by the ECB to invest in products with a higher risk to get any return. Anyone who wants to have a serious solution for this problem and wants to safeguard his purchasing power will inevitably have to invest in tangible assets and will have to reduce its position in fixed income investments (mainly bonds from the core countries of the Eurozone). At Sprout Money we consider ‘tangible assets’ all asset classes which cannot be created out of thin air by the central banks.

Good examples are real estate, commodities, gold, gold mining companies but also share positions of qualitative companies with an excellent track record with a decent (and preferably continuous increasing) dividend to cover the inflation. Who’s just standing like a cow in the pasture looking at a passing train might have a serious issue when the inflation rate suddenly increases within the next few years. Aim to safeguard your purchase power and protect your capital, as at this moment capital preservation is even more important than returns on investment.

Warning Sign: Collapsing Oil Prices

By Michael Lombardi

Oil plays a critical role in economic growth as oil is used in a variety of industries. In times of economic growth, oil prices rise. When the economy is soft, or getting soft, oil prices fall as demand for oil wanes.

Over the past two months, oil prices have collapsed for the simple reason that the global economy is getting weak.

The chart below shows the steep sell-off in oil prices that started in mid-June.

Chart courtesy of www.StockCharts.com

Chart courtesy of www.StockCharts.com

What’s interesting to note is that oil prices are falling at a time when we have numerous troubling events in the Middle East and Russia. In normal circumstances, these developments would have caused oil prices to soar.

One more chart I want to show you today (which continues to spell trouble ahead for the global economy) is the Baltic Dry Index (BDI). Since the beginning of the year, this indicator of global economic activity has been collapsing.

Since January, the BDI has fallen 45%. The BDI is an indicator of trade in the global economy; the less trade in the world, the weaker the global economy.

Over the past few months, the chances of the global economy witnessing an economic slowdown have risen significantly.

As I have been writing, the eurozone is in very deep economic trouble again. Japan, the third-biggest hub in the global economy, is begging for growth. And the manufacturing and real estate sectors in the Chinese economy are slowing at a staggering rate.

The continued growth of the global economy is critical for the U.S. economy. In 2012, 46.6% of the S&P 500 companies had sales from outside of the U.S. economy. (Source: S&P Dow Jones Indices, August 2013.)

How the stock market will continue to rise when half of the S&P 500 companies are getting their revenue from a global economy that weakens each passing day is a mystery—that is unless the stock market advance is a fake, a bear trap, as I have been warning.

After default, Argentina economy falling into deeper hole

By Sarah Marsh

BUENOS AIRES (Reuters) - Argentina's government is ramping up state intervention in the economy to try to prevent a new debt default from triggering a balance of payments crisis but its policies are also battering business confidence and may deepen a recession.

In the six weeks since Argentina failed to complete a debt coupon payment and defaulted for the second time in 12 years, the government has restricted the amount of dollars available to importers, boosted subsidies and drawn up proposals to interfere in private companies' output plans.

"They're clamping down on foreign goods," said 42-year-old camping store salesman Javier Aguirre, gesturing at a single sleeping bag hung on a rack meant to display a dozen. "We are having to place things carefully at the front of the shelves to make it seem we're well stocked."

Along the Santa Fe shopping boulevard in Buenos Aires, the choke on imports and a sharp decline in consumer spending have driven up shop closures and forced retailers to bring forward sales.

The leftist government's measures are meant to shore up foreign reserves that stand at less than five months worth of imports and boost consumer confidence to prevent the $490 billion economy already contracting.

But with no signs of a deal to emerge from default and thus no prospect of a return to global debt markets, capital flight has intensified, pushing the peso currency to record lows and fuelling inflation.

One company manager who imports agricultural machinery, including water pumps and generators, describes the government's policies as "lethal" even before the default, and says they are now even worse.

He said the import curbs mean he been able to import goods worth just $2,795 in the first six months of the year compared with an average $25 million in previous years.

"We are eating up stock just to pay taxes," said the manager, who asked not to be identified because he was speaking out against the government. "We have merchandise for a few months, not more than a year, and after that the company will die."

Business leaders have long complained about President Cristina Fernandez's interventionist policies.

Heavy government spending and high commodity prices helped drive strong growth in the early years of her presidency but tight controls on prices and the currency market have caused imbalances in the economy and it fell into recession this year.

Foreign reserves have slumped and inflation is running at more than 30 percent.

"It was bad enough before, but with the default everything's worse," said Carolina Tiscornia, who works in a clothing store that is closing after revenues fell 30 percent this year.

IMPORT SQUEEZE

Argentina's reserves stand at eight-year lows of $28.4 billion and the central bank cannot keep tucking into its hard currency savings to defend the peso.

Exports are also falling more sharply than expected so the government risks having to drain its reserves perilously low to meet its energy imports bill and make good on its pledge to keep servicing performing debt.

Siobhan Morden, an economist at Jefferies, forecasts that Argentina will owe about $14 billion in debt payments next year and that reserves could drop as low as $7 billion by the end of 2015.

That has left policymakers few options beyond fighting to protect the trade surplus, their primary source of dollars, so the central bank has restricted further the dollars available to importers.

Reuters could not independently verify the numbers but businesses say the restrictions are harsher for industries where imports are considered non-essential or where the government wants to promote domestic production, including agricultural machinery and auto parts.

Adding to their woes, importers complain the debt default and the weak economy have undermined the confidence of suppliers in the ability of Argentine firms to pay their bills.

Importers have seen deadlines to repay credit lines shrink to an average of 30 days from 110 days before the default on July 30, said Miguel Ponce, spokesman for the Argentine Chamber of Importers.

'ASPHYXIATING INTERVENTIONISM'

Exports are down 10 percent this year as key trade partner Brazil tipped into recession and global prices for soy, corn and wheat fell to their lowest levels since 2010.

Industrial output has been in decline for 12 months.

Fiat's Argentine subsidiary cut production and put 3,000 workers on rotating leave because of slack demand and difficulties importing components, local media reported earlier this month. Fiat was not reachable for comment.

Other car makers have also slowed production, sparking a showdown between the auto industry and tough-talking Fernandez, who accuses them of holding stock back because of inflation.

In an attempt to keep production lines running and stem job losses, the government is threatening to intervene in the production decisions of large companies while also boosting subsidies to some industries in a attempt to spur growth.

The so-called "Supply Law", which is passing smoothly through Congress, would allow the government to cap prices, set profit margins and determine production levels.

