By: Doug_Wakefield

"What the mind can conceive and believe it can achieve" ~ Napoleon Hill

When one looks at the US stock markets over the last two years, especially since August 2011, it would appear that it has become liberated from entering a bear market for more than a few days or weeks.

With each subsequent drop, a rally has ensued. US stock indices seem to move one step closer to nirvana with each passing "minor correction" in prices. One need never worry again, as we gain greater confidence in the masters of finance, who with the mere mention of the words, "a highly accommodative policy", can levitate stocks.

But something is very wrong with this picture. Outside of the Dow's value scrolling across the bottom of the daily news or the values showing up in our monthly online statement, is the every increasing dependency on more and more debt and "temporary" intervention to make certain "the recovery" removes all memory of the events of 2008 from our minds. Outside of the euphoric, "all time highs achieved again" is the nagging reality that no negative geopolitical or global economic event or data has phased US stocks for almost 2 years now. A bad day or two for sure, but that is all that the public has had to experience for almost 22 months.

Have we really arrived at a world of no pain and all gains, brought to us by the "highly accommodative policies" of the masters of finance and market intervention?

As we head into August, I would like to present you with data I believe supports the reality that millions of investors are soon to be stunned once again like they were in 2008. Like the Tsunamis we have watched in the last 10 years, we must remind ourselves and others that the bursting of global stock bubbles don't care about our long term plans, they change the landscape for everyone, including central bankers.

Lessons 1 - Forget The Real World, Watch the Computer. Power Continues to Concentrate

For months and months, anyone trying to explain why major technical, fundamental, or geopolitical risk would impact US stocks has looked like a fool who did not understand the new paradigm, brought to you by your nearest central banker. Sadly, this has bred rising complacency along with rising stock prices. Yet while this rally has gone on much longer than I and many others would have imagined, anyone willing to examine the evidence through what has ALREADY occurred, can see that the nirvana rally moves closer each day to a painful return to reality.

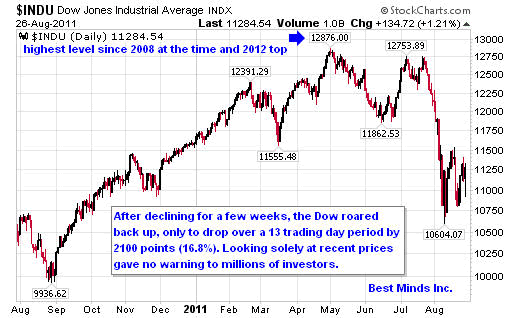

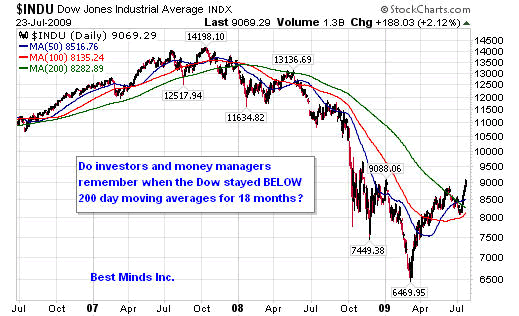

If you have no understanding of high frequency trading platforms or speed computer trading, then watch the report released by 60 minutes in June 2011, Wall Street: The Speed Traders. Anyone who believes this film is solely for those interested in keeping up with "financial news", needs to remember that in July 2011, the Dow topped and lost 2100 points (16.8%) in 13 trading days.

Consider the following opening remarks from this excellent piece:

"Most people don't know it, but the majority of the stock trades in the United States are no longer being made by human beings. They're being made by robot computers, capable of buying and selling thousands of different securities in the time it takes you to blink an eye.

These supercomputers - which actually decide which stocks to buy and sell - are operating on highly secret instructions programmed into them by math wizards, who may or may not know anything about the value of the companies that are being traded.

It's known as "high frequency trading," a phenomenon that's swept over much of Wall Street in the past few years and played a supporting role in the mini market crash last spring that saw the Dow Jones Industrial Average plunge 600 points in 15 minutes."

