By Michael Pettis

Last month’s award of the Nobel Price in economics set off a great deal of chortling because one of the three recipients, Eugene Fama, received the award for saying that markets are efficient at capital allocation and another, Robert Schiller, received the award for saying they are not. Typical is this response by John Kay:

The Royal Swedish Academy of Sciences continues to astonish the public when awarding the Nobel Memorial Prize in Economics. In 2011 it celebrated the success of recent research in promoting macroeconomic stability. This year it pays tribute to the capacity of economists to predict the long-run movement of asset prices.

People with knowledge of financial economics may be further surprised that this year Eugene Fama and Robert Shiller are both recipients. Prof Fama made his name by developing the efficient market hypothesis, long the cornerstone of finance theory. Prof Shiller is the most prominent critic of that hypothesis. It is like awarding the physics prize jointly to Ptolemy for his theory that the Earth is the centre of the universe, and to Copernicus for showing it is not.

To me, much of the argument about whether or not markets are efficient misses the point. There are conditions, it seems, under which markets seem to do a great job of managing risk, keeping the cost of capital reasonable, and allocating capital to its most productive use, and there are times when clearly this does not happen. The interesting question, in that case, becomes what are the conditions under which the former seems to occur.

I wrote about this most recently in my most recent book about China, Avoiding the Fall, and I think it might be useful to recap that argument. I argued in the book (based on some articles I published in 2004-05) that an “efficient” market is one that has an efficient mix of investment strategies. Without this efficient mix, the market itself fails in its ability to allocate capital productively at reasonable costs.

Investors make buy and sell decisions for a wide variety of reasons, and when there is a good balance in the structure of their decision-making, financial markets are stable and efficient. But there are times in which investment is heavily tilted toward a particular type of decision, and this can undermine the functioning of the markets.

To see why this is so, it is necessary to understand how and why investors make decisions. An efficient and well-balanced market is composed primarily of three types of investment strategies—fundamental investment, relative value investment, and speculation—each of which plays an important role in creating and fostering an efficient market.

- Fundamental investment, also called value investment, involves buying assets in order to earn the economic value generated over the life of the investment. When investors attempt to project and assess the long-term cash flows generated by an asset, to discount those cash flows at some rate that acknowledges the riskiness of those projections, and to determine what an appropriate price is, they are acting as fundamental investors.

- Relative value investing, which includes arbitrage, involves exploiting pricing inefficiencies to make low-risk profits. Relative value investors may not have a clear idea of the fundamental value of an asset, but this doesn’t matter to them. They hope to compare assets and determine whether one asset is over- or underpriced relative to another, and if so, to profit from an eventual convergence in prices.

- Speculation is actually a group of related investment strategies that take advantage of information that will have an immediate effect on prices by causing short-term changes in supply or demand factors that may affect an asset’s price in the hours, days, or weeks to come. These changes may be only temporarily and may eventually reverse themselves, but by trading quickly, speculators can profit from short-term expected price changes.

Each of these investment strategies plays a different and necessary role in ensuring that a well-functioning market is able keep the cost of capital low, absorb financial risks, and allocate capital efficiently to its more productive use. A well-balanced market is relatively stable and allocates capital in an efficient way that maximizes long-term economic growth.

Each of the investment strategies also requires very different types of information, or interprets the same information in different ways. Speculators are often “trend” traders, or trade against information that can have a short-term impact on supply or demand factors. They typically look for many opportunities to make small profits. When speculators buy in rising markets or sell in falling ones—either because they are trend traders or because the types of leverage and the instruments they use force them to do so—their behavior, by reinforcing price movements, adds volatility to market prices.

Different Investors Make Markets Efficient

Value investors typically do the opposite. They tend to have fairly stable target price ranges based on their evaluations of long-term cash flows discounted at an appropriate rate. When an asset trades below the target price range, they buy; when it trades above the target price range, they sell.

This brings stability to market prices. For example, when higher-than-expected GDP growth rates are announced, a speculator may expect a subsequent rise in short-term interest rates. If a significant number of investors have borrowed money to purchase securities, the rise in short-term rates will raise the cost of their investment and so may induce them to sell, which would cause an immediate but temporary drop in the market. As speculators quickly sell stocks ahead of them to take advantage of this expected selling, their activity itself can force prices to drop. Declining prices put additional pressure on those investors who have borrowed money to purchase stocks, and they sell even more. In this way, the decline in prices can become self-reinforcing.

