by

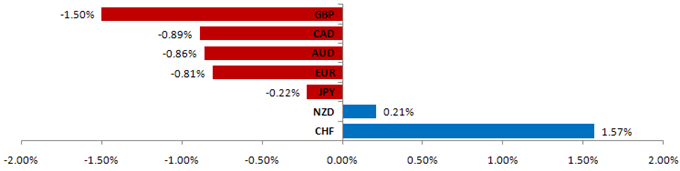

Major Currencies vs. US Dollar (% change)

20 Jun 2011 – 24 Jun 2011

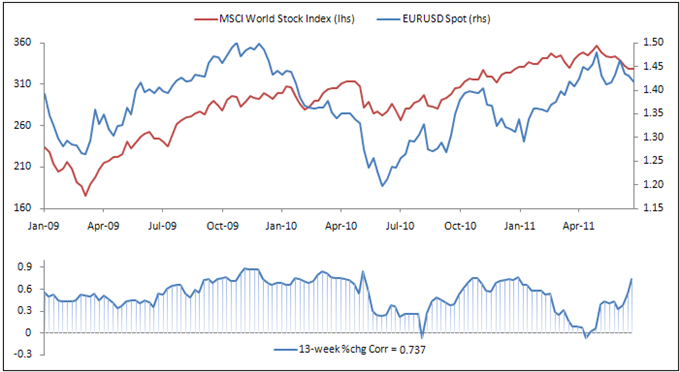

EUR/USD: Euro to Rise as Greece Passes Austerity Plan

The centrality of the Greek debt fiasco to market sentiment at large has forged an intimate correlation between the Euro and global stock prices. This week, this means the focus for both is the Greek parliament’s vote on a new set of austerity measures – a package including tax hikes, spending cuts, and government asset sales – tied to receiving a new round of EU/IMF funding designed to stave off default.

The vote is appears largely ceremonial: last week, Greek Prime Minister George Papandreou called and survived a confidence vote that was designed to give him the mandate to push through just such a package, so to think the same policymakers that were on board with the agenda then would undermine it now seems very unlikely.

While markets will surely remain jittery until the final outcome has been secured, the vote’s completion promises to boost confidence as markets breathe a sigh of relief having avoided the destabilizing effects of a sovereign default (for now). This points the way higher for the single currency over the near term, at least until expectations of slowing economic growth in all three leading engines of global output (China, US, Europe) through the second quarter re-emerge after the Greek crisis fades from the spotlight.

An early estimate of June’s region-wide Consumer Price Index reading and the US ISM gauge of manufacturing activity headline the economic data calendar for the remainder of the week.

Source: Bloomberg

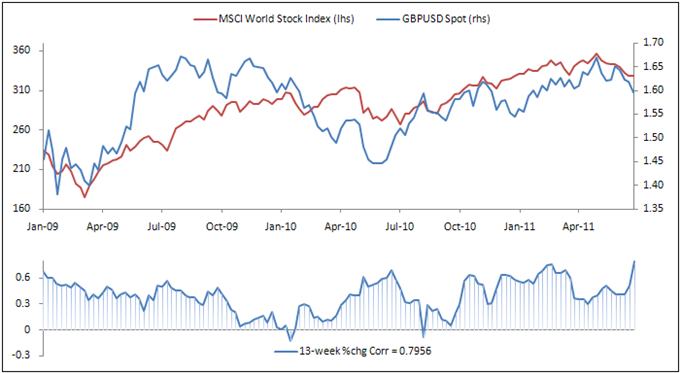

GBP/USD: Pound to Gain with Recovery in Risk Appetite

The absence of any significant developments on the monetary policy front has brought risk appetite trends back into focus for the British Pound. Over the near term, this has aligned Sterling with the Euro while the Greek debt crisis dominates sentiment, hinting it too will rise as the safe-haven US Dollar comes under pressure after the likely passage of a new austerity plan that opens the door for a fresh round of funding for the beleaguered Mediterranean nation.

The UK unit’s advance may be somewhat limited compared with the single currency however considering it had been a beneficiary of stress in the currency bloc as a regional alternative to the Euro, and a positive outcome from Athens will invariably reverse some of those flows. June’s Manufacturing PMI reading headlines the economic calendar, with expectation calling for the sector’s growth to narrowly pick up for the first time in five months.

