by Charles Hugh Smith

Complacent melt-ups aren't just boring--they're not very profitable.

File this under Devil's Advocate: what if the easy money in the stock market is no longer the "guaranteed" Bull melt-up but the Bearish bet on a sudden air pocket?Just as a thought experiment, put yourself in the shoes of the money managers who have the leverage to move the markets.

You probably know the drill: program your trading bots to recognize every technical trading scheme's key support and resistance levels, and then unleash huge futures/options buys after hours or pre-open so the market jumps in the direction that makes you the most money.

Unleashing a tsunami of buy orders forces Bears to cover their bets on a decline (shorts), goosing the market higher. The melt-up depends not just on trading bots hammering the market in the desired direction with massive buy orders--it depends on a supply of nervous Bears to cover their shorts by buying stocks. This buying triggers others' trading bots to buy into the rally.

Short-covering is an essential source of the self-reinforcing buying that has kept the U.S. market melting up for years without any gyrations down of more than a few percentage points.

Buy the dips has entered the Pavlovian realm of automatic response because the managed tsunamis of futures/options force those betting on a decline to cover their shorts by buying, pumping the rally up with steroid-like buying.

The problem with this guaranteed melt-up is the unceasing advance and immediate buy the dip response has decimated the ranks of Bears willing to bet against the melt-up. This has removed one of the primary fuel sources of the melt-up.

In other words, the managers' great success with forcing Bears to seek cover has drained a key reservoir of buying power. Eradicating the Bears has all been jolly good sport, but it has also reduced the shorts who can be forced to cover, which means the market is left with only the managers' manipulations and the other institutional trading bots that follow trends.

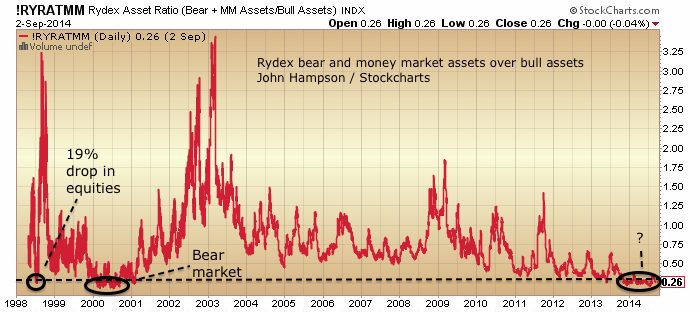

Consider this chart of the Rydex ratio of Bear/Bull assets, from John Hampson:

If Market Bears were tallied, they'd be on the list of Endangered Species. There is some confusion about the true number of Bears left, as prudent money managers may buy puts (bets on a market decline) to hedge their portfolios. As a result, a mass of put buying may reflect hedging, not Bearish bets.

The net result of eradicating the Bears is the gains from the melt-up are now limited. If you're a serious manager of serious money, squeezing out a couple of points from the melt-up is not only boring--it's detrimental to your career, because you need to beat the index melt-up to keep your big-bucks job and skim your payoff.

Which leads to the notion that the really big money waiting to be skimmed from the unwary is not more melt-up but a sudden "unexpected" meltdown that catches everyone who isn't short off-guard. The most profitable trade would be to stealthily build a short position while telling everyone else how the melt-up was guaranteed essentially forever ("the Fed, ECB and Bank of Japan have your back," etc.).

To make sure nobody strayed from the long side of the boat, you'd unleash the usual frenzy of buy orders at every dip, because the last thing you'd want is to give anyone else an easy entry to the Bearish short side.

The ideal situation is a boat heavily tilted to one side with complacent Bulls confident in the continuation of the never-ending melt-up, and only yourself and a few insider cronies on the short side.

Then, when all the Bulls are happily swapping stories about how the yen carry trade guarantees capital flows into U.S. equities and other Bull stories--

BANG! You unleash a tsunami of sell orders that triggers all the trend-following trading bots to sell. When the buy the dip crowd confidently enters their buy orders, you crush them with a load of futures and options orders that reverse the uptick. This triggers another wave of bot selling.

Since there are no Bears left except you and your cronies, the buy the dip retraces have no legs: they quickly peter out because no Bears are left to spark short-covering buying.

Since there are no Bears left, there's only the trading bots programmed to follow trends: and with your leverage and bag of tricks, that trend can go down faster than complacent Bulls thought possible.

Then, when the Bulls are stampeding in panic selling, you cover your Bear bets and start buying from the panic-stricken Bulls. The Hobby Bears who went short near the bottom are forced to cover as your buying turns the tide, and the market is soon in full recovery mode.

This is such an obvious (and immensely profitable) play, I'm surprised we haven't seen it more often. Complacent melt-ups aren't just boring--they're not very profitable.

No comments:

Post a Comment