by Joseph L. Shaefer

Greenland may have been barren and cold in the 1800s, when this shanty became popular. But it wasn’t always so and, in the natural rhythms of Mother Earth’s warming and cooling, may not be so cold and barren in the near future. I haven't been to Greenland, but I have flown over it numerous times. I can assure you there is much green and brown as well as white and ice blue on that great island.

The name Greenland probably comes from the Norwegian Erik the Red, who sometime around 982 was exiled from Iceland for several murders, the circumstances of which were rather murky, with the victims being members of a powerful local family who had murdered members of Erik’s family. Nonetheless, he was exiled from Iceland for three years and henceforth set out with his extended family to find someplace where the reception would be warmer, if not the climate.

He may or may not have been the first Norseman to see Greenland (most accounts credit earlier visits of 50 and even 100 years) but it was Erik the Red who put it on the map (and his son, Leif Ericson, who later put the continent of North America on the map.) Erik allegedly called the place upon which he alighted Grœnland, or Greenland, in hopes of attracting other settlers to join him. (A technique that has been used by numerous real estate developers ever since, naming their tumbleweed-strewn desert lots Shady Acres, Mountain Shadows, Montreux Estates, and so on.)

It's important to note that about this same time what we call the “Thule peoples” began migrating from Alaska and by 1300 had settled in Greenland, displacing many of the then-native peoples as they brought such innovations as whaling harpoons and dog sleds with them. The Norsemen who came with Eric the Red, as well as those who followed after him, both taught and learned much from the native peoples and, later, the Thules they encountered. And, in the tradition of humans everywhere, they also fought with and killed each other from time to time.

These were not people huddling in caves, however, seeking haven from the ravages of continual winter. Ice core samples and clamshell-dated artifacts both clearly show that during this time frame, from roughly 900 to at least the 1300s, herbaceous trees and plants grew in Greenland, wine vines were planted, livestock were introduced, and plants such as barley -- essential for beer, whiskey and other necessities of life -- were grown. Given the natural ebb and flow of climate change on earth over the millennia, it may be that Greenland will once more be truly green.

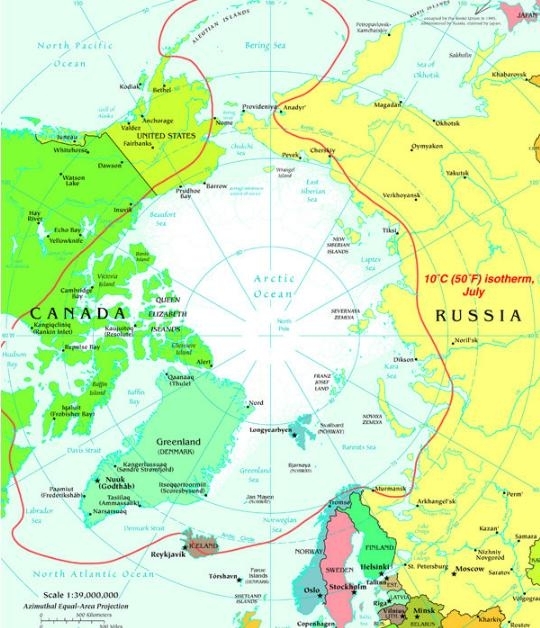

In fact, scientists recently probed 1.2 miles through a glacier in Greenland to recover the oldest plant DNA on record -- finding the DNA of trees, plants, butterflies and spiders from some 450,000 to 900,000 years ago – providing yet more evidence of natural global warming long before man appeared on the scene. With all this in mind, I invite you to take a close look at the map below (click to enlarge):

Before you write Greenland off as some Arctic Circle wasteland, please note that the southern tip of that great island lies just below the 60th latitude north. Note as well that sunny-in-the-summer Norway and Sweden lie mostly north of that same latitude (with major cities Oslo, Stockholm, Helsinki, and St. Petersburg, Russia, lying almost exactly along the parallel), with Finland and almost all of Alaska entirely north of it – just like Greenland -- though I hasten to note that Norway in particular, and Scandinavia in general, also benefit from the warm Gulf Stream currents...