Does this sound like the world of "buy good companies and hold them", or "don't try to time when to get and get out of the markets, invest for the long term?" Anyone who downloads Scott Patterson's book, Dark Pools: The Rise of the Machine Traders and the Rigging of the US Stock Market (2013), learns the following:

"All of that turnover was having a real-world impact on stocks. At the end of World War II, the average holding for a stock was four years. By 2000, it was eight months. By 2008, it was two months. And by 2011 it was twenty-two seconds, at least according to one professor's estimates. One founder of a prominent high-frequency trading outfit claimed his firm's average holding period was a mere eleven seconds."

"Doug, I work with very sophisticated investment managers. I am certain they are at the top of the high speed trading world, even if I am not." From my own research, it is clear that those who desire to turnover stocks in seconds dominate the global markets today. Structures like pensions and mutual funds that are investing for "the long term" are being forced to follow whatever the biggest and fastest fish are doing in the global waters.

This makes investing look easy on the upside while returns that are clearly unsustainable are being produced, thus lulling the public into a false sense of security. Risk has grown at ever increasing levels of leverage while prices have climbed the unsustainable ladder.

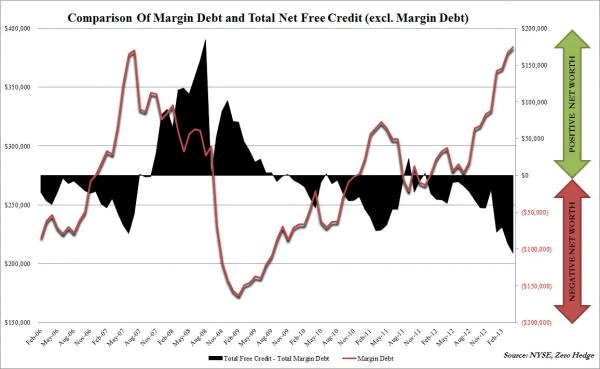

NYSE Margin Debt Rises To New All Time High As Net Worth Slides To Record Low, Zero Hedge, 5/28/13

As history proved two summers ago, when high-speed trading platforms pull back from stocks to protect their own capital, "long term" investors can be left holding the bag.

The problem we have with a world driven by speed computers, is that eventually, the computers are playing a game, looking for patterns. Whereas humans could have evaluated economic and geopolitical news in order to PREPARE a portfolio for rising risk, the computer - unless finding certain terms by which to react in milliseconds to "the news" by means of artificial intelligence - is solely focused on finding the pattern and beating its next slowest competitor in the DAILY scalping game of hyper trading. As long as the rhetoric from central bankers matches the view of "we have overcome risk and will always bring your 401k statement right back up", the public at large will remain ignorant and complacent. However, the reality is that millions of investors have placed their futures next to a small group who have left them holding the bag before when markets roll over from extremely leveraged levels.

Yes, the world of investing has changed radically.

"In 1933, the number of specialist firm on the NYSE totaled 230. By 1983, acquisitions and mergers had reduced that number to 59. By 2001, there were only 10. Today, only four DMMs (Designated Market Maker) control the trading on the NYSE: Goldman Sachs, Knight, Barclays, and newcomer GETCO....Most industry professionals we talk to believe these four horsemen are responsible for 40-50% of all trading on the NYSE. "[Broken Markets: How High Frequency Trading and Predatory Practices on Wall Street are Destroying Investor Confidence and Your Portfolio (2012) Sal Arnuk and Joe Saluzzi, location 621 of 5286 in the Kindle Edition]

Lesson 2 - Is Predictable a Good Thing?

If you wanted the public to believe that they were watching an economic recovery, what better way to do it than to have the Dow rise over a long period of time, totally ignoring negative economic and geopolitical events? If you had the power to turn markets at certain junctures, then the other smaller computers and investment fish would eventually see bad news as good news, and buying the dip would become a "sure thing". If you think this would be impossible to accomplish in a market as complex and diverse as the U.S. equity markets, take a look at the charts below. This is not speculating on what WILL happen; it is already a piece of history.

