By Phil Flynn

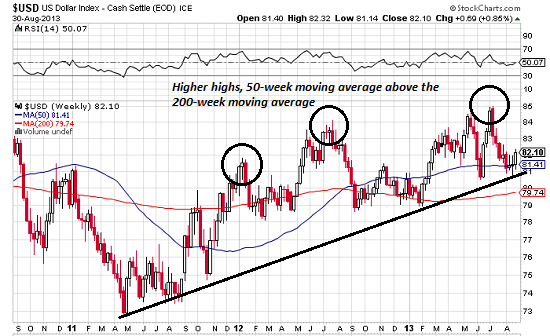

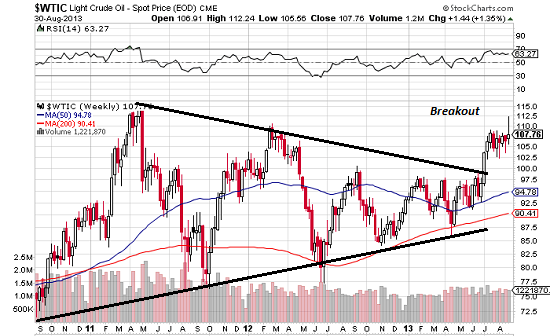

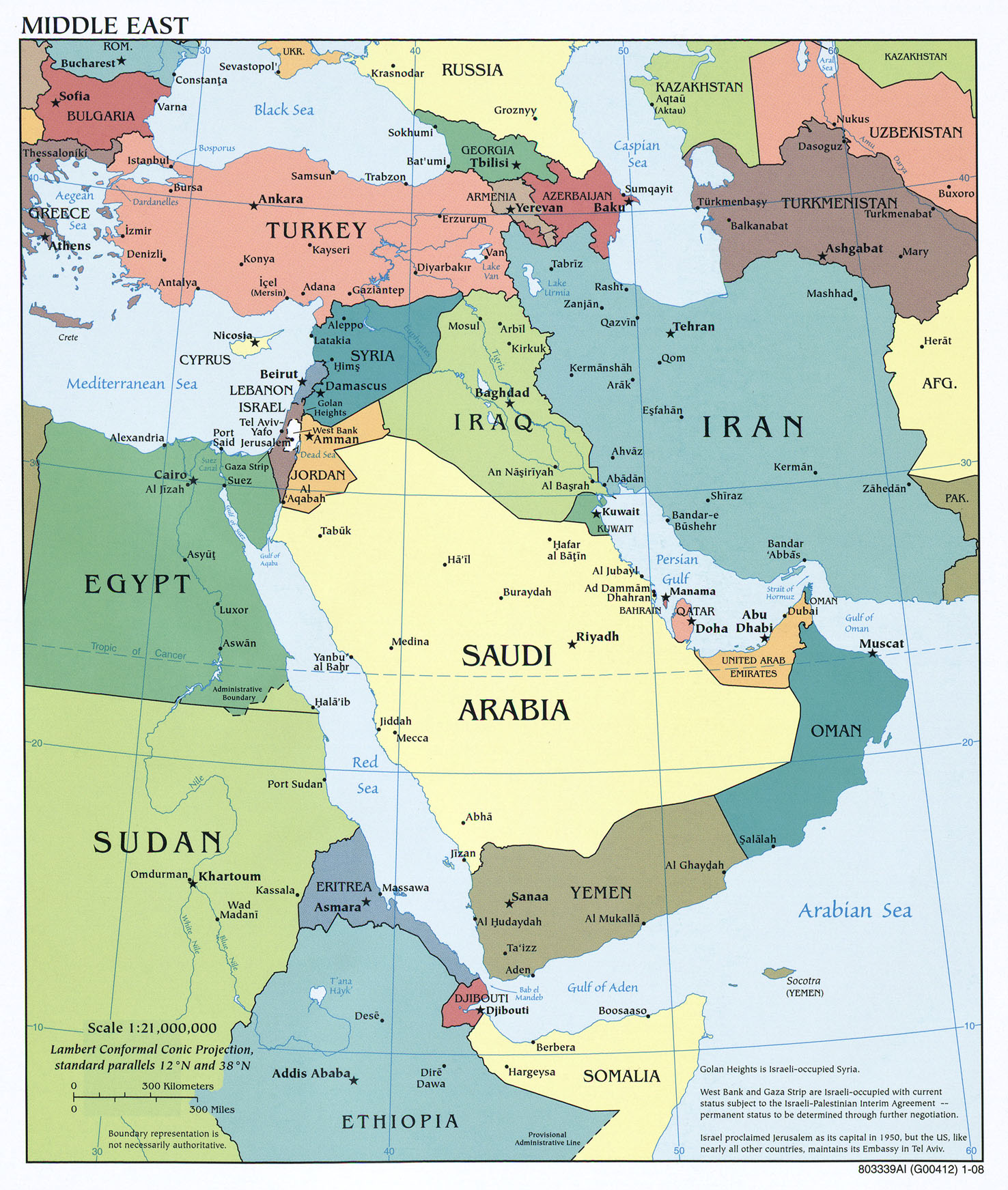

Speaker of the House John Boehner is on board and Senate votes today as the noose tightens around Syria’s neck. Even Vladamir Putin says he might be on board with an attack on Syria if it could be proved conclusively that the Assad regime actually used chemical weapons. Oil prices (NYMEX:CLV13) are being twisted and turned on all of the latest headlines. Seemingly wanting to break on a glut of supply but being supported by geopolitical risk. With the dollar on fire and emerging market currencies getting trounced, WTI continues to be supporting by the so called war premium. A war premium that not only includes a potential attack on Syria but has been juiced and pumped up by Egypt, Iraq and Libya as well.

Of course Mexico believes that the top is in. While Mexico isn’t exactly the best producer of oil, they know a good price when they see one. Reuters reports that Mexico has started executing its 2014 oil hedging program, energy trade sources said on Tuesday, bringing one of the biggest national oil sellers into the market amid a rally in crude prices. The annual hedging program, which is carried out by the Mexican Ministry of Finance, is closely watched by oil traders as the volume of selling needed to hedge even a percentage of the country's roughly 2.5 million barrels per day of production can move markets. Traders said the hedging program was depressing the Brent crude oil 2014 contract versus the Brent contract for delivery this December, which currently has a near $10 premium.

Gold (COMEX:GCZ13) and silver prices soared as emerging market currencies get smashed and South Africa’s National Union of Mineworkers, decided to go on strike and the possibility of war looms. Silver, the best performing commodity of last month, started off way in the lead once again.

Gold haters are stunned by the best back-to-back monthly performance of the metal since the 1970s. This market has many things in common with the 1970s and that is why we continue to maintain our bullish stance and a long term target of $2,400. Silver should retest $50 and longer term it should go as high as $77. Bottom line, never underestimate a market that has fallen under the cost of production and is seeing strong demand with a tightening supply scenario.