The proposal has alarmed big business. Last week, leaders from the agricultural, banking, industry and retail sectors joined forces to threaten legal action against the bill.

"We urge the legislative power to take into account the risks this initiative implies for job creation, investment, output growth and adequate supply," the group said.

Rodolfo Rossi, a former central banker and staunch Fernandez critic, told Reuters the package of measures implemented since the default amounted to "asphyxiating state interventionism".

ANOTHER DEVALUATION?

David Rees at London-based Capital Economics said he expects the Argentina economy to shrink 2-3 percent this year and "there is a growing risk that the recession will spill over into 2015."

Private economists say the printing of money to finance government spending is also stoking inflation, adding pressure to the ailing peso.

The deteriorating economic outlook is pushing Argentines to seek refuge in dollars and the margin between the official exchange rate and black market rate has widened to 70 percent from 44 percent pre-default.

The black market "blue peso" traded at 14.25 per dollar on Thursday, down around 30 percent so far this year.

To take pressure of the peso, the central bank last week raised the minimum monthly salary required for Argentines to buy dollars and reduced the amount of hard currency commercial banks can hold.

Neither will halt the peso's fall for long and a new devaluation is widely expected, adding to inflationary pressures.

"My wages went up 18 percent last year while inflation was around 25 percent ... This year will likely be worse," said one state school maths teacher who gave his name as Miguel. He said he now buys the cheapest food brands but still struggles to pay his bills.

Supermarket sales have fallen for seven straight months, including a 4 percent slide in June, and many smaller stores have been hit even harder.

"Our revenue is down 20 percent from last year," said Daniela Sisca, the owner of a cake shop in the affluent Recoleta neighborhood. "You notice people buying less especially at the end of the month."

3 Things Worth Thinking About

by Lance Roberts

That was the latest proclamation from CNN Money following the release of the latest Job Opening and Labor Turnover Survey from the Department of Labor. It is good news on the surface, however, as usual single data points must be put into some form of reference, or they are meaningless.

First, there is a very anomalous spike in the data that has not previously occurred in the series as shown.

It could be a function of a temporary “snap-back” in demand following the extremely cold winter last year that led to a sharp drop in economic activity in the first quarter of this year. Or, it could be an anomaly in the data that is eventually revised away at some point in the future.

However, there are two other points to consider. Frist, the rise in job openings, which, unfortunately, are primarily focused in lower wage paying jobs, is not as strong as it appears considering the surge in individuals considered to be no longer part of the labor force (Not In Labor Force of NILF). The chart above shows job openings as a percentage of those sitting outside the labor force. Historically, there has been a fairly tight relationship between these measures as job openings would pull labor off of the sidelines and back into the labor force. However, since 2011 the gap has widened as the acceleration in those falling out of the labor force far exceed the number of available job openings.

Secondly, the rise in job openings, while an encouraging economic sign, is also at levels that have been normally more coincident with peaks of employment cycles and economic expansions. The chart below shows net hires (total hires less total separations – 4 mo. Average) as compared to annual percentage change in total employment. Considering that the current economic expansion is the fifth longest in the history, there is an argument that current levels of employment may indeed be indicative of “full employment.” If that is the case, it supports the theory that a “structural shift” in employment is the cause of the continued drag on economic growth.

Revisiting The Interest Rate/Equity Conundrum

I have discussed previously that the current divergence between interest rates and the equity markets was likely to be resolved quite painfully at some point.

“Both stocks and bonds cannot be right. While stocks have risen to new all-time highs in recent days, bond yields have fallen toward the lows of the year. As shown in the chart below, there has historically been a correlation between interest rates and the financial market from a risk on/risk off indication."

"It makes some sense given that when the markets have a preference for risk, asset allocations have shifted from bonds to equities and vice versa. As the demand for bonds falls, and the demand for stocks rise, yields rise. However, the current decline in yields, amidst a very low volume ramp-up in stock prices, suggests that the demand for safety is outweighing the demand for risk.

If historical correlations reassert themselves, the deviation between stock prices and bond yields will correct and likely not to the favor of the bulls.”

This idea was discussed by The Economist yesterday stating:

“If secular stagnation has set in, then yields could stay low for longer. And growth has been weak for a time.

But if you think that low bond yields can be justified by the secular stagnation story, what does that imply for the equity market? With the exception of the US, valuations do not look high (and some emerging markets, including China, look fairly cheap compared with their, admittedly short, history). In many cases, multinationals (investment grade companies) offer dividend yields that are higher than their corporate bond yields. But, again, Japan has shown us that prolonged stagnation eats away at stock market performance. And in the US, profits and margins are well above average levels. As Deutsche sagely says

‘For valuations to be sustained and for equity returns to mirror those seen through history, at some point we need nominal GDP growth to improve on recent trends. The real problem for equity valuations will be if we continue in this low growth world for many years.’

There we have it; if bond yields are justified by low growth, equity valuations in the US are not justified.

Those who continue to act on the assumption that high returns can be achieved are storing up a lot of trouble.”

Quietly Breaking A Topping Formation

I have happy to announce that I am going to be able to start providing technical commentary to you from the illustrious Walter Murphy, Jr.* Yesterday, Walter discussed the recent break of a topping formation in the financial markets. To wit:

“On Tuesday the S&P 500 recorded its fifth loss in six sessions with a 0.65% decline to 1988. NYSE declining stocks exceeded winners by 5:1 while the up/down volume ratio was bearish by a bit less than 7:2. Turnover increased by 3%. The daily Coppock Curve has a bearish bias for 23 of the 24 S&P industry groups, for 27 of the 30 DJIA stocks, and for 84 of the stocks in the NASDAQ 100.

While last Friday’s weakness was deep enough to lock in the S&P’s August-September uptrend as a complete pattern, the reversal was not confirmed by broader indexes such as the S&P 1500, the NYSE Composite, or the Wilshire 5000. That is no longer the case; as a result of Tuesday’s weakness, all three of those indexes have reversed their respective August-September uptrends.”

Considering that there has not been a correction of any real magnitude since 2012; it is prudent to be aware that there is a risk of a deeper correction currently. On a positive note, longer term trends currently remain intact but that can, and does, tend to change quickly. As Walter suggests…”Stay Tuned.”

