It amazes us that in the 11th year of the gold bull market, there are still so many people around who fail to understand gold on the most basic, fundamental level. One of them is of course none other than the Big Cheese of the Fed himself, Ben Bernanke. However, while everybody should be slightly worried by the Fed chief's admission that he 'doesn't understand gold', and is 'puzzled by its price rally', he is at least admitting it. The irony is of course that he, Bernanke, through his actions, is one of the chief instigators of gold's price strength.

Before we delve into this further, we would like to point out that there has been a proliferation of articles recently that bemoan the allegedly short term bearish technical condition of gold and gold stocks. Here are two well-reasoned examples – the first one is by Chris Vermeulen at Minyanville , the second by long term bull Dudley Baker at Goldseek.

The reason why we want to briefly comment on these articles is that quite a number of slightly worried gold bugs (gold bugs are, by dint of bitter experience, always worried that victory will be snatched away at the last moment) have pointed them out to us.

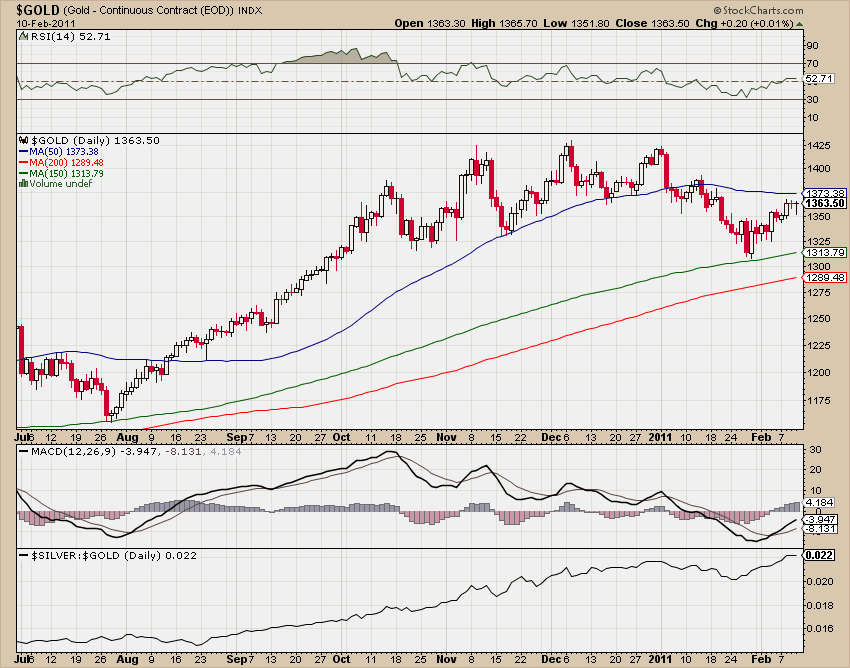

Gold: bounced from the 150 day ma, still below the 50 day. Alas, it is not overbought and MACD is on 'buy' – click for higher resolution.

Looking at gold's chart above, we would note that, yes, it is close to a zone of short term resistance. Alas, there is no evidence yet that the recent decline was anything but a small routine pullback. For gold to indicate that it was more than that, it would have to first break below its recent lows and the 150 day ma it bounced from.

Apart from this technical indecision – neither bulls nor bears can prove much with the help of this chart because neither a breakout to the upside nor one to the downside has occurred as of yet – we would note that gold actually never tends to top out in a 'triple top' type formation.

It normally doesn't happen because this is a very emotional market, in the latter stages of rallies often driven by naked fear. Fear produces spike tops, not lengthy distribution tops. The latter are far more frequent in the stock market (which works exactly the other way around actually, by producing rounded distribution tops and spike lows).

In addition, the mere fact that worried gold bugs are pointing us to these articles is anecdotal evidence of the current widespread uncertainty that is fully confirmed by quantitative sentiment data as well.

Mark Hulbert's HGNSI (a measure of the average recommended gold exposure by gold timers) briefly went negative at the recent lows, the Rydex precious metals fund lost over 40% of its assets due to outflows and open interest in gold futures and the net long speculative position have dropped to two year lows.

While this is obviously not a guarantee for a particular outcome, these facts support the bullish rather than the bearish case. The one thing that looks a bit worrisome for bulls is the fact that many other commodities have recently made blow-off-like moves to the upside and may be ripe for a correction.

Widespread weakness in the commodity sector would likely weigh on gold as well – alas, no such weakness has occurred as of yet.

To come back to what we wrote at the beginning – amazingly, gold remains widely misunderstood by market analysts. Many people will be familiar with Kitco's chief gold analyst Jon Nadler, who continues to analyze gold as though it were the same as copper or aluminum. In his worldview most gold fans are probably slightly loopy, a view that is colored by the fact that the conspiracy fringe in gold bug-land has chosen Nadler as one of its favorite enemies (he's easy to make fun of admittedly). This is due to the fact that he has remained steadfastly bearish throughout the most persistent bull market of the past decade. Why is he bearish? He doesn't understand gold, that's why.

This is yet another great irony of course – the 'chief gold analyst' of one of the biggest precious metals trading firms in the North Americas (Kitco is based in Canada) actually doesn't understand the gold market. It would be difficult to make this one up.

Meanwhile, a very recent example of someone suffering from a similar affliction has been provided by David Berman in the 'Globe and Mail' under the title 'The Case Against Gold'. Even if there were a 'case against gold' (right now there really isn't), this could not possibly be it.

