There are only two times in your life when you will need money: now and later. Hopefully, you are prepared for both occasions and if not, don't worry - there is plenty to go around! Cash, like all other asset classes, has time-varying preference and utility curves. Cash seems to be in ample supply when it's not needed and scarce when it is in high demand. Does this mean that there is now little demand for cash since cash balances are, by all accounts, at record highs? Or does it mean that there is just not all that much worth buying - so the cash tends to pile up? To turn the page, this analyst believes that today's high cash balances are the result of savvy moves by both companies and individuals that rightly anticipated U.S. dollar appreciation.

Older academics may refer to today's U.S. economy as a having a "Monetary Overhang," or a liquidity surplus. Monetary Overhang is a Soviet era term describing a situation where consumers and State Owned Enterprises (SOEs) accumulated cash in excess of desired amounts simply because there was a lack of ability to spend. In other words, there was little worth buying at advertised prices. How much are we talking about here? I loosely estimate there are about $4.7 trillion dollars of a monetary overhang - cash that is looking for a purpose. Here are my numbers:

(Trillions of USD)

Cash held by U.S. S&P firms [Source] $ 1.80

Cash held in U.S. money market accounts [Source] 2.70

Free cash balances in U.S brokerage accounts [Source] .20

Total $4.70

[I purposely excluded bank deposits - circa $10.2 trillion per Fed Weekly H.8 from the above analysis, since these sums tend to be used to facilitate operational transactions such as paying bills. However, I recognize that this point is highly debatable, and many people use deposits as a savings vehicle.]

Interestingly the savants over at JPM recently estimated excess liquidity at near five trillion U.S. dollars based upon their proprietary regression model. I do not have access to their paper, but you can find a summary here. So the numbers are big and are at extreme levels. There may be a bit of double counting here - U.S. corporations can place funds into money market accounts, but the larger point remains: there is a lot of cash that is looking for a home. A quick diversion is in order here. To be an effective metric of excess savings or liquidity, the measure must provide an a priori equilibrium value. That means you need a benchmark value to compare current readings against a reference value. For corporations, that tends to be about 1% of sales; for Banks it is whatever the Fed says it should be…or enough cash to cover 30 days' worth of contractual and contingent cash flows. For individuals, it is about one years' worth of average earnings.

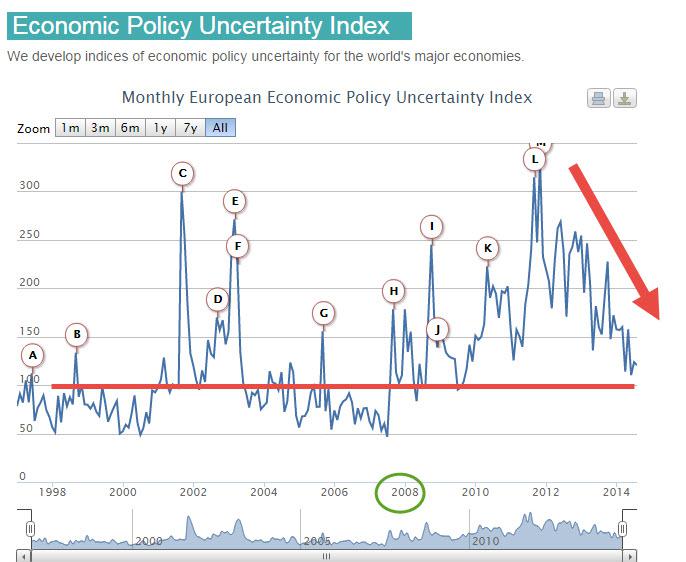

Why are corporations and individuals so willing to hold cash at zero nominal rates and negative real rates? The textbook answer is, of course that there is always a precautionary hoarding of cash in times of high economic uncertainty. However, according to the team of Baker, Davis and Bloom, who attempt to quantify the degree of economic uncertainty, there is a bear market in ambiguity! Specifically, their three-factor model of uncertainty is near an all-time low. That fact may or may not tally with your situation and observations or indeed with reality. Still we are a long way away from the agonizing days of 2008-2009, so it remains puzzling why investors have parked so much cash on the sidelines. Before moving on, we should remember that holding idle cash provides many option like benefits, such as the ability to quickly invest as new opportunities arise, but also comes with a premium, i.e. the lost opportunity cost - which is somewhat counterintuitive, has rarely been lower!

Chart #1 Uncertainty Index(click to enlarge)

Excess cash held by corporations and individuals is expectedly, concentrated in just a few hands. Large mega-cap technology companies like Google, Apple and Microsoft mostly control (own) the large cash balances at S&P 500 companies. Cash placed by individuals in money market funds is also decidedly concentrated. Since the year 2000, cash placed in U.S. money market funds has grown by 47% whilst the number of individual shareholder accounts has fallen by 45%. [Source: ICI Statistics]. It is the same story with excess cash held as free credit balances in brokerage accounts, a luxury that few people can enjoy.

Consequently, excess cash is mostly held by large, sophisticated companies and individuals. These folks have seen the relative value of their cash appreciate by nine percent, despite zero interest rates during the past few years due to U.S. dollar appreciation. These cash-rich companies and individuals can now deploy their appreciated dollars abroad to purchase relatively cheap foreign assets. Assets in the rest of the world have rarely looked so appealing for a U.S. dollar based investor.

What changes or factors will encourage or force companies and individuals to reduce their cash holdings? Here are four that I think are most relevant:

1. Higher than expected inflation and or central banks engineering real rates deeper into negative territory

2. Attractive opportunities to purchase real and financial assets at home or abroad

3.Government confiscation of excess savings by higher tax rates or by implementing a wealth tax

4. Hubris leading to the acquisition of trophy assets at inflated prices i.e. irrational exuberance

Stockpiling of cash for the last three years has proved profitable or at least not a performance drag, despite low nominal rates, for both companies and individuals thanks to USD appreciation. Stick with cash if you think that trend will continue and you are looking to invest in non-dollar assets. If, on the other hand, you cannot take advantage of the strong U.S dollar, a supposedly risk free cash position is, in fact, very risky.

No comments:

Post a Comment