No country for old money

by The Economist

If Scotland gains independence it will need a new currency and a new central bank

WHEN it comes to money and banking, no country has a richer history than Scotland. It was a Scot, David Hume, who in a 1748 essay set out the first coherent theory of the links between money, inflation and growth. And it is a Scottish idea, the joint-stock bank that, starting in the mid-1800s, became the backbone of global finance. Yet Scotland’s monetary future is as uncertain as its past is proud. Nationalist leaders say that if voters opt for independence in a poll scheduled for September 18th, the country will retain the pound in a currency union with the residual United Kingdom (rUK). That is a terrible idea.

The currency union that Scotland’s nationalist party, the SNP, envisages would be similar to the euro area. Sterling notes and coins would continue to circulate in Scotland, with the Bank of England setting a single interest rate for both countries and standing behind Scottish lenders in times of crisis. Such a union would eliminate exchange-rate risk and the cost of currency conversions, bolstering trade. Since the trade in goods and services between Scotland and rUK ran to £110 billion ($178 billion) in 2013—around two-thirds of Scotland’s GDP—the SNP reckons a sterling union would be best, both for Scotland and UK.

While trade is important, other factors matter too. In an influential paper published in 1961 Robert Mundell of Columbia University set out a set of tests for shared currencies. In an “optimal currency area” the factors of production—capital and labour—must be able to move freely. A sterling zone would pass this test, with its common language and many internal migrants. Capital would flow freely too, with the intertwined banking sector linking savers in one country with borrowers in another.

But a sterling zone would face big problems. Its members’ business cycles are reasonably well aligned, but not perfectly in step (see chart 1). That means that as it is, monetary policy is often too tight on one side of the border and too loose on the other. This divergence is likely to increase, since the budgetary transfers and shared fiscal policy that help to synchronise the two economies would cease. The SNP is planning to increase spending by 3% a year in Scotland, whereas the Conservative-led government in Britain wants to balance its books by 2019. Yet Scotland already has a bigger deficit than rUK, and its fiscal position is forecast to worsen as its population ages. Lacking a common fiscal policy, the sterling zone could easily become a mini euro area, with Scotland in the part of Greece. That explains why all three unionist parties oppose this option, and why the Bank of England’s governor, Mark Carney, called it “incompatible with sovereignty” in a speech on September 9th.

If the rUK stymies currency union plans, the SNP claims it will continue to use the pound anyway. This option—sterlingisation—is certainly feasible: there are 11 nations that use another country’s currency informally according to a recent IMF study. Kiribati, a Pacific archipelago, has used the Australian dollar since 1979. Montenegro, Kosovo and Andorra all use the euro despite not being members of the EU. Ecuador and El Salvador use the American dollar.

But there are two big problems with sterlingisation. With the Bank of England no longer responsible for Scotland, monetary policy would be set solely for rUK. If Scotland started to boom or slump but rUK was running well, the bank would not respond; the volatile oil industry means this is quite likely (see chart 2). The implications for Scotland’s financial-services industry could hardly be worse. Scotland is host to a large financial sector, which contributes 12.5% of its GDP. With no central bank supporting them, its banks and insurance companies would be seen as riskier investments and the cost of their borrowing would rise. Many would shift their headquarters to England taking highly paid staff and tax revenues with them.

Taking a punt

The best option sounds most radical: a new currency and new central bank. It is actually a very common step: 28 new central banks have been set up in the past 25 years. They sprang up rapidly in the 1990s as former Soviet and Yugoslav states gained independence. Iraq established a new bank and currency in 2003. Most recently Crimea has been attempting to set one up.

These innovators give blueprints Scotland could follow. When Estonia gained independence in August 1991, the government decided to create a new currency to replace the rouble. Less than a year later, in June 1992, deposits held in Estonian banks were redenominated, from roubles to kroons. Special counters at the new central bank were opened to allow residents to swap the old currency for the new one. As a show of confidence in the kroon, residents were also permitted to switch roubles for German marks, a strong currency. The scheme, reviewed in a 2002 IMF paper, worked well: the switch to a new central bank and currency took a week.

An independent Scotland should be able to follow this example. It will have more time to plan: fully 18 months between the vote and independence, which would come in May 2016. Scottish notes already circulate, and production could easily be scaled up. The new country’s share of Britain’s foreign-exchange reserves—around £9 billion—would provide credibility.

Deciding how the new currency should be managed would be more complicated. Poland and the Czech Republic quickly adopted inflation targets, allowing their exchange rates to float. But in order to smooth trade in the new country’s early years, it would be better to fix the exchange rate against the pound, according to Angus Armstrong and Monique Ebell of NIESR, a think-tank. This would require the SNP to rein in its spending plans. If it did not, Scotland’s expanding deficit might prompt a run on the new currency. But at least such austerity would be in support of a gleaming new currency, rather than to keep in step with grubby old English money.

George Soros Warns "This Is The Worst Possible Time" For Scottish Independence

by George Soros

This is the worst possible time for Britain to consider leaving the EU – or for Scotland to break with Britain.

The EU is an unfinished project of European states that have sacrificed part of their sovereignty to form an ever-closer union based on shared values and ideals. Those shared values are under attack on multiple fronts. Russia’s undeclared war against Ukraine is perhaps the most immediate example but it is by no means the only one. Resurgent nationalism and illiberal democracy are on the rise within Europe, at its borders and around the globe.

Since world war two the European powers, along with the US, have been the main supporters of the prevailing international order. Yet, in recent years, overwhelmed by the euro crisis, Europe has turned inward, diminishing its ability to play a forceful role in international affairs.

To make matters worse, the US has done the same, if for different reasons. Their preoccupation with domestic matters has created a vacuum that ambitious regional powers have sought to fill.

The resulting breakdown of international governance has given rise to a plethora of unresolved crises around the globe. The breakdown is most acute in the Middle East. The sudden emergence of the Islamic State in Iraq and the Levant, or Isis, provides the most gruesome example of how far it can go and how much human suffering it can cause.

With the Russian invasion of Ukraine, military conflict has spread to Europe. Two radically different forms of government are competing for ascendancy. The EU stands for principles of liberal democracy, international governance and the rule of law. In Russia, President Vladimir Putin maintains the outward appearance of democracy by exploiting a narrative of ethnic and religious nationalism to generate popular support for his corrupt, authoritarian regime.

As a major power and global financial centre, Britain ought to be centrally involved in crafting a European response to this threat. But like the US and the EU itself, Britain has also been distracted by internal matters. Conservative Prime Minister David Cameron has been persuaded by anti-European zeal – not least within his own party – to put UK membership in the EU to a vote in 2017. A poll on Scottish independence is only days away. Just when Britain should be confronting grave threats to its way of life, it is preoccupied with divorce of one type or another.