Berman makes -similar to Nadler – the often seen mistake of thinking of gold as though it were an industrial commodity. He regales his readers with statistics of annual jewelry demand, mine supply and central bank selling. He somehow forgets to mention that the all time record high in jewelry demand was recorded in 1999 – at the very low point of a 20 year long bear market in gold. We don't recall seeing any articles at that time arguing that 'record jewelry demand means that gold prices must go up'. As it were, jewelry demand is completely immaterial to gold's price – as are all the other 'fundamental factors' (mine and scrap supply, central bank selling) Berman cites – including the alleged 'impact of exchange traded funds'.

Just about the only thing that contains a grain of truth is Berman's statement that

The bullish argument for gold rests primarily upon fear – the fear that paper currencies are being devalued by governments and central banks; the fear that the world is awash in money, which will lead to problematic inflation; and the more general fear that the world is falling apart, and prudent doomsayers will need more than shotguns and tins of beans to survive. |

Yes, fear of the devaluation of paper currencies plays a big role in gold's rally. Not only the 'fear' of same of course, but the quite obvious fact of same. As we recently related, US true money supply TMS-2 is close to tripling from its level a decade ago. So we are well beyond the stage of 'fear of devaluation' by now into the realm of actual, massive devaluation. It is true that therefore, 'investor confidence in paper currency has been rattled'. It's the 'creative monetary policies' (why printing gobs of money is considered 'creative' is not quite clear to us, unless it was meant to be sarcastic) that have done it. Note here that the influence of 'terrorist attacks' on gold can be safely ignored, as it rarely lasts beyond a few hours of trading (as an example, the WTC attack occasioned a $20 one day spike in gold that was given back in its entirety over the following two weeks).

It is a pity that Berman didn't think this particular argument about currency devaluation through further – instead he segues from there into discussing gold ETFs, which he deems to be the chief culprits of gold's rally. Gold ETFs have made investing in gold easier for institutions and retail investors alike, and as such have certainly paved the way for a little more gold investment at the margin than would have otherwise occurred. However, the assumption that they are an indispensable major factor in determining gold's price is just as flawed as the assertion that jewelry demand has an important impact. In reality, all these things are but a drop in the ocean.

As we have pointed out previously, the chief mistake Berman, Nadler et al. make is to regard gold as a commodity akin to an industrial commodity like e.g. copper, the stocks of which are regularly used up. For more background on this, look at 'Some Thoughts on Gold' Part One and Part Two . In part two, we criticized a similarly flawed analysis of gold that was published in the WSJ last year.

The total stock of gold in the world is about 165,000 tons. All of it still exists. Annual mine supply of 2,500 tons, jewelry demand of 1,700 tons and the largest gold ETF's holdings of 1,250 tons are insignificant compared to this accumulated stock. At the LBMA (London Bullion Market Association), the annual mine production of gold is turned over in trading every three to four business days. All the jewelry makers in the world could basically buy their entire fabrication stock in less than three trading days there – and that is only the LBMA. There is quite a bit of gold trading going on in other ventures such as Dubai, Zürich, New York and Shanghai as well.

Gold is not analyzable as a commodity that gets 'used up' in industrial processes. Its large stock-to-flows ratio indicates that it must be analyzed as what it really is, a currency, or a financial asset. It is the reservation demand of the current holders of this large stock of gold that is the most important factor in its valuation. It should be quite obvious in this context that reservation demand encompassing 165,000 tons of gold will not be influenced much by a central bank selling 100 tons here or an ETF gobbling up 50 tons there.

In short, it is monetary or investment demand, which in turn is technically divisible into outright new demand and reservation demand, that is the main driver of gold's price. If one wants to analyze gold's likely price trend, it would be perfectly legitimate to completely ignore annual mine and scrap supply and annual industrial and jewelry demand for gold. One might perhaps mention these as 'marginal factors', but they really are unimportant in terms of the bigger picture. Instead, one must concentrate on the factors driving above mentioned monetary demand.

These factors are, in no particular order:

- the level of real interest rates (i.e., nominal interest rates minus market-based inflation expectations),

- the dollar's exchange rate,

- the rate of growth of the true money supply,

- the steepness of the yield curve,

- credit spreads (and other indicators of waxing or waning economic confidence),

- the desire to increase or decrease savings, and

- confidence in government, the monetary authority and the financial establishment generally.

One thing we can take away from Berman's article is that there are still quite a few people out there that need to be apprised of the gold market's workings. This in turn means that there remains a large source of potential gold demand that is as of yet untapped. People who don't understand gold are likely to be wary of buying it upon hearing that 'jewelry demand has fallen precipitously'. After all, on the surface it sounds like just the thing that might be bearish. In reality, jewelry demand is but a tiny component of overall gold demand and its most price elastic one to boot. Note here that a certain percentage of jewelry demand is actually part of the investment demand for gold. This is especially true in India, where 'bullion jewelry' is sold at a very small mark-up to the spot price of gold and used not mainly for adornment, but as a form of savings.

In any case, it seems important to us that the flaws in Berman's analysis and similar attempts to disparage gold investment on the basis of irrelevant data be pointed out. We would add to this that the situation has actually improved somewhat in recent years in terms of mainstream analysis provided by banks and investment banks, which is certainly a gratifying development.

Lastly, we want to point readers to an article that has recently appeared at Zerohedge – the Dutch Central Bank is unhappy with a pension fund allocating too much money to investment in gold and is ordering it to divest. It is interesting in this context that government debt securities are apparently exempted from the 'prudent man' rule that is supposed to stand in the way of this 'concentration risk'.

Ironically, yields on Portuguese government bonds hit a fresh all time high just as this order was handed down – so government debt is deemed a 'prudent investment' even if it goes to hell in a hand basket, but gold is 'too risky'. The Dutch Central Bank makes the same analytical mistake as Berman - it keeps referring to gold as a mere 'commodity'. The pension fund on the other hand points out in its deposition that gold is actually – gasp! – money.

No comments:

Post a Comment