By: Kevin Flynn

Last week, I took on the market's general belief in global central bank stimulus as a de facto guarantee of stock prices. The concluding assertion was "Central bank stimulus is not an invisible force field against adversity." Two weeks prior to that, I warned that Mr. Market might have some surprises in store for stock prices in the coming months, particularly during the period between Labor Day and Thanksgiving (a refinement upon the "eight weeks or so" estimate I originally gave). It seems appropriate to re-examine those assertions in light of recent developments, with a particular eye towards the markets.

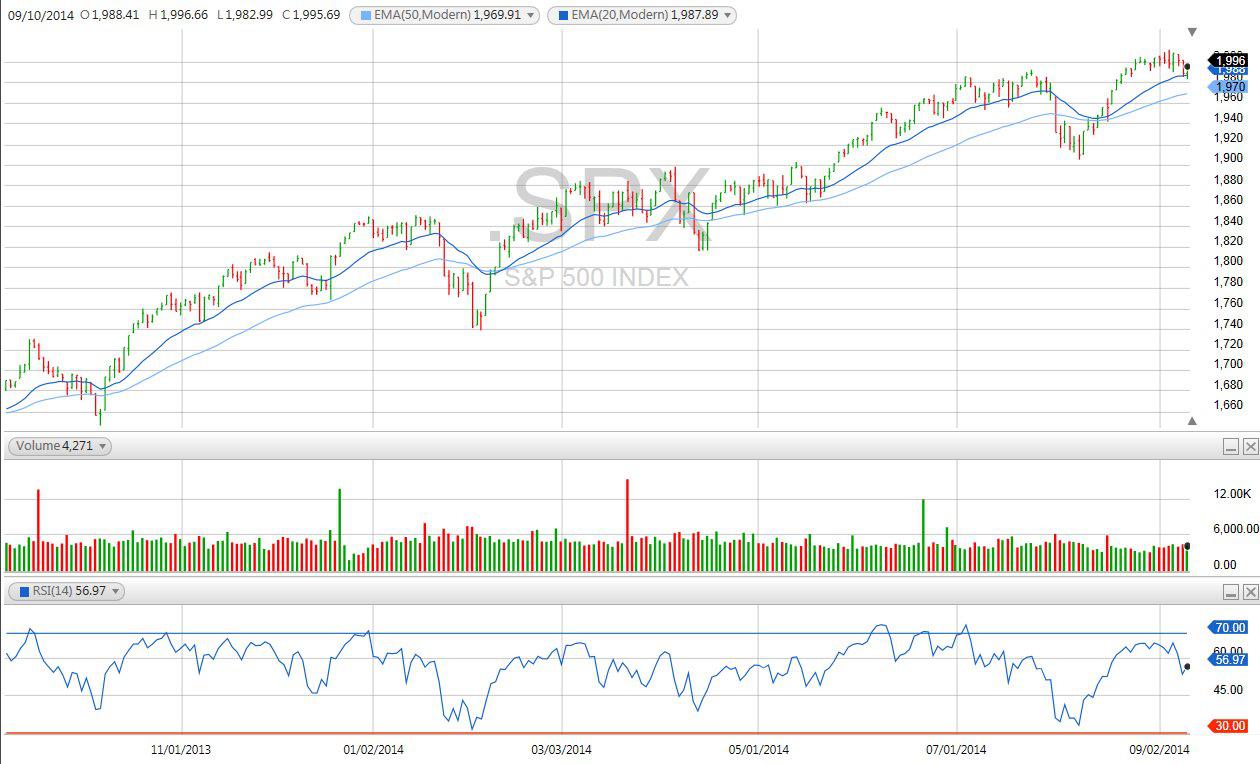

The stock market passed its first September test on Monday and Tuesday with a smooth bounce off the 20-day exponential moving average (EMA) on the S&P 500. It was particularly impressive on Tuesday morning, when prices pulled off a reversal seemingly out of thin air. Playing the rebound off the 20-day has been the percentage bet over the last two years, as the market has rarely spent much time below it. Most tests of the 20-day average have consisted of hovering for a day or so and then resuming the upward climb, as was apparently the case this week.

(click to enlarge)

The roughly ten-day prelude to our traditional back-to-school holiday is also the stock market's "silly season," when prices usually rally several percent on little more than the effect of junior clerks being buoyant (if limited) buyers while their seniors are all on holiday. It's the same vacation break as the all-too-brief one that places policymakers on hold from mischief-making, resulting in a benign news tape. That little pop is usually followed by early September weakness, and indeed, is probably the main reason why the average performance for the month is slightly negative.

This year's 1% pullback to the 20-day EMA feels like a rather modest move by post-Labor Day standards, and the quick rebound suggests that the upward momentum trend is indeed still intact. Put another way, the market has yet to get truly worried about much of anything - it couldn't find the 200-day EMA these days with a pick and shovel (the last visit there coming in the wake of the market's post-Obama re-election tantrum).