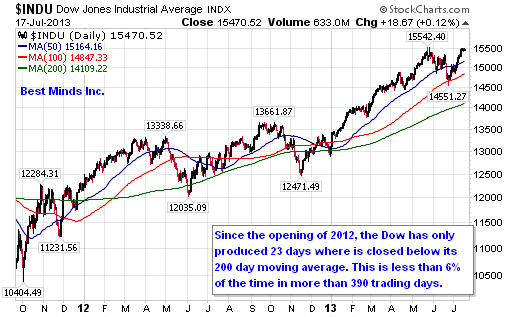

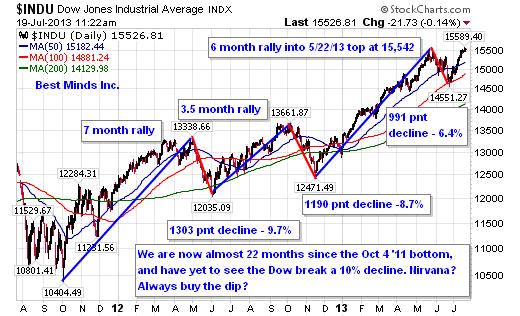

Once the Dow broke above the 200 day moving average in December 2012, it has only briefly stalled below this level. Did the high-speed trading platforms have anything to do with this? Could they have helped "lead" the "recovery"?

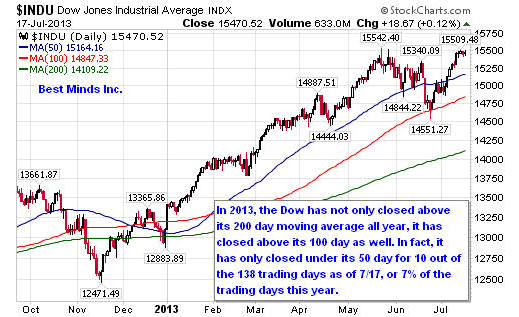

Now move forward to 2013. Notice, that once it was determined that the 200 day MA would hold at the end of 2012, and the fiscal cliff was a joke - I mean, who ever said we had to have a debt ceiling again anyway or record the amount of national debt we were accumulating. The bounce level was going to be at the 50 or 100 day moving averages, and beyond that, what is there to know?

Now think with me. Does history reveal that financial and political leaders desire the public to be pleased with their progress, when they had little to do with the progress that was made? Is it possible that the "progress" that has been made, required loading the system with more and more debt and interfering with markets to avoid those same markets from producing fear, while on the other hand rewarding complacency? Does that sound like a free market?

While the world of investors is still in the nirvana phase, is there anything one can gain from examining the historical archives? Do you remember a recent period in market history where SELLING rather than BUYING took place when these same moving averages were hit?

Lesson 3 - The Faster the Speed, the MORE likely an Accident

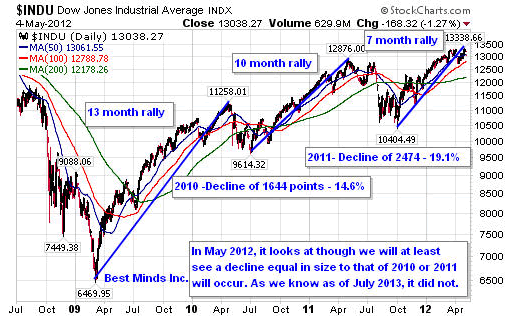

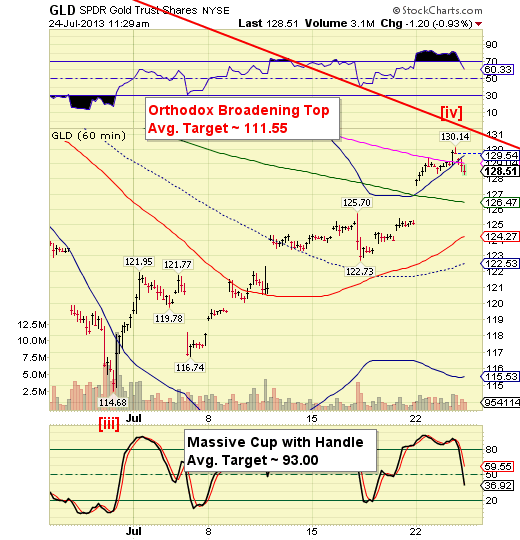

We gain confidence the more we see something working. We lose confidence the more we see something not working. And yet, this is exactly how great speculative bubbles are formed. Instead of seeing rising risk as a caution to sell and pare down, we see the rising prices as a lost opportunity and eventually succumb to watching individuals purchasing stocks and funds at their highest prices on record. We saw this in the spring of 2000, the fall of 2007, and are watching in live right now in the summer of 2013.