Divorce is always messy. A vote for Scottish independence would weaken – in political and economic terms – both a truncated UK and Scotland. An independent Scotland would be financially unstable, especially if threats to renege on debt repayments were carried through.

For Scotland and the rest of the UK to enter into a currency union without a political union, after the euro crisis has demonstrated all the pitfalls, would be a retrograde step that neither side should contemplate. Yet without it, an independent Scotland could not benefit from the low interest rates that a strong pound has brought. These considerations ought to outweigh whatever possible benefits independence might bring.

Yes, there are significant policy differences between Scotland and the rest of the UK. There is a more left-leaning approach to many issues, notably education, north of the border. But Scotland would be better placed to attain its political goals as part of a united Britain that is part of the EU.

The same applies to a British exit from Europe. Policy differences can be mediated. A divorce would weaken the UK. Those who call for separation seem to have forgotten that Britain currently enjoys the best of all possible worlds. Being part of the EU but not part of the euro allows the UK to enjoy the trading benefits without the currency constraints.

Furthermore, Britain has always played a balancing role between hostile blocs. Its absence would greatly diminish the weight of the EU in the world.

The EU has proved to be the best guarantor of peace and human security since the end of the second world war. The importance of preserving the shared values underpinning a whole way of life far outweigh any possible advantages of independence. The difficult times we are facing call for increased unity, not divorce.

Only if Britain fails to resolve its differences with the EU, and if the pro-European Scots (having voted to remain within the UK) thus find themselves unwillingly excluded from Europe in 2017, would there be just cause for Scots to call for a new referendum. If it comes to that, Scotland will be in a different position – one that could legitimise a split.

But to vote for independence from the UK now would be to prematurely surrender Scottish leverage in London, and Britain’s leverage in the world.

Parallels to 1937

by Robert J. Shiller

NEW HAVEN – The depression that followed the stock-market crash of 1929 took a turn for the worse eight years later, and recovery came only with the enormous economic stimulus provided by World War II, a conflict that cost more than 60 million lives. By the time recovery finally arrived, much of Europe and Asia lay in ruins.

The current world situation is not nearly so dire, but there are parallels, particularly to 1937. Now, as then, people have been disappointed for a long time, and many are despairing. They are becoming more fearful for their long-term economic future. And such fears can have severe consequences.

For example, the impact of the 2008 financial crisis on the Ukrainian and Russian economies might ultimately be behind the recent war there. According to the International Monetary Fund, both Ukraine and Russia experienced spectacular growth from 2002 to 2007: over those five years, real per capita GDP rose 52% in Ukraine and 46% in Russia. That is history now: real per capita GDP growth was only 0.2% last year in Ukraine, and only 1.3% in Russia. The discontent generated by such disappointment may help to explain Ukrainian separatists’ anger, Russians’ discontent, and Russian President Vladimir Putin’s decision to annex Crimea and to support the separatists.

There is a name for the despair that has been driving discontent – and not only in Russia and Ukraine – since the financial crisis. That name is the “new normal,” referring to long-term diminished prospects for economic growth, a term popularized by Bill Gross, a founder of bond giant PIMCO.

The despair felt after 1937 led to the emergence of similar new terms then, too. “Secular stagnation,” referring to long-term economic malaise, is one example. The word secular comes from the Latin saeculum, meaning a generation or a century. The word stagnation suggests a swamp, implying a breeding ground for virulent dangers. In the late 1930s, people were also worrying about discontent in Europe, which had already powered the rise of Adolph Hitler and Benito Mussolini.

The other term that suddenly became prominent around 1937 was “underconsumptionism” – the theory that fearful people may want to save too much for difficult times ahead. Moreover, the amount of saving that people desire exceeds the available investment opportunities. As a result, the desire to save will not add to aggregate saving to start new businesses, construct and sell new buildings, and so forth. Though investors may bid up prices of existing capital assets, their attempts to save only slow down the economy.

“Secular stagnation” and “underconsumptionism” are terms that betray an underlying pessimism, which, by discouraging spending, not only reinforces a weak economy, but also generates anger, intolerance, and a potential for violence.

In his magnum opus The Moral Consequences of Economic Growth, Benjamin M. Friedman showed many examples of declining economic growth giving rise – with variable and sometimes long lags – to intolerance, aggressive nationalism, and war. He concluded that, “The value of a rising standard of living lies not just in the concrete improvements it brings to how individuals live but in how it shapes the social, political, and ultimately the moral character of a people.”

Some will doubt the importance of economic growth. Maybe, many say, we are too ambitious and ought to enjoy a higher quality of life with more leisure. Maybe they are right.

But the real issue is self-esteem and the social-comparison processes that psychologist Leon Festinger observed as a universal human trait. Though many will deny it, we are always comparing ourselves with others, and hoping to climb the social ladder. People will never be happy with newfound opportunities for leisure if it seems to signal their failure relative to others.

The hope that economic growth promotes peace and tolerance is based on people’s tendency to compare themselves not just to others in the present, but also to the what they remember of people – including themselves – in the past. According to Friedman, “Obviously nothing can enable the majority of the population to be better off than everyone else. But not only is it possible for most people to be better off than they used to be, that is precisely what economic growth means.”

The downside of the sanctions imposed against Russia for its behavior in eastern Ukraine is that they may produce a recession throughout Europe and beyond. That will leave the world with unhappy Russians, unhappy Ukrainians, and unhappy Europeans whose sense of confidence and support for peaceful democratic institutions will weaken.

While some kinds of sanctions against international aggression appear to be necessary, we must remain mindful of the risks associated with extreme or punishing measures. It would be highly desirable to come to an agreement to end the sanctions; to integrate Russia (and Ukraine) more fully into the world economy; and to couple these steps with expansionary economic policies. A satisfactory resolution of the current conflict requires nothing less.

OJ crop challenged

Commodity traders eye strengthening dollar

Commodity prices have been feeling the backlash of a strengthening dollar as of late, and investors it seems have become accustomed to the adage coined during the financial recession that the dollar is the least dirty shirt. With the ECB and BoJ likely to ease and the Bank of England first having to deal with the politics of potential Scottish secession, all eyes are on the safety of the dollar and the prospect of Fed tightening that could occur before most other central banks.