Value investors, however, play a stabilizing role. The announcement of good GDP growth rates may cause them to expect corporate profits to increase in the long term, and so they increase their target price range for stocks. As speculators push the price of stocks down, value investors become increasingly interested in buying until their net purchases begin to stabilize the market and eventually reverse the decline.

Relative value investors or traders play a different role. Like speculators, they tend not to have long-term views of prices. However, when any particular asset is trading too high (low) relative to other equivalent risks in the market, they sell (buy) the asset and hedge the risk by buying (selling) equivalent securities.

A well-functioning market requires all three types of investors for socially useful projects to have access to appropriately-priced capital.

- Value investors allocate capital to its most productive use.

- Speculators, because they trade frequently, provide the liquidity and trading volume that allows value investors and relative value traders to execute their trades cheaply. They also ensure that information is disseminated quickly.

- Relative value trading forces pricing consistency and improves the information value of market prices, which allows value investors to judge and interpret market information with confidence. It also increases market liquidity by combining several different, related assets into a single market. When buying of one asset forces its price to rise relative to that of other related assets, for example, relative value traders will sell that asset and buy the related assets, thus spreading the buying throughout the market to related assets. It is because of relative value strategies that we can speak of a unified market for different assets.

Without a good balance of all three types of investment strategies, financial systems lose their flexibility, the cost of capital is likely to be distorted, and the markets become inefficient at allocating capital. This is the case, for example, in a market dominated by speculators. Speculators focus largely on variables that may affect short-term demand or supply for the asset, such as changes in interest rates, political and regulatory announcements, or insider behavior.

They ignore information like growth expectations or new product development whose impact tends to reveal itself only over long periods of time. In a market dominated by speculators, prices can rise very high or drop very low on information that may have little to do with economic value and a lot to do with short-term, non-economic behavior.

Value investors keep markets stable and focused on profitability and growth. For value investors, short-term, non-economic variables are not an important or useful type of information. They are more confident of their ability to discount economic variables that develop and affect cash flows over the long term. Furthermore, because the present value of future cash flows is highly susceptible to the discount rate used, these investors tend to spend a lot of effort on developing appropriate discount rates. However, a market consisting of only value investors is likely to be illiquid and pricing-inconsistent. This would cause an increase in the required discount rate, thus raising the cost of capital for borrowers.

Because each type of investor is looking at different information, and sometimes analyzing the same information differently, investors pass different types of risk back and forth among themselves, and their interaction ensures that a market functions smoothly and provides its main social benefits. Value investors channel capital to the most productive areas by seeking long-term earning potential, and speculators and arbitrage traders keep the cost of capital low by providing liquidity and clear pricing signals.

Where Are the Value Investors?

Not all markets have an optimal mix of investment strategies. China, for example, does not have a well-balanced investor base. There is almost no arbitrage trading because this requires low transaction costs, credible data, and the legal ability to short securities. None of these is easily available in China.

There are also very few value investors in China because most of the tools they require, including good macro data, good financial statements, a clear corporate governance framework, and predictable government behavior, are missing. As a result, the vast majority of investors in China tend to be speculators. One consequence of this is that local markets often do a poor job of rewarding companies for decisions that add economic value over the medium or long term. Another consequence is that Chinese markets are very volatile.

Why are there so few value investors in China and so many speculators? Some experts argue that this is because of the lack of investors with long-term investment horizons, such as pension funds, that need to invest money today for cash flow needs far off in the future. Others argue that very few Chinese investors have the credit skills or the sophisticated analytical and risk-management techniques necessary to make long-term investment decisions. If these arguments are true, increasing the participation of experienced foreign pension funds, insurance companies, and long-term investment funds in the domestic markets, as Beijing has done with its QFII program, is certainly seems like a good way to make capital markets more efficient.

But the issue is more complex than that. China, after all, already has natural long-term investors. These include insurance companies, pension funds, and, most important, a very large and remarkably patient potential investor base in its tens of millions of individual and family savers, most of whom save for the long term. China also has a lot of professionals who have trained at the leading U.S. and UK universities and financial institutions, and they are more than qualified to understand credit risk and portfolio techniques. So why aren’t Chinese investors stepping in to fill the role provided by their counterparts in the United States and other rich countries?