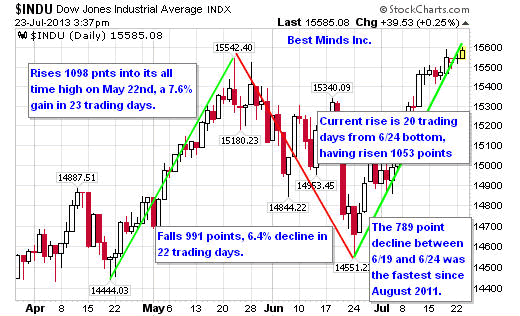

The best way to watch the math reveal a trap and not a triumph, we need to look for a pattern where markets climb faster with each subsequent rise, and declines become more shallow. Whether we return to the March 2009 bottom - the lowest this century - or the October 2011, we can see this pattern has already unfolded quiet clearly.

Looking at the two charts above, we can see the following:

- Rally of 13 months; decline of 14.6% into 2010 low.

- Rally of 10 months; decline of 19. 1% into 2011 low.

- Rally of almost 22 months, no decline beyond 10%.

Eventually, the bounces become so predictable - both computers and individuals totally ignoring all real world risk in order to capture the latest and hottest power rally - we can see price levels achieve the larger gains in shorter periods of time. The powerful drop that took place between June 19th and June 24th can only be seen in one way...another opportunity to get in, not a warning sign of a major top.

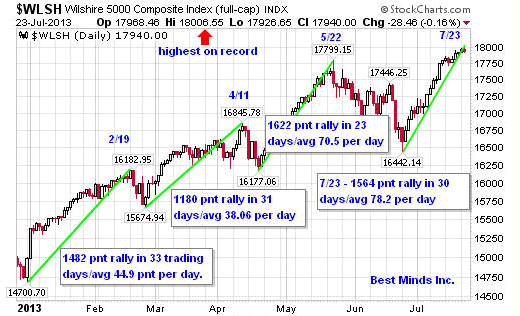

We can see the same pattern in the larger Wilshire 5,000, the broadest US stock index. Once the "fiscal cliff" was revealed as another stall in seriously challenging the status quo on December 31, 2012, US stocks took off. The Wilshire topped on February 19th. After a pull back to its 50-day moving average, it took off again, topping on April 11th. Once again it pulled backed to the 50 day MA, and started rising.

By the time it reached its high on May 22nd, it had scaled 1622 points in 23 trading days, averaging 84% more points than the climb into the April 11th top. More points; shorter timeframe.

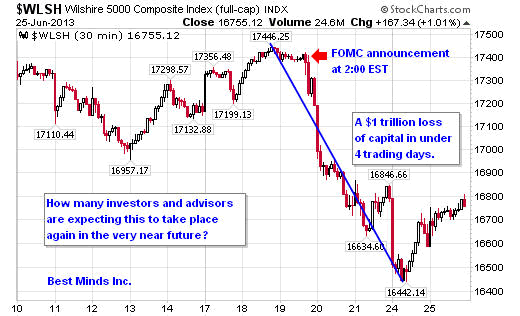

US stocks had drifted sideways into the June FOMC meeting. When the Federal Open Market Committee (FOMC), finished their regular scheduled meeting on June 19th, their press release (2:00 EST) was not well received by investors or more accurately, the split second artificial intelligence buried in the high frequency computer trading programs. In less than 4 trading days, the Wilshire had shaved off $1 trillion in paper wealth.

