Summary

- Many defensive assets are highly correlated to the broader stock market, offering at best the possibility of smaller losses.

- The best defensive move is to increase cash.

- Leveraged and short ETFs are high risk if timing is even slightly off.

- ETFs such as UUP offer upside potential during corrections, but less downside risk than short or leveraged ETFs.

There's isn't a single definition of defensive stocks, but most investors agree that defensive stocks are those in non-cyclical industries such as consumer staples, healthcare and utilities. Defensive stocks also include those stocks with relatively high dividends, which makes them attractive to income-oriented investors who are likely to hold through a bear market. Defensive stocks are supposed to outperform during market corrections

Defensive stocks are predicted to perform better during the late stages of a bull market when investors rotate out of cyclical sectors and into non-cyclical sectors. The argument is that investors sell one sector with volatile earnings tied to the business cycle, such as energy, and buy another with more stable earnings, such as healthcare. There is another argument that says defensive shares perform better not due to investor buying, but a lack of selling. Investors dump their cyclical shares ahead of and during a correction, but hang on to blue chip dividend paying shares.

While sector rotation occurs, the fatal flaw with defensive stocks is that bear markets are in large part psychological. Looking back at IBM (NYSE:IBM) earnings, one would be unable to pinpoint the 2008 financial crisis since earnings went up in 2008 and 2009, but IBM shares still fell more than 40 percent. Even if a company continues to grow earnings through a recession, the bear market hits valuations as investors demand a greater margin of safety.

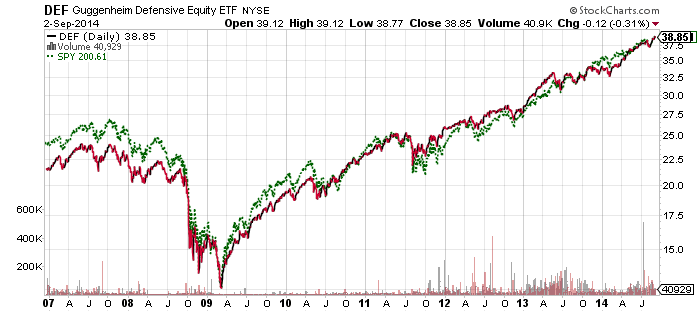

Here's one example of a defensive ETF, Guggenheim Defensive Equity (NYSEARCA:DEF). In green in the chart below is the price of the SPDR S&P 500 Index (NYSEARCA:SPY). Even though DEF has performed well relative to the S&P 500, it hasn't behaved as might be expected by investors looking for a fund that holds up in a down market.

(click to enlarge)

In 2008, DEF declined 30 percent, better than the S&P 500's 37 percent decline. Supposedly, defensive sector funds didn't fare much better. SPDR Healthcare (NYSEARCA:XLV) delivered a relatively impressive 23 percent loss in 2008, well ahead of the S&P 500 Index, but still a major loss.

If the goal is relative performance, DEF and XLV did outperform the S&P 500. However, it makes more sense to include funds such as these as part of a long-term passive portfolio strategy because significant losses will still occur in a bear market. For an investor who is actively rotating into defensive sectors to avoid expected losses, why not pick something that won't lose money?

The Defensive ETFs

In order to qualify as defensive, an ETF or stock should be preferably low risk and lower volatility (which rules out short and leveraged ETFs), and be negatively correlated with the stock market.

U.S. Dollar

Although neither an ETF nor a stock, cash qualifies as a defensive position. Many investors turn to cash during a bear market, selling their riskiest assets in order to cut their losses. In essence, every purchase of an asset is also the selling of cash, or U.S. dollars for U.S. investors, and during a bear market demand for U.S. dollars, or cash, tends to increase dramatically.

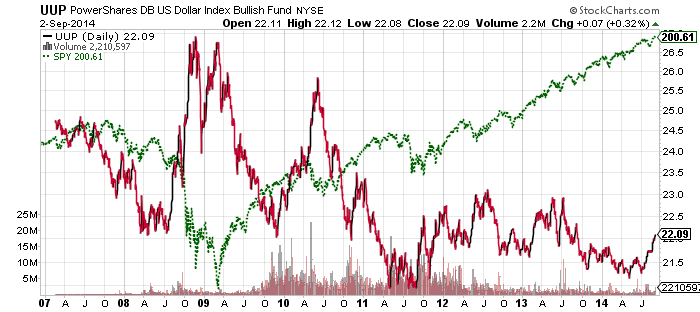

Taking the move to cash one step further, investors can use PowerShares U.S. Dollar Index Bullish Fund (NYSEARCA:UUP) as a defensive position. UUP owns U.S. dollar index futures contracts. The index is about 58 percent in the euro, 14 percent in the Japanese yen and 12 percent in the British pound. For most investors, risk-on leads to buying assets such as bonds, stocks and real estate. Risk-off involves reversing those positions, and that means buying back U.S. dollars. Since the world remains heavily indebted, reducing risk also involves repaying debt, much of which is U.S. dollar denominated, and that leads to a scramble for U.S. dollars during market panics.