Now consider where the massive discoveries of natural resources have taken place in recent years: oil and gas from the North Slope of Alaska, the north of Canada, the North Sea between Norway and Scotland, and the Russian north. Coal, iron, nickel, tungsten, gold, silver and rare earth elements (first discovered near the town of Ytterby, Sweden, to the northeast of Stockholm just below – you guessed it – latitude 60) are but a few of the other treasures the north has offered up.

Now if you look at the world from the view point of the map above, it simply makes sense that Greenland might also have been dusted with or surfeited with some of the same minerals and resources that its geologically-similar cousins in Russia, Canada, the US (Alaska) and the Nordic nations have. The Nordic nations are comprised of Iceland, Norway, Sweden, Finland, and Denmark, all of which have the bulk of their land mass north of Latitude 60 except for Denmark – but, then, since Greenland is currently “affiliated” with Denmark, we can’t exclude Denmark from this analysis.

(It’s a long story but the short version is: the Norwegians took responsibility for Greenland in the 1300s. Later, after combining with each other, rebelling from each other, etc., Norway and Denmark split for good in 1814. Denmark got Greenland. Greenland became an official and integral part of their kingdom in 1953. It was granted home rule by the Danish Parliament in 1979. In 2009, Greenland assumed self-determination with responsibility for self-government of judicial affairs, policing, and natural resources. Denmark maintains control of foreign affairs and defense. As part of the realm of the Kingdom of Denmark, Greenlanders elect two representatives who sit in Denmark’s Parliament. Ultimately the split will be final and Greenland will stand on its own.)

With the abundance of riches clearly discovered north of Latitude 60 by other nations, why do we hear nothing of such discoveries in Greenland or in the fecund waters surrounding Greenland? The answer lies in the political, cultural and ecological realms, not in the geologic or geographic. Denmark has done an admirable job of protecting the Inuit culture from outside influences. (88% of the some 58,000 Greenlanders are Inuit or mixed Danish and Inuit. The remaining 12% are mostly Danish. Almost all Greenlanders reside along the fjords in the south-west of the main island.) So currently fishing and ice fishing are the dominant means by which Greenlanders provide themselves with sustenance, just as they always have. In seasons with good catches, they depend upon fish and arctic shrimp for critical export products to trade for goods from elsewhere.

But that political and cultural decision to continue a certain way of life may or may not reflect the desires of native Greenlanders as they take their place among the nations of the world. Certainly they have shown a clear interest in the past in improving their standard of living by allowing other forms of exploration for valuable minerals and other natural resources.

Cryolite was discovered in Greenland in 1799 and has been used over the years to make caustic soda, as an insecticide and a pesticide, and, most significantly, in the production of aluminum. More recently, their state oil company, Nunaoil conducted a good deal of seismic research in Greenland’s coastal waters – enough so that third-party seismic data providers have found it profitable enough to take that task on themselves.

The state company Nunamineral has been seeking capital to increase the production of gold, which began in 2007. In that same year, their mining of ruby deposits also began. There is even a public company which became involved in ruby mining in 2004, which I’ll discuss below. And there are numerous other minerals projects just getting launched seeking likely deposits of uranium, aluminum, nickel, platinum, tungsten, titanium, lead, zinc and copper.

So – is Greenland the Final Frontier? With apologies to fellow Star Trek fans, it is certainly the largest land mass and continental shelf area that remains relatively unexplored on this planet, anyway. I say yes – Greenland is a place for brave investors to begin learning more about!

Among the ways I see as possible to participate would be the likelihood of responsible drilling for oil and gas offshore. Greenlanders cannot endanger their prolific fishing grounds, so they will most likely select shallower areas initially or the most experienced deeper-area operators with the most sterling safety records. I have crossed the North Atlantic twice via ship and seen its icebergs and gales firsthand. Make no mistake, these are treacherous waters. Two of our favored companies, both in our model portfolios, excel in this area. Both – no surprise – are Norwegian. No one has greater experience and a better safety record drilling in extreme environments than the Norwegians. I’ve also crossed the Skagerrak (the straits between Norway and Denmark) in 40-foot seas. My hat is off to anybody who can safely drill in those waters!

