Summary

- Since the banking collapse in 2008 leading to the global depression, fines, penalties and settlements levied on banks for criminal acts have increased.

- Will these growing costs be enough to deter banks from future criminal activity?

- These issues are addressed along with some thoughts for anyone considering bank stock purchases.

Elliott R. Morss ©All Rights Reserved

Introduction

In 1999, Sandy Weill, supported by a coterie of other bankers and lobbyists, got the US Congress to repeal Glass-Steagall. That Act had kept depository institutions safe since the '30s. With restrictions removed, US banks purchased, packaged and traded mortgages and their derivatives. In late-2008, the market for these financial packages disappeared resulting in the US banking collapse and the largest global depression since 1929.

Some claim there were other reasons for the '08 Depression. I argue that the banks losing track of what was actually in the mortgage packages they were selling was the primary reason the market for mortgage-backed securities suddenly disappeared. And this in turn led to the bank collapse et al.

Were the banks that caused the collapse acting legally? Apparently not. While the wheels of justice turn slowly, there have recently been a number of large fines and settlements won by governments and private firms against the largest banks. In most of the settlements, the banks have not conceded wrong-doing. Hard to believe - why would Bank of America (NYSE:BAC) agree to pay the Feds nearly $17 billion if they did nothing wrong? The answer: Bank of America committed numerous criminal acts. But admitting it would open the bank up to even more lawsuits and the Feds settled because they know how expensive lawsuits against the big banks can be.

This article provides detail on big bank crimes along with some thoughts on whether these large fines and settlements will be adequate to keep the banks in check going forward.

The Crimes Committed

There is long list. The crimes generating the largest penalty fees/settlements are:

- Mortgage foreclosure abuses;

- Fraud - misleading information on mortgage-related securities;

- Money laundering;

- Manipulating LIBOR and other prices; and

- Tax evasion.

a. Foreclosure Abuses

In frenzied efforts to make money on the trading of mortgage securities, large banks lost track of who actually had title to properties underlying mortgages they wrote, bought, packaged, and sold off. Banks engaged in criminal acts when they initiated foreclosures on properties they did not own or know who did.

b. Fraud

Numerous settlements have been won against the large banks for fraudulent misrepresentations of the mortgage security packages they were selling. Goldman (NYSE:GS) actually urged its clients to buy mortgage packages while selling off its own holdings of the same securities. And while the banks were certainly at fault for fraud, it should be kept in mind that the buyers should have known better. Many of these packages were brought by the Federal Housing Finance Agency and its "offsprings" Fannie Mae and Freddy Mac. The well-paid officers of the Federal agencies buying this stuff should either have known or found out what they were getting before making the purchases. The reality is that as long as large commissions were made on these transactions, neither buyers nor sellers cared about product quality.

c. Money Laundering

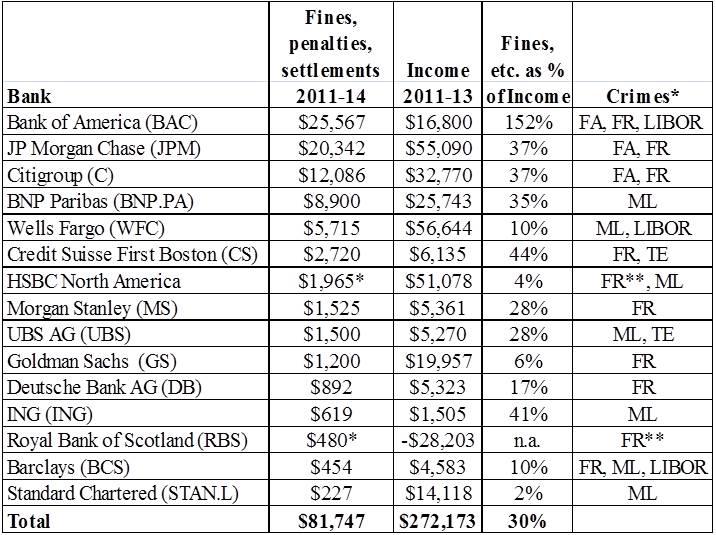

The US had financial sanctions in place against Burma, Cuba, Iran, Libya, and Sudan. The sanctions said all banks doing business in the US should not conduct transactions for customers in these countries. The following banks got caught and the fines they agreed to pay are: BNP Paribas (BNP.PA) (OTC:BNPZY) - $8.9 billion, HSBC (NYSE:HSBC) - $2 billion, ING (NYSE:ING) - $619 million, Credit Suisse (NYSE:CS) - $536 million, Lloyds TSB Bank - $350 million, Barclays (NYSE:BCS) - $298 million, and Standard Chartered (STAN.L) (OTC:SCDRF) - $227 million.