Source: Bloomberg

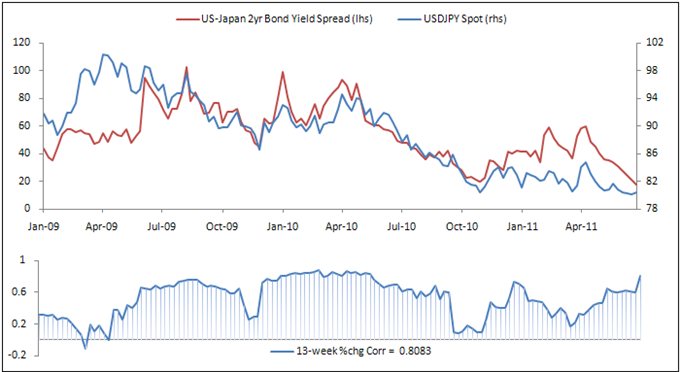

USD/JPY: Prices Look to Greek Vote, ISM for Direction

The spread between US and Japanese 2-year Treasury bond yields remains the core driver of USDJPY. IN the absence of major economic data for much of the week, Euro Zone debt concerns will indirectly play a role here as well. A successful vote in Greece is likely to send capital out of the safety of US Treasuries, putting bond prices under pressure and sending yields higher by default. The imminent completion of the Fed’s QE2 program will encourage this dynamic, making this pair one of the few where the greenback is likely to advance as Athens pushes their problems further down the road.

The US ISM Manufacturing reading to be released on Friday may cut the move short, however. Expectations call for the weakest reading in 22 months, which threatens to reignite fears of a broad-based global slowdown in the second half of the year, undermining sentiment and pressuring USDJPY lower anew. A large batch of Japanese economic releases including Unemployment and CPI figures as well as the Tankan manufacturing survey are also on tap.

Source: Bloomberg

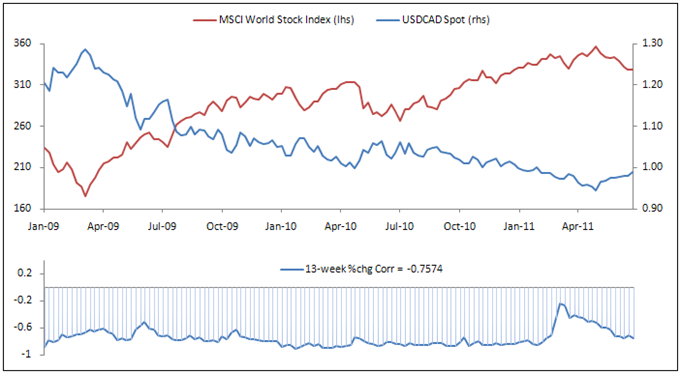

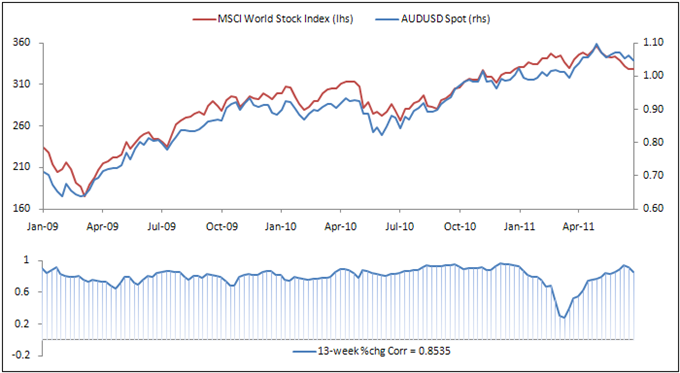

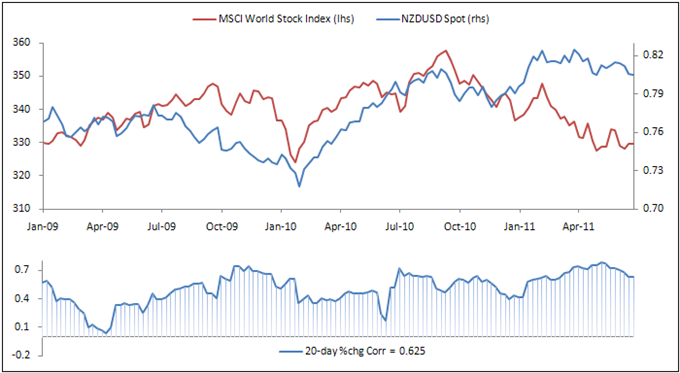

USD/CAD, AUD/USD, NZD/USD: Stocks Still Leading the Comm Bloc

The so-called “commodity bloc” currencies remain firmly anchored to stock markets, the reflection of a sensitivity to the trajectory of global economic growth underpinning the trends driving both sets of assets. As elsewhere this week, this puts the spotlight on the Greek austerity vote for the majority of the week – an arrangement that suggests the path of least resistance is to the upside – but leaves the door open for a reversal as US ISM figures cross the wires. Australian Private-Sector Credit, New Zealand Business Confidence as well as Canadian CPI and GDP figures headline the homegrown data docket.

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

No comments:

Post a Comment