The rise in production of U.S. crude oil and tepid global recovery have weighed on the largest commodity market with WTI crude prices dropping close to $90.00 per barrel. The European benchmark contract of Brent crude closed below $100 per barrel for the first time in 16 months. The shift in focus from the Ukraine/Russia conflict has also resurrected risk appetite and dulled demand for gold, the price of which has also been negatively impacted by a stronger greenback.

Crop prices have suffered as well, with traders assuming ample supply on the horizon. Generally speaking, the luster of trading commodities has somewhat dissipated on account of the dull global recovery, settled weather conditions and most recently on account of weakening appeal of prices typically favored during times of dollar weakening. But perhaps orange juice futures are getting off lightly – or at least relatively so. Forget the rain, says commodity analyst Judy Ganes. “Florida citrus growers have more on their mind than the amount rain they are getting as the fruit has been dropping prematurely from their trees and their production is dwindling rapidly,” she notes in her latest Monthly Softs Fast Facts publication. Despite little impact from this year’s hurricane season, the market already knows that supply is dwindling and that next month’s USDA crop report could reveal further shrinkage. But watch out, notes Ms. Ganes.

Chart – Speculators looking for OJ to follow crude or gold rather than fundamental supply woes

The tail-end of the hurricane season is usually the most active time period for storms to develop, while “a cold snap in the winter would deal another blow to struggling growers since Florida orange production is already forecast to fall to a near 50-year low”. The loss of appetite amongst OJ speculators is apparent in the above price chart, which also shows the net speculative position held by investors.

Typically, they play from the long side in hopes of benefitting from a squeeze when hurricanes strike and decimate production. You can easily see that speculators together rarely get net short of this market, but they may be heading that way according to the latest data. That could prove rather interesting in the event that weather patterns – rain or freezing temperatures – weigh further upon supply.

Initial claims

The latest labor data missed forecast, with 15,000 more claims than expected at 315,000 through the last weekend. It is not a bad number, simply because the recovery in the labor market (using this measure at least) has come full circle. Numbers of around 300,000 are just what the economy was used to prior to the recession and it is possible we will not see continually declining initial claims data.

The four-week moving average remains close to that line in the sand at 304,000 and its stability should be the focus going forward. The Labor Department did note that even though it did not estimate claims data for any states in the latest week, the Labor Day holiday might have impacted the overall reading. Nothing to see here; move right along.

Chart – Initial claims and four-week moving average

Home Builders diverging again, similar to 2006-2007

by Chris Kimble

CLICK ON CHART TO ENLARGE

Almost four years ago the Power of the Pattern shared that a falling resistance line breakout would be good for home builders ETF XHB (see post here). Since the posting XHB is up almost 100%. Despite the S&P 500 doing well since 2010, XHB has out performed the S&P by 40%.

Turning the page forward, we have shared with Premium Members of late that a divergence is taking place between home builders and the broad markets that we feel is worth paying attention too.

The above chart reflects that the DJ Home Construction Index diverged against the S&P 500 for almost two years (2005-2007) before both of them fell in price together from 2007 to 2008.

The home construction index has now diverged against the S&P 500 for almost a year and a half. Humbly, I believe it is worth investors time to watch this divergence and to be careful should home builders and the broad market break support together.

The Fed Should Raise Rates Now; However, It Won't

by Morgan Myrmo

"It is far better to be alone than in bad company." - George Washington

As investors have come to learn in the current bull market, there is a lot riding on interest rates. With monetary expansion uttering the new era of long-term economic growth, the simple threat of "turning off the pump" and letting the economy work with less Fed monetary influence has investors completely spooked.

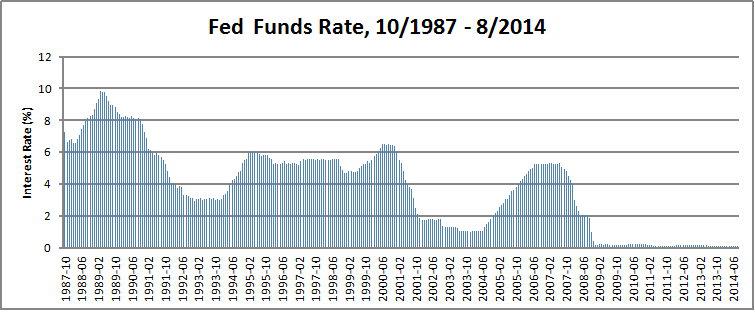

The next meeting scheduled for the Federal Open Market Committee, or FOMC, is September 16-17, 2014. Most anticipate the winding down of the bond-buying program as anticipated in October 2014. Also, the consensus is that rates will stay at near-zero due to the most recent "Fedtalk."

The Traditional Fed Directive Demands Higher Rates Now

Traditionally speaking, the Fed actions have functioned to promote its dual mandate of full employment and price stability. With the great recession however, the Fed has become more of an "American monetary Godfather," using a strong, government-backed Keynesian approach.

To save the domestic economy from irreversible disaster, the Fed created the unprecedented monetary policies that continue today and are often referred to as "quantitative easing."

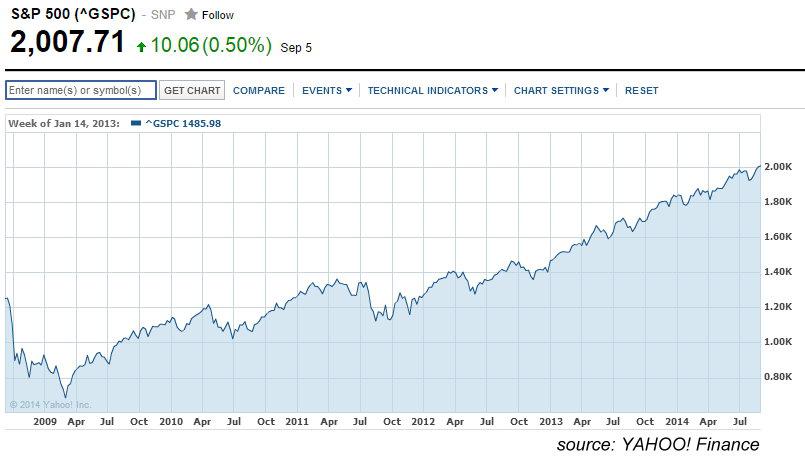

Also referred to as QE, or QE-Infinity to describe this continual, seemingly never-ending economic stimulus, quantitative easing has helped usher in a new era of stock returns as the current domestic bull market has clocked five consecutive years of positive annual returns.