The answer lies in what kind of information can be gathered in the Chinese markets and how the discount rates used by investors to value this information are determined. If we broadly divide information into “fundamental” information, which is useful for making long-term value decisions, and “technical” information, which refers to short-term supply and demand factors, it is easy to see that the Chinese markets provide a lot of the latter and almost none of the former. The ability to make fundamental value decisions requires a great deal of confidence in the quality of economic data and in the predictability of corporate behavior, but in China today there is little such confidence.

How to develop the investor base

Furthermore, regulated interest rates and pricing inefficiencies make it nearly impossible to develop good discount rates. Finally, a very weak corporate governance framework makes it extremely difficult for investors to understand the incentive structure for managers and to be confident that managers are working to optimize enterprise or market value.

And yet, when it comes to technical information useful to speculators, China is too well endowed. Insider activity is very common in China, even when it is illegal. Corporate governance and ownership structures are opaque, which can cause sharp and unexpected fluctuations in corporate behavior. Markets are illiquid and fragmented, so determined traders can easily cause large price movements. In addition, the single most important player in the market, the government, is able—and very likely—to behave in ways that are not subject to economic analysis.

This has a very damaging effect on undermining value investment and strengthening speculation. In the first place, unpredictable government intervention causes discount rates to rise, because value investors must incorporate additional uncertainty of a type they have difficulty evaluating.

Second, it puts a high value on research directed at predicting and exploiting short-term government behavior, and thereby increases the profitability of speculators at the expense of other types of investors. Even credit decisions must become speculative, because when bankruptcy is a political decision and not an economic outcome, lending decisions are driven not by considerations of economic value but by political calculations.

China is attempting to improve the quality of financial information in order to encourage long-term investing, and it is trying to make markets less fragmented and more liquid. But although these are important steps, they are not enough. Value investors need not just good economic and financial information, but also a predictable framework in which to derive reasonable discount rates. And here China has a problem.

There are several factors, besides the poor quality of information, that cause discount rates to be very high. These include market manipulation, insider behavior, opaque ownership and control structures, and the lack of a clear regulatory framework that limits the ability of the government to affect economic decisions in the long run. This forces investors to incorporate too much additional uncertainty into their discount rates.

Chinese value investors, consequently, use high discount rates to account for high levels of uncertainty. Some of this uncertainty represents normal business uncertainty. This is a necessary component of an economically efficient discount rate, since all projects have to be judged not just on their expected return but also on the riskiness of the outcome. But Chinese investors must incorporate two other, economically inefficient, sources of uncertainty. The first is the uncertainty surrounding the quality of economic and financial statement information. The second is the large variety of non-economic factors that can influence prices.

This is the crucial point. It is not just that it is hard to get good economic and financial information in China. The problem is that even when information is available, the variety of non-economic factors that affect value force the appropriate discount rate so high that value investors are priced out of the market.

Speculators, however, are much more confident about the value of the information they use. Furthermore, because their investment horizon tends to be very short, they can largely ignore the impact of high implicit discount rates. As a result, it is their behavior that drives the whole market. One consequence is that capital markets in China tend to respond to a very large variety of non-economic information and rarely, if ever, respond to estimates of economic value.

During the past decade, Beijing was betting that increasing foreign participation in the domestic markets would improve the functioning of the capital markets by reducing the bad habits of speculation and increasing the good habits of value investing and arbitrage. But it has become pretty clear that this faith was misplaced: the market is as speculative and inefficient as ever. This should not have been a surprise. The combination of very weak fundamental information and structural tendencies in the market—such as heavy-handed government interventions and market manipulation—reward speculative trading and undermine value investing. This forces all investors to focus on short-term technical information and to behave speculatively. In China even Warren Buffett would speculate.

Investors in Chinese markets must be speculators if they expect to be profitable. As long as this is the case, investors will not behave in a way that promotes the most productive capital allocation mechanism in the market, and such efforts as bringing in foreigners will have no meaningful impact.

What China must do is something radically different. It must downgrade the importance of speculative trading by reducing the impact of non-economic behavior from government agencies, manipulators, and insiders. It must improve corporate transparency. It must continue efforts to raise the quality of both corporate reporting and national economic data. Finally, it must deregulate interest rates and open up local markets to permit arbitragers to enforce pricing consistency and to allow better estimates of appropriate discount rates.