Barbara Powell of Bloomberg reported that gasoline slid to a three-week low as Monday’s U.S. Labor Day holiday marked the end of the nation’s summer driving season and a switch to winter-grade fuel, which is less-expensive to produce. Futures dropped as consumption typically declines after Labor Day when summer vacations end and students return to school. U.S. gasoline demand dipped to a five-week low in the seven days ended Aug. 23 and in June was the lowest for that month since 2001, government data show. Environmental regulations will ease this month, allowing refiners to choose from more components when blending fuel.

Supplies of reformulated gasoline blendstocks, or RBOB, along the U.S. East Coast, where Nymex futures are delivered, rose 687,000 barrels last week to 17 million, 8 percent higher than a year ago. Total U.S. inventories were 5 percent above the five-year average for that week, according to an EIA analysis.

Dow Jones reported that the national average price of retail diesel fuel rose 6.8 cents to $3.981 a gallon in the week ended Monday, the U.S. Energy Information Administration said Tuesday. That is the highest price since April 1. The price jump, the biggest since Feb. 11, came as crude-oil prices last week touched their highest level since February 2012 on worries that a potential U.S.-led strike on Syria could spill over into a broader crisis in the Middle East. Prices are 14.6 cents a gallon below their level a year earlier. The latest price puts retail diesel at 16.4% below the record high level of $4.764 a gallon hit on July 14, 2008. Then, diesel carried a premium to a year earlier of $1.875 a gallon as crude-oil prices soared to record highs near $150 a barrel. In its August Short-term Energy Outlook, the EIA said it expected diesel prices to average $3.91 a gallon in September, compared with a September record average high of $4.12 a gallon last year. The forecast is based on Nymex crude-oil futures averaging $100 a barrel, a five-year high for September, and up from $94.51 a year earlier.

Nymex crude futures opened the month on Tuesday at $108.54 a barrel. Internationally traded Brent crude oil, which holds sway over gasoline prices, is expected to average $104 a barrel this month, down from the September record last year of $112.86 a barrel. Brent is averaging $115 a barrel so far this month. Prices rose in all regions, led by an 8.3-cent rise in the Midwest. Crude-oil prices accounted for 65% of the cost of diesel fuel in July, according to the EIA. Release of the EIA data was delayed one day by the Labor Day holiday on Monday. AAA Daily Fuel Gauge Report said its survey put retail diesel prices Tuesday at $3.935 a gallon, up 4.7 cents from a week ago. Prices were 5.1 cents higher than a month ago, but were 16.6 cents below a year ago.

{kind=link}