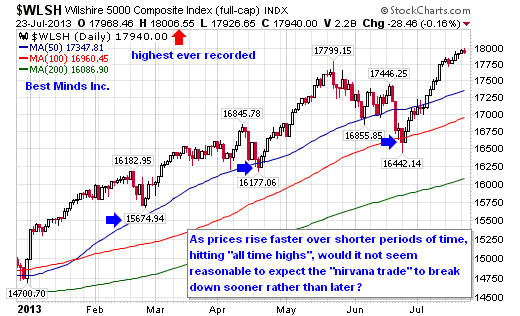

After touching its 100-day moving average, the Wilshire 5000 started up again. As of the close of business on Tuesday, July 23rd, the Wilshire has reached 18,000 for the first time in the history of American markets. Its climb between the June 24th low and this price level has taken 20 trading days, thus producing a daily average price increase faster than its previous run into its May 22nd high.

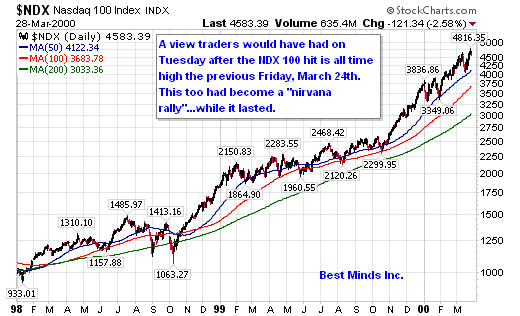

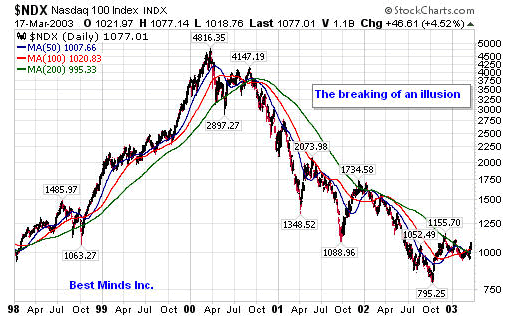

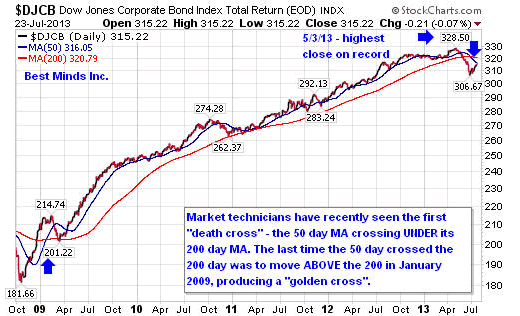

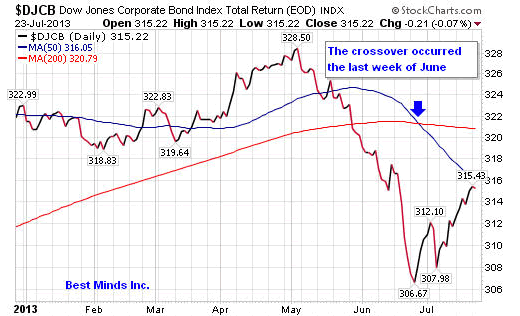

2000 and 2013 - Both are Warning US Stock Investors Now

In case this still appears purely academic, let's look at four more charts; two of the NASDAQ 100 - one in March 2000 and the other three years later - and two different views of the Dow Jones Corporate Bond Index, which on May 3, 2013, reached its highest level on record.

Even material written 18 months ago by bankers outside of Wall Street, supports the fact that the REAL world of finance has not been signaling a nirvana trade for some time now.

"We currently live in a world of extraordinary levels of government intervention and manipulation of the global market economy. Tax credits, credit facilities, foreign currency interventions and 'voluntary haircuts' on foreign bonds are government attempts to postpone inevitable market corrections." Economic Uncertainty, Texas Banking, January 2012, pg 9

May we all remember, when everyone is doing the same trade, then it is time to look in a different direction. The great trades made by contrarians were never from following the crowd.

See the original article >>

{kind=link}

{kind=link}