If done correctly, these changes would be enough to spur a major transformation in the way Chinese investors behave by permitting them to make long-term investment decisions. It would reduce the profitability of speculative trading and increase the profitability of arbitrage and value investing, and so encourage a better mix of investors. If China follows this path, it would spontaneously develop the domestic investors that channel capital to the most productive enterprise. Until then, China’s capital markets, like those of many countries in Latin America and Asia, will be poor at allocating capital.

When efficient markets become inefficient

But this is not just an issue for China. In the US there have been times when markets seemed efficient and rational, and times when they clearly were not. Of course this cannot be explained by the disappearance of the tools needed by value investors – for example the market for internet stocks seemed rational in the early 1990s and clearly became irrational by the late 1990s, but this did not occur, I would argue, because fundamental investors were suddenly deprived of their analytical tools.

What happened instead, I would argue, is that conditions that led to a too-rapid expansion of liquidity at excessively low interest rates changed the environment in which fundamental investors could operate. As excess liquidity forced up asset prices, the likes of Warren Buffet found themselves unable to justify buying assets and so they dropped out of the market. As they did, the mix of investment strategies shifted until the market became dominated by speculators, and when this happened what drove prices was no longer the capital allocation decision of value investors but rather than short-term expectations of changes in demand and supply factors that characterize a highly speculative market.

This, I would argue, made the US stock market of the late 1990s (and perhaps today, too) “irrational”, not because they are fundamentally irrational or inefficient but rather because they can only function efficiently with the right mix of investment strategies. When the mix was altered – and this can happen when liquidity is too abundant, or when a sudden shock undermines the confidence value investors have in their ability to analyze data, or when a political event cause uncertainty to rise so high that value investors are priced out of the market, or for a number of other reasons – the markets stopped functioning as they should.

Perhaps what I am saying is intuitively obvious to most traders or investors, but it seems to me that it suggests that the argument about whether markets are efficient or not misses the point. There are certain conditions under which markets are efficient because the tools needed for each of the various investment strategies are widely available and ate credible. When those conditions are not met, because the tools are not available, or when they are temporarily overwhelmed by exogenous events, perhaps because the credibility of those tools are temporarily undermined, or when excess liquidity causes fundamental investors to drop out, markets cannot be efficient.