d. Manipulating LIBOR and Other Prices

Large banks use depositors' monies to buy and sell huge blocs of financial assets. And they have used these funds to cause prices to rise and fall. Many have heard about the LIBOR scandal. But there have been others. For example, JPMorgan (NYSE:JPM) was fined $410 million for manipulating electricity prices in 2013.

e. Tax Evasion

For many years, Swiss banks aided Americans in avoiding US taxes. In recent years, the Swiss authorities reluctantly agreed to cooperate with the IRS on these matters. And not surprisingly, UBS agreed to pay a US fine of $780 million in 2009 for tax evading activities. But today, Switzerland is not alone. The Treasury reports that the Cayman Islands rank third behind the UK and Canada for US investments.

The Criminals

Table 1 provides data on the fines, penalties and settlements levied against the big banks. The final column gives fines, etc., for the 2011-14 period as a percent of reported income for 2011-13. There are several problems with these ratios1, but they are indicative of how significant the fines are relative to each bank's income.

Table 1. - Fines, Penalties, and Settlements Levied Against Large Banks

(in millions of US$)

(click to enlarge)

* Crimes: FA=Foreclosure Abuses; FR=Fraud; LIBOR = Manipulating Interest Rates and Prices;

ML=Money Laundering; TA=Aiding in Tax Evasion;

** Banks are in negotiation with Federal housing agencies - significant additional fines expected.

Sources: Newspaper reports and company SEC filings.

Do Fines Have Deterrent Effect?

There is no question that since the 2008 depression, a new regulatory era has started. And part of that are much higher penalties. But will they have the desired impact of reducing bank crime? I talked recently to a senior executive in one of the big US banks. He said: "Big banks are in the risk business. One of those risks is that either governments or private firms will take us to court. In deciding what to do, we have to consider that risk. However, the returns on some activities are high enough to risk lawsuits. And when they are, the penalties we incur will be viewed as a cost of doing business."

Take another look at Table 1 where fines are compared to banks' income. I don't care how large a bank is. When your fines exceed $1 billion, your stockholders will sooner or later take note. And the fines are not the only costs that banks incur for illegal acts. In 2013, Bank of America paid $2.9 billion in "Professional Fees" (I am sure a significant segment of this is for outside lawyers); JPMorgan's tab for said fees was $7.6 billion!

How About The Volcker Rule?

Paul Volcker, the former Federal Reserve Chief, has for some time argued that banks should not be allowed to trade using depositor assets. He points out that the Glass-Steagall Act did not allow it and we had no major bank problems while it was in force. A significant feature of the "true" Volcker Rule is that banks cannot sell off the loans/mortgages that they originated, but instead hold them to maturity. The "incentive effects" of adopting the Volcker Rule would be significant: instead of trying to maximize commission income from the sale of loan/mortgage packages (the driving force behind the 2008 collapse - nobody cared about the quality of loans), banks would instead focus on making sound loans.

At one point, Volcker had some influence in the White House. That ended when Larry Summers and Tim Geithner took over. Both Summers and Geithner, looking for paychecks from the finance industry in their next jobs, effectively eliminated Volcker's influence. However, Barney Frank and others in Congress insisted that the Dodd-Frank Bill does include a Volcker Rule. Unfortunately, just how it would be defined was left to the regulators. And the bank lobbyists have been at work. Open Secrets estimates that banks spent more than $60 million on lobbying in each of the last 3 years (2011-13).

So where are we today? I quote from the most recent JPMorgan annual report to the Security and Exchange Commission:

"On December 10, 2013, regulators adopted final regulations to implement the Volcker Rule. Under the final rules, "proprietary trading" is defined as the trading of securities, derivatives, or futures (or options on any of the foregoing) as principal, where such trading is principally for the purpose of short-term resale, benefiting from actual or expected short-term price movements and realizing short-term arbitrage profits or hedges of such positions. In order to distinguish permissible from impermissible principal risk taking, the final rules require the establishment of a complex compliance regime that includes the measurement and monitoring of seven metrics. The final rules specifically allow market-making-related activity, certain government-issued securities trading and certain risk management activities."