Returns haven't been stellar for UUP over the long-term: the fund was up 4.80 percent in 2008, but it has lost ground in every year since then. It is up 2.3 percent so far this year. However, while UUP has consistently lost ground and underperformed the U.S. Dollar Index, in part due to the expenses and the costs associated with rolling futures contracts, its largest annual loss was 6.52 percent in 2009. Furthermore, as the chart below shows, UUP has seen high volatility in its favor when the stock market endures a meaningful sell-off.

(click to enlarge)

What makes UUP attractive as a defensive fund is that investors do not have to be overly concerned with timing. Even if the market doesn't correct and the U.S. dollar weakens, losses are likely to remain limited (assuming it's not the U.S. dollar that is correcting). UUP has a negative 0.72 correlation to the SPY since 2008, but that rises during corrections. Investors won't make a lot of money holding UUP, but a gain of about 10 percent is likely during the correction if there is a major global sell-off in stocks or if a correction is due to problems in Europe, since the euro is such a large component of the dollar index. In a smaller correction or one focused on the U.S. market, UUP may not provide much upside.

Treasury Bonds

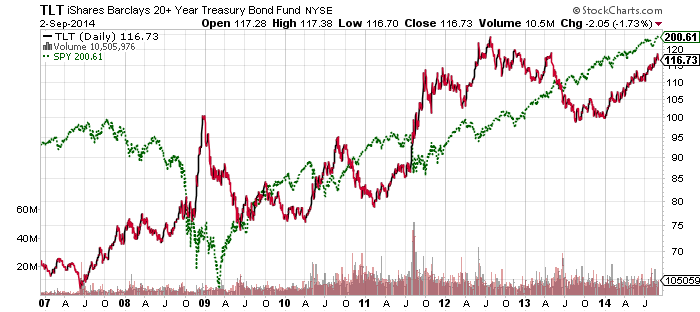

Investors who want to take on more risk, for a chance at more reward, can look to U.S. treasury bonds. Since interest rates typically fall during a market correction and investors move towards the safest of assets, U.S. treasuries tend to catch a strong bid during corrections. The most volatile of these is PIMCO 25+ Year Zero Coupon Treasuries (NYSEARCA:ZROZ), and behind it, iShares Barclays 20+ Year Treasury (NYSEARCA:TLT). In contrast to the low volatility UUP, ZROZ saw a gain of more than 60 percent in 2011 and a loss of more than 20 percent in 2013. ZROZ wasn't around in 2008, but TLT scored a nearly 34 percent return that year, and gained 34 again in 2011. TLT lost nearly 22 percent in 2009 and lost 13 percent last year.

(click to enlarge)

Investors who want less risk can move from long-term treasuries to intermediate-term treasuries. iShares 7-10 Year Treasury (NYSEARCA:IEF) gained more than 15 percent in 2011 and lost about 6 percent in 2013.

Gold

One issue some investors may raise with UUP and funds such as TLT is that the U.S. dollar and treasuries might be the cause of a major bear market. Although TLT has a very high negative correlation to the S&P 500 during market corrections, TLT actually has a positive 0.63 correlation since the start of 2008 due to the Federal Reserve's low interest rate policy benefiting both bonds and stocks. In the event that rising interest rates and a weaker dollar sparks a stock market sell-off, or if a correction is centered on deflationary concerns such as in 2008 or 2011, or sovereign debt concerns as was seen in 2010 and 2011, investors may flock to gold as a safe haven. Gold is not as attractive as a general defensive asset, but investors concerned about these specific risks should consider gold as a defensive holding.

iShares Comex Gold (NYSEARCA:IAU) or SPDR Gold (NYSEARCA:GLD) are two of several options.

Conclusion

Ultimately, turning defensive is mostly about timing, and if you can time the market, you're 90 percent done. The last 10 percent is crucial though: picking the right fund. Many investors who correctly anticipated a crisis in 2008 did poorly because they expected the U.S. dollar to collapse instead of nearly all currencies collapsing against the U.S. dollar.

For the vast majority of investors who are terrible market timers, the best way to turn defensive is to rotate out of riskier, more volatile assets and raise cash. In 2008, cash produced relative outperformance of nearly 40 percent versus the S&P 500 Index. Often times less is more.

It also pays to be prudent. Going completely to cash, for example, is risky if the market goes on to gain 30 percent in the next year. The temptation to get back in at higher prices may cause an investor to miss out on gains and then take losses when the bear market eventually arrives.

Instead of making large moves, take small steps. Move 5 to 10 percent of the portfolio into a more defensive position and then wait to see if you are correct. If the market keeps going up, but you're able to sleep better with 10 percent in a defensive position, there's no need to increase it. The same goes for buying back in. Don't try to time a bottom, but rather slowly move back into a fully invested position as the market drops.

Use stops or actively manage defensive positions. The purpose of a defensive position is to protect capital against losses, not to take losses. Market corrections last weeks, bear markets months. If the asset in question is not behaving as expected and falling along with the market, exit the trade.

For those who are terrible market timers, but insist on trying to time the market, stick with the ETFs that won't blow up your portfolio. Short and leveraged ETFs must be very well timed or they will cause losses that are very difficult or impossible, to overcome.

Remember to sell. A defensive trade is not a long-term investment. Selling a little early or a little late is better than waiting until a gain turns into a loss. The big gains are made during bull markets, not bear markets (unless you're a professional short seller).

No comments:

Post a Comment