See the original article >>

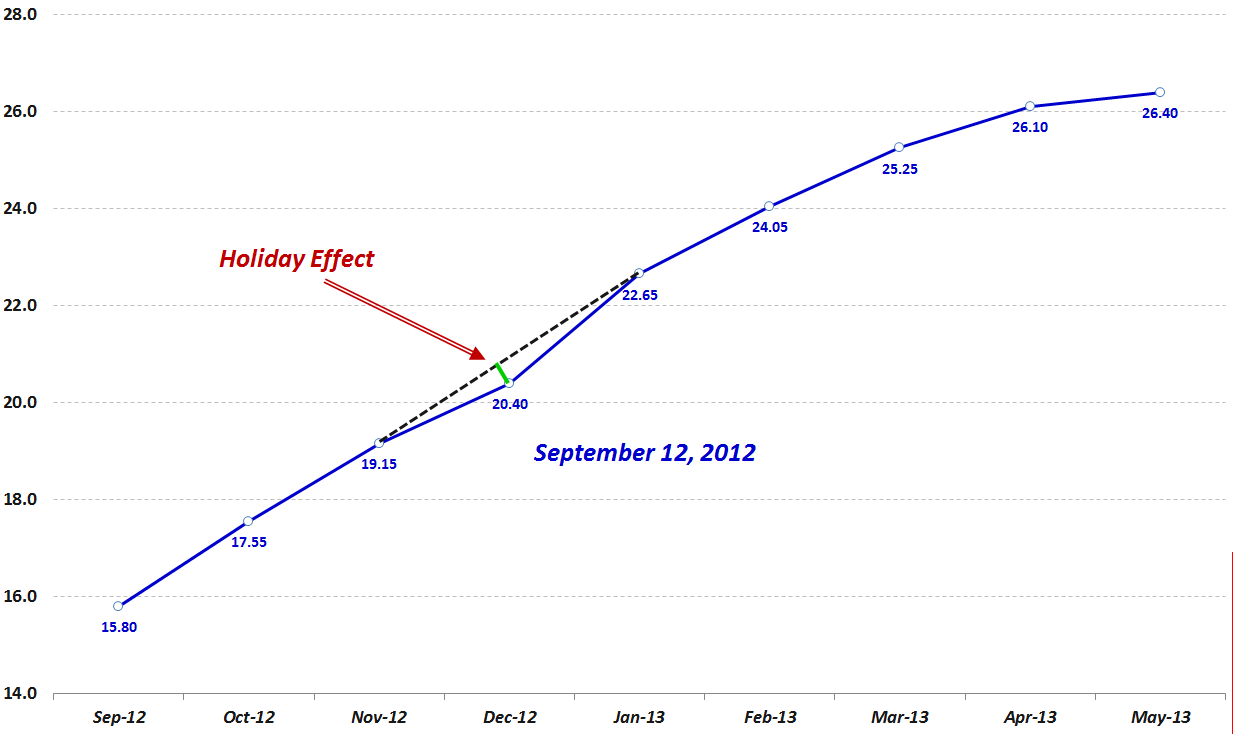

Source: Bloomberg

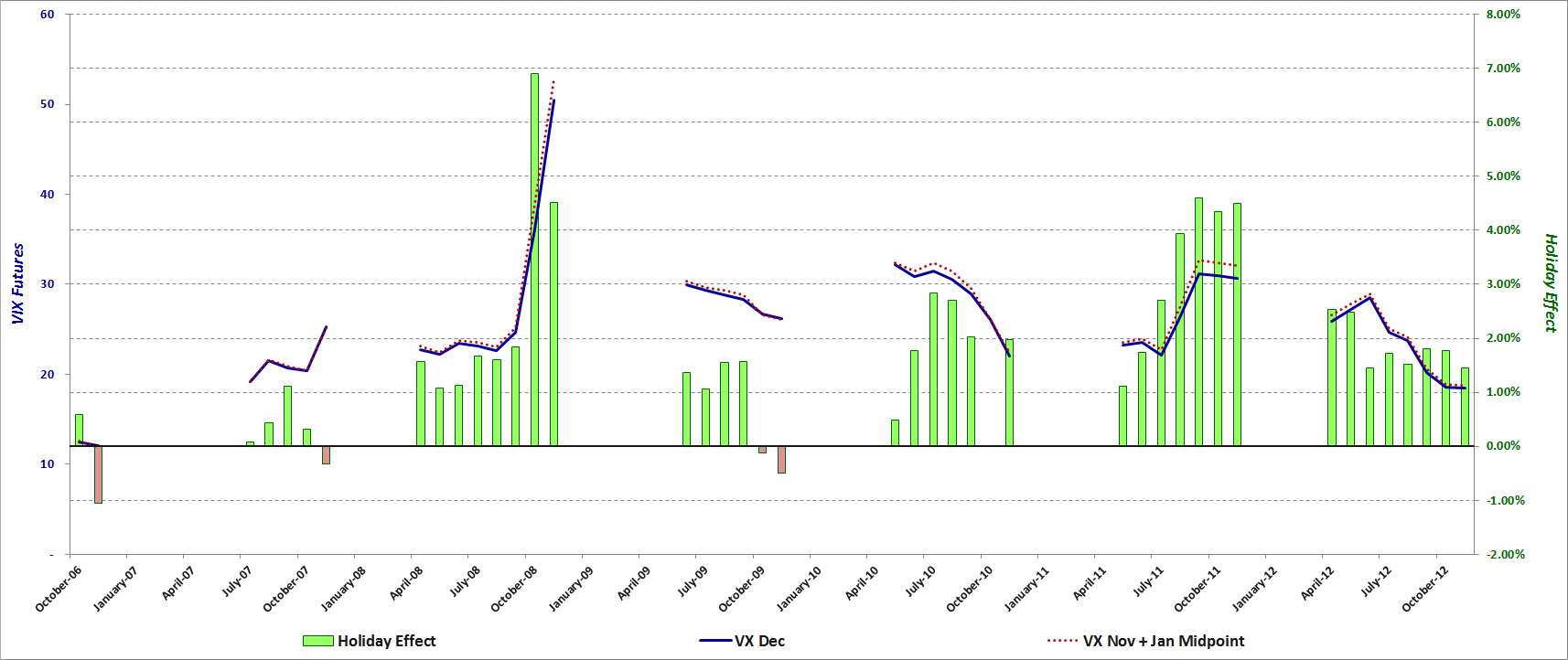

Source: Bloomberg