(click to enlarge)

2014 is on-trend to deliver the 6th-straight year of gains, with the S&P 500 Index up nearly 10% at 2007.71 (September 5, 2014).

(click to enlarge)

Just because the stock market has recovered and is setting all-time highs does not mean the Fed should raise rates and put an end to QE. There are more important indicators to consider, such as economic strength and of course employment and inflation statistics.

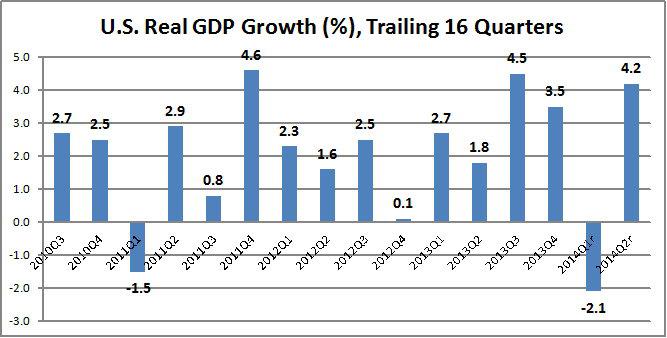

Economically speaking, the business cycle continues to improve, which clearly is lending a hand to stock market prices. According to the U.S. Bureau of Economic Analysis, the past four years have showcased continued economic growth, albeit with two quarters of economic contraction (most recently Q1 2014, -2.1%, adverse weather conditions blamed as major function of growth).

(click to enlarge)

While Real GDP is an important economic measure, it is more of a current indicator than a leading indicator. Looking at other measures will better forecast economic strength. The question that bestows us becomes not where the economy has been but where it is going and if the economy is forecasted to continually improve, then does the Fed need to continue with QE?

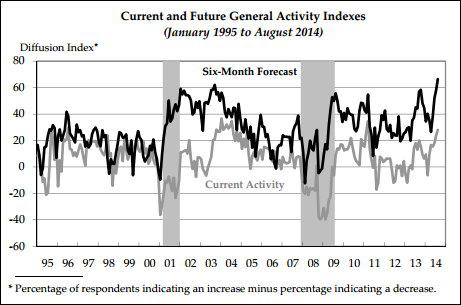

According to the Federal Reserve Bank of Philadelphia Manufacturing Business Outlook Survey, the Philly-Fed regional manufacturing sector continues to grow. According to the August 2014 survey newsletter:

"The survey's broad indicators of future activity increased, suggesting that firms remain optimistic about continued growth over the next six months."

Specifically notable is the overwhelmingly positive response that the economy will grow over the next six months (66.4%), while no respondents forecasted a decrease in business activity.

(click to enlarge)

Also to note, the diffusion index of current general activity reached the highest level since 2011, further suggestion that the regional economy is doing quite fine.

Philadelphia Federal Reserve Bank President Charles Plosser, in a speech on September 6, 2014, stated:

"The rate has been near zero for nearly six years now, and the Fed has augmented its aggressive policy actions through large-scale asset purchases, now tallying in the trillions, rather than in the billions of dollars. "

In reviewing the U.S. economy, Mr. Plosser continued:

"We are more than five years into a recovery that began in June 2009. While the pace has been sluggish and uneven, I believe the progress is undeniable. In fact, despite a winter cold spell in the first quarter, I remain mostly positive about the prospects ahead."

Regarding the lower-than-expected gains in August payrolls, Plosser cited the YOY trend is upward and showcases continued employment strength.

" I prefer to look at longer-term trends rather than monthly numbers that are still subject to revision. Year-to-date monthly average job growth has amounted to 215,000 jobs this year, compared with a monthly average of 194,000 jobs added last year.

Despite the slowdown in August, job creation has improved markedly this year. The economy has created 1.7 million jobs since the start of the year, nearly 10 percent more than the same period in 2013, 20 percent more than in 2012, and 30 percent more than in 2011.

The unemployment rate was 6.1 percent in August, down more than a full percentage point from a year ago. This means the unemployment rate continues to fall faster than many policymakers had been forecasting."

Plosser continued with information regarding inflation, which is trending upward and has recently been forecasted to reach 2% by 2015.

The Philadelphia Fed's most recent Survey of Professional Forecasters also increased its average estimate of headline PCE inflation to 1.8 percent in 2014, up from 1.6 percent in the last survey. The survey also increased the estimate of PCE inflation to 2.0 percent in 2015, up 0.1 percentage point from the previous estimate.

All of these figures suggest that inflation appears to be gradually moving closer to our target of 2 percent and doing so more quickly than anticipated in December 2013."

So when it comes to the dual mandate of the Federal Open Market Committee, of which Plosser is a member of for the remainder of 2014, it seems that a quicker-than-anticipated ending of QE should be required.

To back up the Philadelphia Business Outlook Survey, the August 2014 ISM Report on Business, released September 2, 2014 (four days before Plosser's speech), stated the following:

"The August PMI registered 59 percent, an increase of 1.9 percentage points from July's reading of 57.1 percent, indicating continued expansion in manufacturing. This month's PMI reflects the highest reading since March 2011 when the index registered 59.1 percent."

Clearly the trend is positive, with manufacturing expanding faster than average on the year.

Both FOMC member Plosser and the ISM are showcasing strong manufacturing data, which is backed up by continual growth in real GDP and strengthening employment data. So what is the Fed to do?

The Fed Should Raise Rates Now

To recap what most investors already understand, the dual-mandate of the Fed is to help the economy achieve full employment and ensure price stability. Currently domestic unemployment is at 6.1% and the economy has been adding on average 215k jobs per month this year, a 10.8% increase versus 194k monthly jobs in 2013.

Regarding PCE inflation, the inflation measurement the FOMC regards, Plosser revealed last Friday in his speech that inflation expectations of 2% for 2015 and inflation "appears to be gradually moving closer to our target of 2 percent and doing so more quickly than anticipated in December 2013.

While there is no agreed-upon definition of full employment and Plosser does acknowledge somewhat of a frustrated workforce, 6.1% unemployment is a giant step for the economic rebound. In his recent speech, Plosser states:

"Many Americans remain frustrated and disappointed in their jobs and job prospects. For example, there remains a large contingent of those working part time for reasons economists don't fully understand. Nonetheless, we have to acknowledge that significant progress has been made."