The banks' lobbyists have done a good job. The agreed-upon rule only applies to a segment of short-term trading. And "a complex compliance regime" that involves "seven metrics"? The banks will just hire a few more accountants and lawyers and again befuddle the regulators. And the banks have negotiated things so they will be able to "hedge". In sum, the banks got just about what they wanted, a very distant relative of the Volcker Rule.

In its SEC report, JPMorgan stated, "The Firm has ceased all prohibited proprietary trading activities." This is intended to convince the SEC and JPM's stockholders that the London Whale incident will not be repeated: speculative trading by a staffer in London that resulted in trading losses of $6.2 billion, and 2012 fines of $1 billion.

Senator John McCain made an apt comment on the incident: "JPMorgan's chief investment office increased risk by mislabeling the synthetic portfolio as a risk-reducing hedge when it was really involved in proprietary trading".

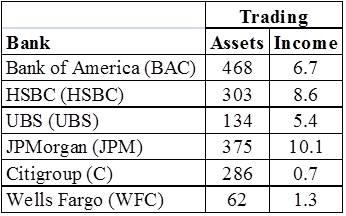

So will the "watered-down" version of the Volcker Rule have a meaningful impact? Table 2 provides data on the trading assets and income of banks at the end of 2103. It remains a big business and will continue as such.

Table 2. - Trading Assets and Income, Selected Banks

(bil. US$)

Source: SEC Submissions

Too Big To Fail - The Living Will Solution

Just after the 2008 bank collapse, there was considerable concern expressed about certain banks being "too big to fail". Congress's solution was to ask the big banks to write up plans for "orderly bankruptcies" that would not set off wider panics. This sounded like a dead-end, losing proposition from the start and it has proven to be just that. The banks have submitted their initial plans and the federal regulators have reacted. The Federal Deposit Insurance Corporation has determined that the living wills were "not credible." Thomas M. Hoenig, the vice chair of the FDIC, concluded: "Despite the thousands of pages of material these firms submitted, the plans provide no credible or clear path through bankruptcy that doesn't require unrealistic assumptions and direct or indirect public support."

The Only Thing That Will Make Banks Safe

We do not deposit money in banks so banks can gamble. We put money in banks for safe keeping. Depository institutions should not be allowed to trade any assets. Too risky. Let hedge funds, private equity funds, and venture capital funds take the risks. The simple and only solution that will make banks safe: limit FDIC insurance to banks that hold their own loans to maturity and do not engage in trading on their own accounts.

Investing in Big Banks

Given the bad press big banks have been getting, perhaps the best way to view them is like sin/vice investments. For example, the Vice Fund (VICEX)2 only invests in tobacco, alcohol, defense, and gambling companies. It has done well (5 year average return - 17.7%) .

There is an interesting literature on sin/vice investing3. In essence, the studies find that in the long run, sin stocks outperform the overall market. Why? Because some institutional investors shy away from sin stocks, sin industries have high entry barriers, and companies within sin sectors often have considerable pricing power.

However, you want to view large bank investments, I offer one recommendation: before investing in a big bank, take a look at its annual filing with the SEC. In particular, find and read the "Litigation" note to its Consolidated Financial Statements. For example, JPM's Litigation note appears on pg. 326-332 of its 2013 10-K Report to the SEC. It describes 37 major actions that have been investigated with numerous cases coming forth from them.

I end with a quote contained in JPM's Litigation note:

"The Firm has established reserves for several hundred of its currently outstanding legal proceedings….During the years ended December 31, 2013, 2012 and 2011, the Firm incurred $11.1 billion, $5.0 billion and $4.9 billion, respectively, of legal expense. There is no assurance that the Firm's litigation reserves will not need to be adjusted in the future."

1. The fines, etc. data reflect what has actually been settled on, either in court or in out-of-court settlements. Just when, how and if these fines, etc. will be collected remains uncertain. The banks set aside reserves (and in so doing, reduce income) for what they expect they will have to pay annually. That means their incomes are somewhat lower than they would have been in the absence of the fines, etc.

2. The "Vice Fund" was recently renamed the "USA Mutuals Barrier Investor Fund".

3. See F.J. Fabozzi, K.C. Ma, and B.J. Oliphant, "Sin Stock Returns", Journal of Portfolio Management, Fall, 2008, and H. Hong and M. Kacperczyk, "The Price of Sin: The Effects of Social Norms on Markets", Journal of Financial Economics, April, 2009.

No comments:

Post a Comment