Equity investors are struggling to figure out how to approach the European enigma. It’s clear that a recovery is brewing, but there’s still too much uncertainty for comfort. In our view, distinguishing the European context from that of the US or Japan can help point the way toward unravelling the puzzle.

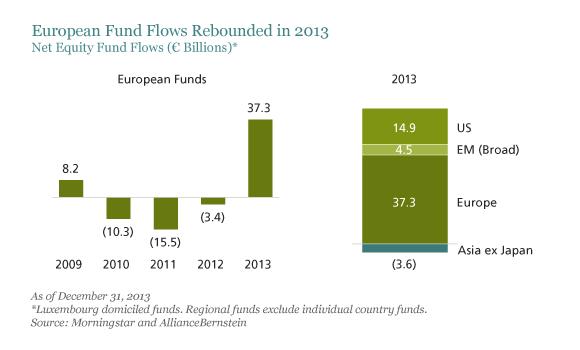

Investors have been rediscovering Europe. During 2013, flows to non-US regional equity funds investing in Europe turned positive for the first time since 2009, jumping to €37 billion (Display). It’s been a long time since we’ve seen such a clear preference for European equities over other regions.

But earnings don’t seem yet to support the renewed optimism. Profit margins of European companies are still compressed. Earnings growth remains sluggish across the continent. And earnings revisions for European companies have been below those elsewhere in the world so far this year.

Is the Recovery Real?

So why are investors upbeat? Signs of a nascent recovery of economic growth are clearly part of the story, as some of the hardest-hit countries in the periphery—including Spain, Portugal and Ireland—exited recession last year. Our economists forecast euro-area growth of 1.1% in 2014.

It’s also possible that investors hope the European Central Bank (ECB) will ultimately follow the examples of the US and Japan, where extraordinary monetary policies have helped kick-start the private sector. In other words, perhaps the ECB will eventually be forced to resort to the same type of quantitative easing tactics that have fueled economic growth elsewhere in the largest developed economies.

In fact, to date, the ECB has conspicuously avoided following the lead of the Fed and Bank of Japan in expanding the monetary base—despite ECB president Mario Draghi’s famous pledge to do “whatever it takes” to protect the euro (Display, left chart). As a result, inflation in the euro area has continued to decline, in contrast to Japan (Display, right chart), where the Abenomics plan has helped prompt a reversal of persistent deflation. And as long as fiscal austerity remains the norm and quantitative easing isn’t on the policy agenda, the threat of deflation will linger. None of this sounds very good for European stocks.

Finding Winners in a Complex Landscape

That view, however, depends on how you look at it. In fact, we think the current environment creates an excellent backdrop for discerning, stock-picking approaches. Relatively low levels of earnings and profit margins mean that there is ample room for European companies to improve profitability and deliver growth. But since regional conditions are so shaky, it’s vital to identify those companies with a strategic advantage, global revenue base and superior management that are capable of delivering results. This is not a case of all boats rising at the same time.

Caution is warranted. At the stock level, many European companies are vulnerable and could underperform without a supportive monetary and fiscal environment. And at the portfolio level, passive, diversified approaches offer little protection from potential bouts of weakness. Investors in European index funds may find themselves saddled with exposure to many companies that are less capable of weathering volatility and more susceptible to a potential downturn of the market.

We think global portfolios shouldn’t ignore Europe, where the recovery isn’t fully baked into stock prices, as in some other parts of the world. By using deep research to search across diverse sectors, stock pickers can find companies with better prospects for margin improvement that can do well in challenging conditions—and would be rewarded even more in a surprise acceleration of a European recovery.

No comments:

Post a Comment