Following the run up to nearly 33 cents, world sugar futures have retreated and stayed in the 22-24 cent range for much of the week. The market is expecting strong production numbers from Brazil and India, the two largest producers, and there seems to be optimism among analysts that the global S-D balance will finally shift to the surplus side in the coming months.

In the USDA Foreign Agriculture Service (FAS) April attache report, their outlook stated that Brazil cane production will increase 2% (to 631 mmt) in the 2011/12 marketing year (MY), with 569 mmt of this volume coming from the Centre-South; the 569 mmt projection is +12mmt over the 2010/11 MY and largely the result of an expansion of hectares for sugarcane, rather than a favorable weather pattern.

See the table below taken from the attache report for harvested hectares over the last 6 seasons. This is confirmed by the relatively flat total reducing sugar (TRS, or industrial yield) when analyzed Y/Y. Readers should note that a drier pattern in key mid/late crop months actually serves to boost yields, and tends not to be an inhibiting factor.

[Click to enlarge]

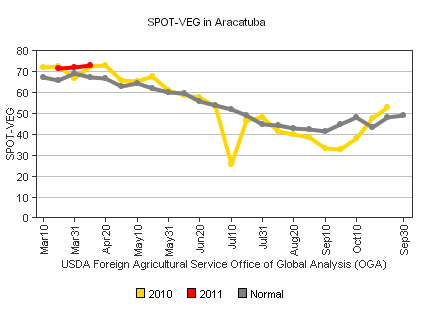

While the Weather Trends view is also for an increase in Y/Y production for BR (between +1.3% and +1.6%), we feel that the USDA estimate may be too optimistic. Further, even with higher production numbers out of Brazil, domestic ethanol demand for flex-fuel cars coupled with high crude prices will still keep a premium built into the #11 price, so the downside price potential remains limited between now and October. Satellite derived vegetation indices for many of the Centre-South cane growing regions are on par with last year which was considered an average weather year for cane in BR.

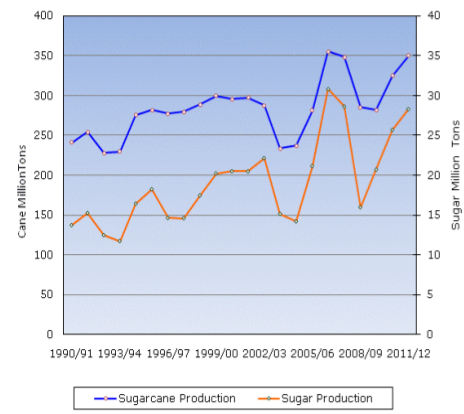

Other FAS estimates carrying significance include their view for Indian sugar production to increase 10% for the 2011/12 marketing year (Oct/Sep) to 28.3 mmt raw value as a function of higher total cane production.

The April FAS attache report fort India includes the illustrative chart below from the India Ministry of Agriculture, which shows total cane production and sugar production since the 1990/91 MY. This shows how in recent years, technological advances as well as the increased demand for raw sugar is allowing growers to extract more sugar per metric ton.

Last year’s gain was also in part due to higher plantings following the Monsoon failure during the previous 2009 season, so the first year in the new retune crop will provide the strongest Y/Y lift; we will still look for a similar increase this year as projected plantings are up again, but as with Brazil, the numbers may be slightly lower than the FAS expectation.

So what does this mean for price? The onset and the seasonal behavior of the 2011 Indian Monsoon will therefore become a key factor in assessing yield potential this year, and this will be a key variable towards ultimately translating what the crop potential means for the global supply balance sheet into 2012. Further, while Brazil is looking at a favorable supply scenario, ethanol demand, crude oil prices and the relative strength of the BR real will be equally important in assessing price risk and potential.

No comments:

Post a Comment