By Paul Dobson and Inyoung Hwang

Stocks surged, with the Standard & Poor’s 500 Index climbing to its highest closing level ever, and metals gained as the dollar slid after Federal Reserve Chairman Ben S. Bernanke called for maintaining stimulus.

The S&P 500 rose 1.4% to 1,675.03 at 4 p.m. in New York while emerging-market stocks advanced the most in almost 10 months. Treasuries rose and gold futures rallied 3% for a fourth straight advance, the longest winning streak since April. Bloomberg’s Dollar Index, a gauge of the currency against 10 major peers, sank 1.4%. Portugal’s PSI 20 Index slid 2% and the nation’s bonds slid amid concern a political crisis will persist.

Bernanke said yesterday that “highly accommodative monetary policy for the foreseeable future is what’s needed” and minutes of the Fed’s June meeting showed officials want to see more signs of job growth before starting to scale back their $85 billion-a-month bond purchases. About $5.3 trillion was erased from global equities between May 21 and June 24 after Bernanke signaled that the central bank could start tapering asset purchases this year.

“Everyone realizes that Fed policy is going to remain extraordinarily accommodative,” Hank Smith, who oversees $7 billion as chief investment officer at Radnor, Pennsylvania- based Haverford Trust Co., said by telephone. “The market has adjusted to this and we’re back to where we were prior to the Fed’s announcement of what was really a very subtle shift in policy.”

Rally Extended

The S&P 500 rose for a sixth straight day, its longest rally since March, with trading volumes 8% higher than the 30-day average at this time of day. The benchmark index has recouped all of a 5.8% slide from May 22 to June 24 triggered after Bernanke told Congress the Fed could taper its bond purchases if the economy continues to improve. The Nasdaq-100 Index has climbed for 12 straight sessions, the longest rally in three years.

All 10 of the main industry groups in the S&P 500 advanced, with technology, utility and commodity companies leading gains. Freeport-McMoRan Copper & Gold Inc. and Newmont Mining Corp. rose at least 4.6% as gold rallied. Advanced Micro Devices Inc. rose 12% as analysts recommended that investors buy the shares.

Microsoft Corp. jumped 2.8% after saying it is reorganizing into fewer units and shuffling senior management roles to speed development of hardware and Web-based services.

Market Movers

Intel Corp. and Walt Disney Co. also climbed more than 2.5% to lead the Dow Jones Industrial Average up 169.41 points to 15,461.07 as the 30-stock gauge reclaimed a record high on a closing basis for the first time since May. The Russell 2000 Index of smaller U.S. companies jumped 1.3% to reach a record for a fifth straight day.

Benchmark 10-year Treasury yields declined 5.4 basis points to 2.57%, after climbing to 2.75% earlier this week, the highest since August 2011. German 10-year bond yields fell four basis points to 1.62%.

The number of Americans filing for unemployment benefits unexpectedly increased to a two-month high of 360,000 last week, Labor Department figures showed. The median forecast of 47 economists surveyed by Bloomberg called for a drop to 340,000. Claims are difficult to adjust in July for seasonal events such as vehicle plant shutdowns and the Independence Day holiday, a Labor Department spokesman said as the data were released.

Fed Minutes

Minutes of the Fed’s June meeting showed about half of the 19 participants in the Federal Open Market Committee wanted to halt the central bank’s bond-buying program by year end. The minutes also showed many wanted to see more signs that employment is improving before backing a reduction in the pace of asset purchases. Data last week showed U.S. employers added 195,000 jobs last month, beating the increase of 165,000 predicted by economists.

About three stocks climbed for every one that dropped in the Stoxx Europe 600 Index, which advanced 0.6%. A gauge of mining companies rallied 3.9%, its biggest gain since January. BHP Billiton Ltd. and Rio Tinto Group, the world’s two largest commodity producers, rose more than 4.5% each.

Associated British Foods Plc jumped 5.1% after reporting that sales grew 20% at its Primark clothing business in the 16 weeks to June 22.

Portugal Banks

Portugal’s Banco Comercial Portugues SA and Banco BPI SA lost more than 6% in Lisbon. Portugal’s President Anibal Cavaco Silva used a televised speech last night to call for the end of the country’s bailout program in June 2014 to coincide with the start of the process leading to new elections. Yields on the nation’s 10-year bonds rose 13 basis points to 6.90%.

The MSCI Emerging Markets Index added 3.1%, the most since Sept. 14 on a closing basis. China’s stocks advanced the most since Dec. 14 as lenders rallied on speculation the government will take measures to bolster economic growth. Ping An Bank Co. and China Minsheng Banking Corp. jumped more than 9%, helping the Shanghai Composite Index rise 3.2%.

The cost of insuring against losses on corporate bonds dropped, with the Markit iTraxx Europe Index of credit-default swaps on 125 investment-grade companies falling 3.7 basis points to 105.66.

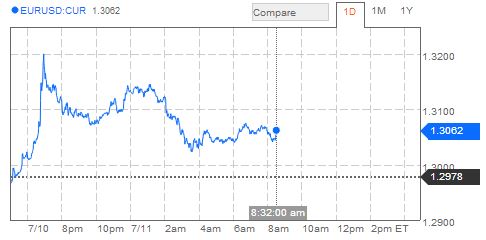

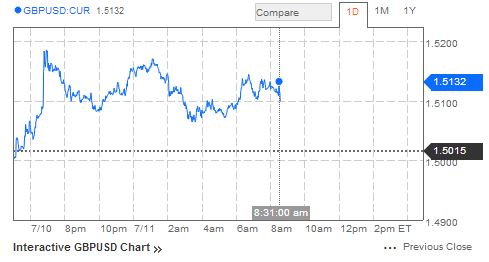

The dollar weakened against 15 of its 16 major peers as the Bloomberg Dollar Index sank to its lowest level since June 25. The euro gained for a second day, climbing 1% to $1.3109. South Korea’s won climbed 0.9% versus the dollar after the Bank of Korea held its benchmark seven-day repurchase rate unchanged at 2.5% for a second straight month today.

Yen, Rupee

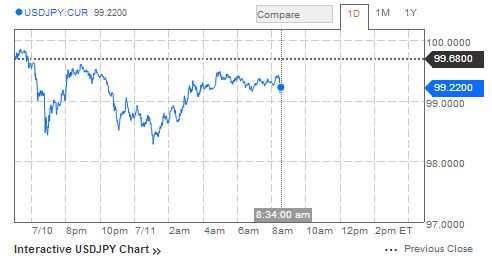

The yen strengthened 0.8% to 98.90 per dollar after the Bank of Japan said at the end of its two-day meeting today it would retain its plan for monetary stimulus.

The Indian rupee was little changed at 59.68 per dollar. The central bank may impose further curbs on rupee trading by lowering lenders’ net open position limits, according to a person with knowledge of the matter, who asked not to be identified because the information is confidential. They were referring to the amount of foreign-exchange contracts that investors can hold without opposing trade covers.

Silver for September delivery jumped 5.1% to $20.14 an ounce and gold and copper gained at least 2.5%. West Texas Intermediate oil fell 1.5% to $104.91 a barrel after rising to a 15-month high of $107.45 a barrel earlier. The S&P GSCI gauge of 24 commodities lost 0.4% after seven straight gains.