In other words, the Fed has succeeded in bringing the economy up to speed in terms of employment. With PCE inflation expectations of 2% coming sooner than anticipated just nine months ago and employment at or near full, it appears that the Fed has succeeded and that now is the time to raise rates.

Why Now, Why Not Later?

While the Fed has increased the money supply during QE, which is finally set to end in October 2014, the economy has been able to achieve relative price stability and job growth.

With a huge balance sheet now, the Fed needs to look at an exit strategy to tame inflation. A slow rise in interest rates, whilst keeping to an era of low-interest rates, would ensure dollar strength and continued positive real GDP growth.

Economic uncertainty, which would be created by rapid interest rate hikes, would spook business and investors would retreat quickly. Leave rates too low for too long and high interest rates would be required to tame inflation, which would come at the price of lower real estate prices, reduced consumer spending, lower GDP growth and increased stock market volatility.

What Will The Fed Do?

I believe the FOMC will raise rates sooner than the investment banks and markets anticipate. Goldman Sachs (NYSE:GS) believes that the rates will start to rise in October 2015, however with a strong economy, 6.1% unemployment and a sooner-than-later 2% PCE expectation blooming, the FOMC will have to act faster than expected.

What markets need to realize is that it's not the first rate hike that impedes economic growth, it's the continued rate hikes that the market does not expect that would threaten uninterrupted annual real GDP growth.

The Fed will have to change "verbiage" to reflect this. For the markets to stay in sync with the Fed, Janet Yellen should showcase an anticipated March 2015 hike to 0.25%, followed by the likelihood of another hike to 0.5% in October 2015.

(click to enlarge)

The current fiasco in Europe (on September 6, 2014 the ECB cut rates to near-zero and announced new QE, bond-buying measures) will only increase global demand for the dollar and dollar-denominated debt and equities into 2015. With slightly higher rates, additional collar-debt demand could in fact keep the 10-year treasuries at ~2.5% to ~2.75%.

In addition to stable, low-priced debt, the slightly higher interest rates will help stifle inflation, improve bank profitability, keep housing and commercial real estate prices stable and support continued positive real GDP growth.

A Very Imperfect Storm

By: Kevin Flynn

Last week, I took on the market's general belief in global central bank stimulus as a de facto guarantee of stock prices. The concluding assertion was "Central bank stimulus is not an invisible force field against adversity." Two weeks prior to that, I warned that Mr. Market might have some surprises in store for stock prices in the coming months, particularly during the period between Labor Day and Thanksgiving (a refinement upon the "eight weeks or so" estimate I originally gave). It seems appropriate to re-examine those assertions in light of recent developments, with a particular eye towards the markets.

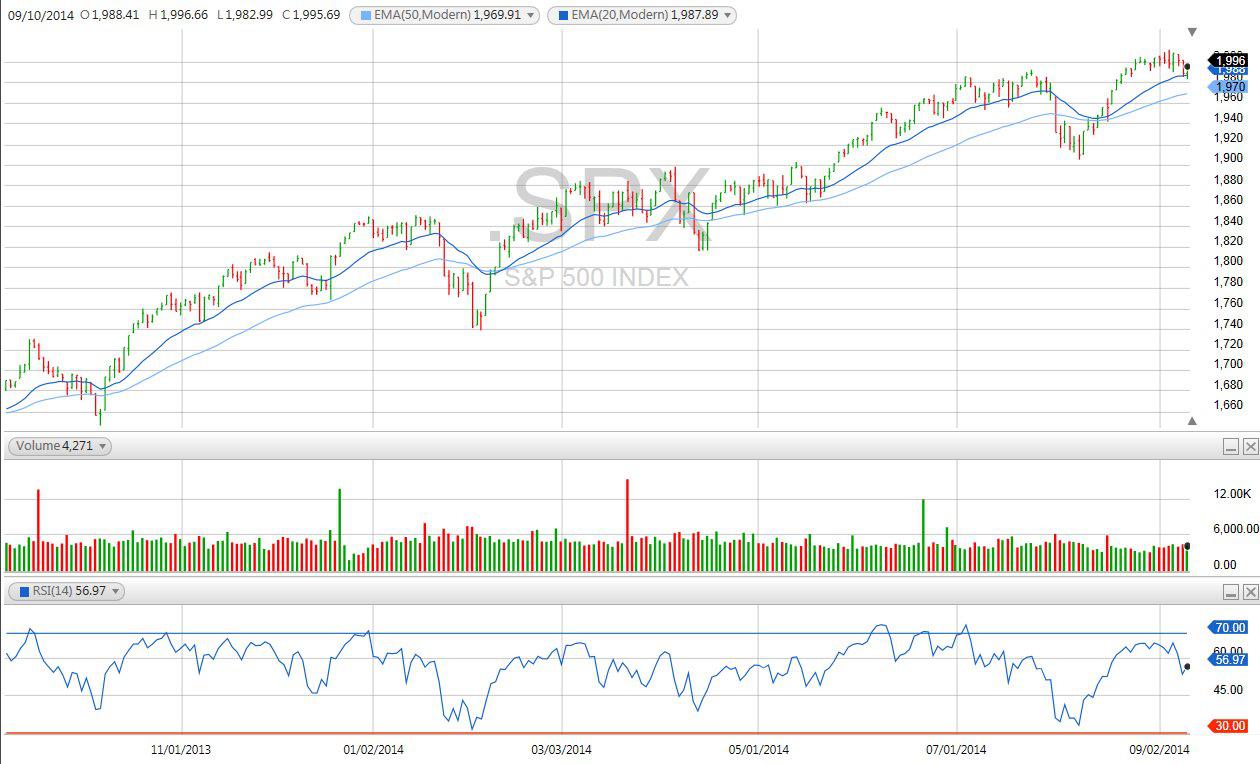

The stock market passed its first September test on Monday and Tuesday with a smooth bounce off the 20-day exponential moving average (EMA) on the S&P 500. It was particularly impressive on Tuesday morning, when prices pulled off a reversal seemingly out of thin air. Playing the rebound off the 20-day has been the percentage bet over the last two years, as the market has rarely spent much time below it. Most tests of the 20-day average have consisted of hovering for a day or so and then resuming the upward climb, as was apparently the case this week.

(click to enlarge)

The roughly ten-day prelude to our traditional back-to-school holiday is also the stock market's "silly season," when prices usually rally several percent on little more than the effect of junior clerks being buoyant (if limited) buyers while their seniors are all on holiday. It's the same vacation break as the all-too-brief one that places policymakers on hold from mischief-making, resulting in a benign news tape. That little pop is usually followed by early September weakness, and indeed, is probably the main reason why the average performance for the month is slightly negative.

