by Charles Hugh-Smith

About the claim that central banks will never let asset bubbles pop ever again--their track record of permanently inflating asset bubbles leaves much to be desired.

The problem with trying to solve all our structural problems by injecting "free money" liquidity into financial Elites is that all the money sloshing around seeks a high-yield home, and in doing so it inflates bubbles that inevitably pop with devastating consequences.

As noted yesterday, the Grand Narrative of the U.S. economy is a global empire that has substituted financialization for sustainable economic expansion. In shorthand, those people with access to near-zero-cost central bank-issued credit can take advantage of the many asset bubbles financialization inflates.

Those people who do not have capital or access to credit become poorer. That is the harsh reality of neofeudal, neocolonial financialization. Neofeudalism and the Neocolonial-Financialization Model (May 24, 2012).

Injecting liquidity by creating credit and central bank cash out of thin air is not a helicopter drop of money into the economy--it is a flood of money delivered to the banks and financial elites. The elites at the top of the neofeudal financialization machine already have immense wealth, and so they have no purpose for all the credit gifted to them by the central banks except to speculate with it, chasing yields, carry trades and nascent bubbles (get in early and dump near the top).

Life is good for the kleptocratic financial Aristocracy: for debt-serfs, not so good.

No wonder the art market and super-luxury auto sales have both exploded higher. Thanks to the central banks' liquidity largesse, the supremely wealthy literally have so much money and credit they don't know what to do with it all.

If you want to borrow money to attend college, the government-controlled interest rate is 9%. If you want to speculate in the yen carry trade or buy 10,000 houses, the rate is near-zero or at worst, the rate of inflation (around 2% to 3%). If you want to borrow money for anything other than a socialized mortgage to buy a single-family home, tough luck, you don't qualify. But if you want to speculate with $10 billion--here's the cash, please please please take it off our soft central-banker hands.

If your speculations end badly, then no problem, we transfer the toxic trash heap of debt and phantom assets onto the balance sheet of the central bank or onto the public (government) ledger.

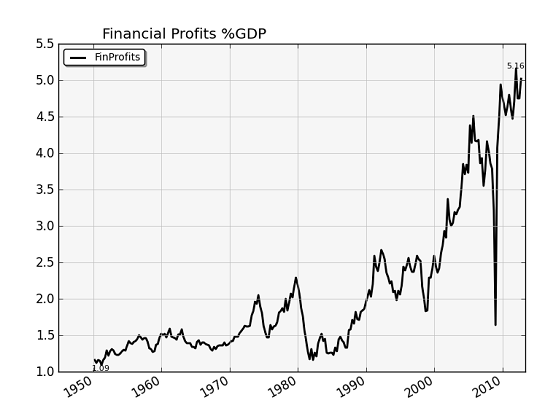

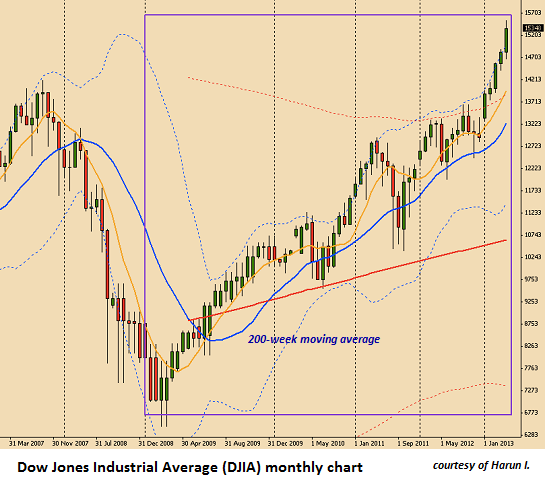

Given this reality, it was inevitable that the stock, bond and housing markets would all be inflated into bubbles by this monumental flood of free money. Please consider these three charts:

Spot The Bubble: Average New Home Price Soars By Most Ever In One Month To All Time High (Zero Hedge)

Verdict: bubble.

Verdict: bubble.

Japanese Bond Market Halted At Open As Bond Selling Purge Goes Global (Zero Hedge)

Verdict: bubble popping.

It is widely accepted as self-evident that all these bubbles will not pop because the central banks won't let them pop. That's nice, but if this were the case, then why did stocks crater in 2000-2001 and 2008-2009, and why did the housing bubble implode in 2008-2011? Did they change their minds for some reason?

No; they assured us right up to the moment of implosion that everything was fine, there was no bubble, etc. The only logical conclusion is that bubbles pop even though central banks resist the popping with all their might.

In the past, central banks were pleased to inflate one bubble at a time, enabling money both smart and dumb to flee one smoking ruin and get busy inflating the next bubble-ready asset class.

But now, thanks to essentially unlimited liquidity and credit, the central banks have inflated three bubbles at the same time: stocks, bonds and housing. That raises an interesting question: what if all these bubbles pop in unison? Will the central banks be able to place a bid under all three markets simultaneously? If so, where will all that freed-up cash go next?

One possibility is gold, another is commodities such as grain and oil. The latter is especially interesting, because central banks and governments hate energy speculators with special intensity because the "Brent vigilantes" have the power to boost inflation where it matters, i.e. energy.

Once energy takes off in a speculative bubble, the rising cost of energy sucker-punches the already-anemic global recovery, and the responsibility eventually lands on the laps of the central banks who created all the bubbles. Their quantitative easing policies discredited, the central banks will have to restrain their liquidity hand-outs, and that will undermine what's left of the various speculative bubbles they've blown.

Those who argue bubbles won't be allowed to pop ever again should look at history from 1999 to the present again.

No comments:

Post a Comment