A word of caution on Mr. Market, though - the August rally off the QE trend line was on very light volume. That doesn't guarantee that the tape is about to make a big move downward, only that sentiment is flimsier than it looks, and more susceptible to exaggerated swings. A great deal is being written about how strong the stock market is this year that ignores the fact that more than half the gains have come in the last few weeks, on little news and even less volume.

The market still has a lot to get through before Thanksgiving can kick off the sacred tradition of the end-of-the-year rally. Scotland has been rattling global markets, with polls showing it might just vote "yes" on independence after all. My guess is that it will all turn out like the Greek vote a couple of years ago - a narrow cling to the status quo providing a rally in relief from the chasm that a secession victory would open up. I'm not making any bets in either direction, but if "yes" wins, look out below.

On the heels of the Scot vote comes the all-important Fed meeting next week. During the bull market, the pattern for stock prices around Fed meetings is to rally into them and then sell off afterwards. This time around might provide the reverse, as fears of what the central bank might say about tightening could lead to selling in advance of the meeting, followed by a relief rally afterwards. I'm not making predictions about what the Fed will say or do, mind you, only that the market is getting hit with a lot of warnings about potential sell-offs in advance of the meeting. With that much time to prepare, the market often ends up selling the rumor and buying the news. Should we get more evidence of a tightening bias, an initial sell-off followed by a big rip-reversal rally ("it could have been worse") would be classic Wall Street.

There's more going on than Scotland and the Fed. If famed investor Sam Zell and I were to have dinner and talk about anything but investments and what a nice city Chicago is, we'd probably come to blows. That said, I do respect his investment acumen, and we could have a fine time doing nothing but talking about what to buy and sell. Last week on CNBC, he made some observations that put me in mind of his 2007 posture: one, the stock market seemed an awful lot more elevated than the economy; two, he had never seen so many global uncertainties in his investing career; and most importantly, three: he has more fingers on his hand than he needs to count buying opportunities. That should worry you.

The Ukraine situation is going smoothly: Putin takes what he wants, and then we all breathe a sigh of relief when he goes back home after getting it. I'm not sure of the logic of this. But the situation isn't going to go away so easily, especially after President Obama made a point of stressing American backing of the Ukrainian people in his address on the violent Islamic extremist group ISIL, yet another potential source of instability (I don't know about you, but I'm crossing my fingers for Thursday the 11th).

Bear capitulation is another sign of impending volatility. There's been a rash of bailing bears lately, from Deutsche Bank's David Bianco, to my own surprise, Gina Martin Adams at Wells Fargo. I can't think of any Street bears still alive right now (I don't count anyone who manages a gold fund), and that is never something I like to see. The this-time-it's-different excuse-theory starting to make the rounds is that because the recovery was half-strength GDP-wise, it will last twice as long. Of course it will. The only consolation is that there's usually a time lapse of some months before the last capitulator finds occasion to regret his or her words.

Bond whiz Jeff Gundlach weighed in on CNBC during the week with an observation in line with what I have been saying since last fall - the Fed is out of ammunition to fight economic setbacks (though the bank would never admit as much). Gundlach made the remark in the context of it being the only possible sane reason for a rate hike, as otherwise, the economy is in for another rerun of 2% GDP that he doesn't see changing. Despite the Fed's exaggerated fearfulness about financial instability, I too see this as the main reason for raising rates - that, and the unemployment rate, which is surely going to be below 6% in 2015, if not before.

The August jobs report and the July JOLTS report both point to the same thing, in my opinion - the labor market is starting to peak. The apparent August weakness was not as bad as it looked, and the jobs data, claims data and JOLTS all point to a labor market that will top out next year. The Fed can't afford to be caught empty-handed.

Another big reason for raising rates is the restoration of normalcy (or an approximation thereof) in investing behavior. I don't know if anyone can definitely say what short rates would be without central bank intervention, but my guess is that the curve would look more like 1%-1.5% at the front end and 3%-4% at the long end. I don't think that those rates would impede economic growth at all, though I do concede that the transition to those rates will likely cause some financial system dislocations. The question that doesn't get enough mainstream attention, and the one that Gundlach perhaps should be asking is, why does the Fed have a lid on short rates at 0%-0.25% with an unemployment rate of only 6.1%? And its balance sheet is over $4 trillion?

That's the part that bothers me the most, because the ultra-low rate policy is without question creating asset price bubbles. The stock market is overvalued, but if you really want to know where the bubble is, it's in high-yield bonds, the proverbial elephant in the room that no one wants to talk about. We have effectively transferred the credit bubble from mortgage-backed bonds to the corporate high-yield sector.

German airline, Lufthansa, which has a junk rating from Moody's, sold five-year bonds Friday priced at 1.125% in an offering that was heavily oversubscribed. That's ridiculous. That's no amber light, it's a giant flashing red billboard. The bonds will be safe for a time yet, I readily concede. But once rates start to move back up, we are going to be faced with a world where everyone wants to unload a Mt. Everest of high-yield bonds and no one wants to buy them. All sellers and no buyers - that's a bond market recipe for financial system disaster. Didn't anyone see it coming?

No comments:

Post a Comment