This year's 1% pullback to the 20-day EMA feels like a rather modest move by post-Labor Day standards, and the quick rebound suggests that the upward momentum trend is indeed still intact. Put another way, the market has yet to get truly worried about much of anything - it couldn't find the 200-day EMA these days with a pick and shovel (the last visit there coming in the wake of the market's post-Obama re-election tantrum).

A word of caution on Mr. Market, though - the August rally off the QE trend line was on very light volume. That doesn't guarantee that the tape is about to make a big move downward, only that sentiment is flimsier than it looks, and more susceptible to exaggerated swings. A great deal is being written about how strong the stock market is this year that ignores the fact that more than half the gains have come in the last few weeks, on little news and even less volume.

The market still has a lot to get through before Thanksgiving can kick off the sacred tradition of the end-of-the-year rally. Scotland has been rattling global markets, with polls showing it might just vote "yes" on independence after all. My guess is that it will all turn out like the Greek vote a couple of years ago - a narrow cling to the status quo providing a rally in relief from the chasm that a secession victory would open up. I'm not making any bets in either direction, but if "yes" wins, look out below.

On the heels of the Scot vote comes the all-important Fed meeting next week. During the bull market, the pattern for stock prices around Fed meetings is to rally into them and then sell off afterwards. This time around might provide the reverse, as fears of what the central bank might say about tightening could lead to selling in advance of the meeting, followed by a relief rally afterwards. I'm not making predictions about what the Fed will say or do, mind you, only that the market is getting hit with a lot of warnings about potential sell-offs in advance of the meeting. With that much time to prepare, the market often ends up selling the rumor and buying the news. Should we get more evidence of a tightening bias, an initial sell-off followed by a big rip-reversal rally ("it could have been worse") would be classic Wall Street.

There's more going on than Scotland and the Fed. If famed investor Sam Zell and I were to have dinner and talk about anything but investments and what a nice city Chicago is, we'd probably come to blows. That said, I do respect his investment acumen, and we could have a fine time doing nothing but talking about what to buy and sell. Last week on CNBC, he made some observations that put me in mind of his 2007 posture: one, the stock market seemed an awful lot more elevated than the economy; two, he had never seen so many global uncertainties in his investing career; and most importantly, three: he has more fingers on his hand than he needs to count buying opportunities. That should worry you.

The Ukraine situation is going smoothly: Putin takes what he wants, and then we all breathe a sigh of relief when he goes back home after getting it. I'm not sure of the logic of this. But the situation isn't going to go away so easily, especially after President Obama made a point of stressing American backing of the Ukrainian people in his address on the violent Islamic extremist group ISIL, yet another potential source of instability (I don't know about you, but I'm crossing my fingers for Thursday the 11th).

Bear capitulation is another sign of impending volatility. There's been a rash of bailing bears lately, from Deutsche Bank's David Bianco, to my own surprise, Gina Martin Adams at Wells Fargo. I can't think of any Street bears still alive right now (I don't count anyone who manages a gold fund), and that is never something I like to see. The this-time-it's-different excuse-theory starting to make the rounds is that because the recovery was half-strength GDP-wise, it will last twice as long. Of course it will. The only consolation is that there's usually a time lapse of some months before the last capitulator finds occasion to regret his or her words.

Bond whiz Jeff Gundlach weighed in on CNBC during the week with an observation in line with what I have been saying since last fall - the Fed is out of ammunition to fight economic setbacks (though the bank would never admit as much). Gundlach made the remark in the context of it being the only possible sane reason for a rate hike, as otherwise, the economy is in for another rerun of 2% GDP that he doesn't see changing. Despite the Fed's exaggerated fearfulness about financial instability, I too see this as the main reason for raising rates - that, and the unemployment rate, which is surely going to be below 6% in 2015, if not before.

The August jobs report and the July JOLTS report both point to the same thing, in my opinion - the labor market is starting to peak. The apparent August weakness was not as bad as it looked, and the jobs data, claims data and JOLTS all point to a labor market that will top out next year. The Fed can't afford to be caught empty-handed.

Another big reason for raising rates is the restoration of normalcy (or an approximation thereof) in investing behavior. I don't know if anyone can definitely say what short rates would be without central bank intervention, but my guess is that the curve would look more like 1%-1.5% at the front end and 3%-4% at the long end. I don't think that those rates would impede economic growth at all, though I do concede that the transition to those rates will likely cause some financial system dislocations. The question that doesn't get enough mainstream attention, and the one that Gundlach perhaps should be asking is, why does the Fed have a lid on short rates at 0%-0.25% with an unemployment rate of only 6.1%? And its balance sheet is over $4 trillion?

That's the part that bothers me the most, because the ultra-low rate policy is without question creating asset price bubbles. The stock market is overvalued, but if you really want to know where the bubble is, it's in high-yield bonds, the proverbial elephant in the room that no one wants to talk about. We have effectively transferred the credit bubble from mortgage-backed bonds to the corporate high-yield sector.

German airline, Lufthansa, which has a junk rating from Moody's, sold five-year bonds Friday priced at 1.125% in an offering that was heavily oversubscribed. That's ridiculous. That's no amber light, it's a giant flashing red billboard. The bonds will be safe for a time yet, I readily concede. But once rates start to move back up, we are going to be faced with a world where everyone wants to unload a Mt. Everest of high-yield bonds and no one wants to buy them. All sellers and no buyers - that's a bond market recipe for financial system disaster. Didn't anyone see it coming?

The Risk Of Permanent Loss

by Smead Capital Management

Since the stock market has done extremely well from its "abyss-like" low in March of 2009, many investors are worried about the risks associated with owning U.S. large-cap stocks. A cacophony of articles have been written, which not only look for the stock market to correct, but also have an expectation of the kind of bear market decline which would set investors back for five years, like the declines in 2000-02 and 2007-09. Those declines each hit the S&P 500 Index for a loss of 40% or more.

We believe that investors should focus on the risk of "permanent" loss, and frame their concerns today around their long-duration participation in the stock market. Permanent loss can come in two forms. First, can I lose all the money I have in a company or portfolio by it going bankrupt? Second, can I severely damage my liquid assets by not handling the emotional pressure of a big decline (20% or more) and selling at the depths of the market low?