The first of these companies is Statoil (STO), partially owned by the Norwegian government, but which trades on the NYSE for the rest of us, and is quite liquid. Since I’ve written about it recently, let me suggest you take a look at that discussion rather than re-hash it here.

The second, which I’ve also suggested for your due diligence in an SA article here is Norway’s SeaDrill (SDRL), the world’s most successful deepwater driller and the one with the newest fleet of deepwater rigs. (In addition I mentioned both firms, among others, while advocating a safer approach to emerging markets, less than a month ago here.)

You may have other mineral, oil and gas, or other resource firms your due diligence has led you to. I suggest that if they are truly global thinkers and planners they, too, are quietly taking a look at Greenland as a not-too-distant future possibility.

There are a few “penny dreadfuls” which have already established a beachhead in Greenland and have contracts or actual ongoing operations there. I use the term penny dreadfuls not to be derisive – every firm has to start somewhere and some of these may go on to become giants – but because these firms are typically characterized by a large number of shares outstanding, as well as warrants and options granted to management and anyone providing them with capital. They are also characterized by a continuing need for capital since they usually have as yet no positive cash flow from their current operations. Since few bankers are willing to lend to them (Assets? What assets?) they must keep diluting current shareholders’ positions by issuing new stock.

With that (very large) caveat in mind, let’s take a quick look at a couple of these. I mentioned a ruby miner above. Their home page tells me “WE’VE DISCOVERED a new source of rubies that rivals those found in Burma,” and “YOU’VE DISCOVERED the opportunity to make a solid investment.” I was a defense attaché in Burma and I’m just not certain anyone can claim, at this early stage, that these rubies are their equivalent.

But, more, I dislike companies whose primary pitch, right on the home page, is to “investors” to pump up the stock price and not to vendors, buyers of their gems, and other stakeholders. Still, if that’s your thing, True North Gems (TNGMF.PK), at 12 ½ cents, down from a previous speculative blowoff in 2003 of 95 cents, but up from 8 cents in September, may just be your “buy ‘em when they’re cheap” kind of a gamble. They’ve been working each summer since 2004 to define their prospects and take some samples. The company has sapphire, emerald and nickel prospects in Canada, as well.

Greenland Minerals (GDLNF.PK) may not excite some as much as TNGMF, but it’s more my cup of tea. From a low of 10 cents at the bottom of the market in March 2009, it is now $1.38. I still like this Australia-based miner’s prospects, even at this price. In December, GDLNF received approval from the government of Greenland to fully evaluate the Kvanefjeld multi-element project, including radioactive elements like uranium. Why is this a huge deal? The Danes have a very “conservative” policy about anything nuclear. Despite their neighbor once-removed, France, deriving 75% of their electrical energy from safe, quiet, non-polluting nuclear, the Danes are dead-set against the stuff. They have never allowed so much as an analysis of just how much uranium might reside in Greenland.

Yet Kvanefjeld is a large mineralization deposit near the southern tip of Greenland that is rich in rare earth elements (REEs), uranium, and zinc. It is suspected to contain one of the world’s largest resources of REEs. The only question is whether the Greenland government will allow them to extract those REEs, knowing that some uranium may be moved or, with permission, extracted in the process. I'm guessing they will allow both. As the company says, "The Kvanefjeld Project is recognised as the world’s largest undeveloped JORC-compliant resource of rare earth oxides (REO), in a multi-element deposit that is also enriched in uranium and zinc." (The JORC Code comes from the Australasian Joint Ore Reserves Committee and is designed to assure minimum standards for public reporting to ensure that investors and their advisers have all the information they would reasonably require for forming a reliable opinion on the results and estimates being reported.)

In addition, the company has delineated yet another large mineralization complex, Ilimaussaq, with the potential to produce both light and heavy rare earth products, more uranium and zinc concentrates, fluoride compounds and zirconium. I believe Greenland Mineral's go-slow approach and respectful partnership with the government and people of Greenland gives them the inside track for further successes. Further information is available on their excellent website, including pdf’s of all the maps, geologic charts, and photos you could possibly want to see.

There are a number of other small companies exploring for REEs and metals in Greenland but I think we’ll save them for a later time. This is enough to digest in one sitting!