By: Tony_Caldaro

After making a new all time high last Friday the market traded lower all week. Then Friday’s Payrolls report was released and the market nearly managed to get back the entire loss in just one day. For the week the SPX/DOW were -0.2%, the NDX/NAZ were +0.3%, and the DJ World index lost 0.9%. Economic reports for the week were overwhelmingly positive. On the uptick: ISM manufacturing, construction spending, auto sales, the ADP, new home sales, Q3 GDP, monthly Payrolls, personal spending, the PCE, consumer sentiment, consumer credit, the M1-multiplier, the monetary base, the WLEI; plus weekly jobless claims, the unemployment rate and the trade deficit all improved. On the downtick: ISM services, factory orders, personal income and investor sentiment. Next week we get a look at retail sales, inventories and the PPI. Best to your week.

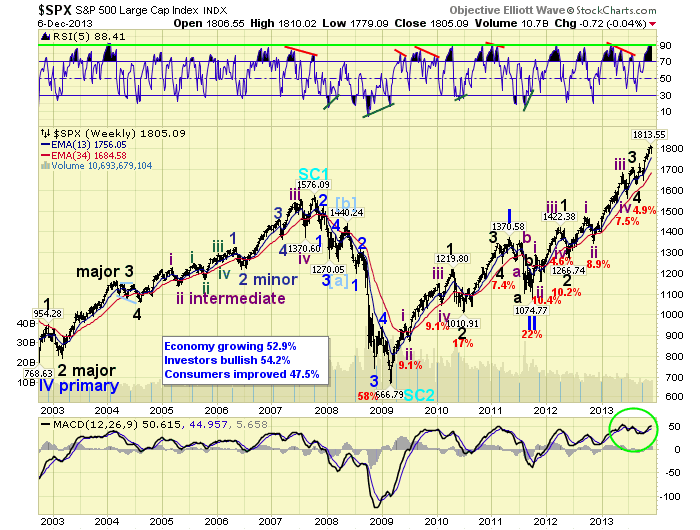

LONG TERM: bull market

Relentless isn’t it. The Cycle wave [1] bull market, now in its 56th month, has exceeded our bull market high projection by about 3%. We have been expecting this bull market to unfold in five Primary waves, and it is still in Primary wave III. Primary waves I and II ended in 2011. Primary III has been underway since then. Primary I took 26 months to unfold, and Primary III is now in its 26th month. Primary I rose a bit more than 700 SPX points, and Primary III is currently a bit more than 700 SPX points as well. How is that for symmetry.

There are differences however. Primary I had only one subdividing Major wave, while Primary III already has had two. The fifth wave of Primary I was quite short at 120+ SPX points. Primary III’s fifth wave is already nearly 200 SPX points. On the surface it would appear Primary III has the potential to extend in time and price.

MEDIUM TERM: uptrend

Last Friday the market hit an all time high early, and then had its first significant pullback since that rally from SPX 1777 began. There was also an abundance of negative divergences, from short term to medium and long term. This week the market did sell off, declining to SPX 1779 by midday Wednesday. This resolved most of the short term negatives.

We have been counting the current uptrend since the late August low at SPX 1627. The market first rose in five waves to SPX 1730, then pulled back to 1646. It rose in another five waves to SPX 1775, then pulled back to 1746. And finally another five wave rally to SPX 1814, then a pullback to 1779 this week. We mention this pattern because there has not been one overlap of any of the waves yet. In example: SPX 1746 bottomed above 1730, and SPX 1779 just bottomed above 1775. You can see this on the daily chart above, but it is clearer on the hourly chart below. What this means is that until there is an overlap we can not be certain that an uptrend has ended. Until SPX 1775 is overlapped this uptrend can extend yet again. Medium term support remains at the 1779 and 1699 pivots, with resistance at the 1828 and 1841 pivots.

SHORT TERM

Currently we have a tentative green v/i label at the SPX 1814 high. The ‘v’ suggests a potential Intermediate wave v high, ending Major wave 5 and Primary III. The ‘i’ suggests an Intermediate wave i high, with Intermediate waves ii-iii-iv and v to follow before ending Major 5. Until SPX 1775 is overlapped there is the potential for other counts as well. The overall bias appears to be bullish until SPX 1775 is overlapped.

Short term support is at the 1779 pivot and SPX 1746, with resistance at SPX 1810, SPX 1818 and the 1828 pivot. Short term momentum ended the week overbought. The short term OEW charts are positive with the reversal level SPX 1797. Best to your trading!

FOREIGN MARKETS

The Asian markets were mostly lower on the week for a net loss of 1.3%. Fifty percent are in confirmed downtrends.

The European markets were all lower on the week for a net loss of 3.1%. Seventy-five percent are in confirmed downtrends.

The Commodity equity group were all lower on the week for a net loss of 1.5%. All three indices are in confirmed downtrends.

The DJ World index is still uptrending but lost 0.9% on the week. Currently 65% of the world’s indices are in confirmed downtrends.

COMMODITIES

Bonds continue to downtrend losing 0.8% on the week.

Crude is uptrending again and gained 5.4% on the week.

Gold remains in a downtrend losing 1.7% on the week.

The USD is downtrending again losing 0.5% on the week.

NEXT WEEK

Tuesday: Wholesale inventories. Wednesday: Treasury budget. Thursday: weekly Jobless claims, Retail sales, Export/Import prices and Business inventories. Friday: the PPI. The FED has nothing scheduled until the FOMC meeting on the 17th and 18th. Best to your week and Holiday season.

No comments:

Post a Comment