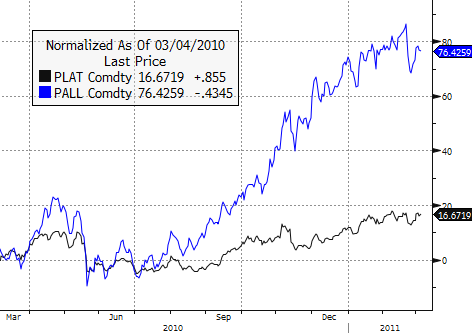

In just over one year, the ETF Securities Platinum Trust (PPLT) and Palladium Trust (PALL) have swelled to $832.65 million and $932.66 million in assets under management, respectively. Is acceleration just a spillover effect from gold's stratospheric rise? Or is something else fundamentally driving these metals higher?

Factors Driving Today's Prices

On Friday, platinum closed at $1,841/oz, up 4 percent since the beginning of the year. Meanwhile, palladium, 2010's big winner, is up only 1.28 percent year-to-date, closing at $810/oz. While these year-to-date returns may seem lackluster, there are reasons to believe higher prices may be soon on the way:

Both metals have seen prices like these before. Back in 2008, platinum rose to almost $2,200/oz right before the crash. For palladium, you have to look back a bit further; in 2001, the metal briefly scaled the $1,000/oz mark, before quickly falling back under $400/oz.

But the impetus for today's price increases can be traced back to the after-effects of the 2008 crash. Demand for both metals dropped after the crash, and mining companies rushed to contract supply.

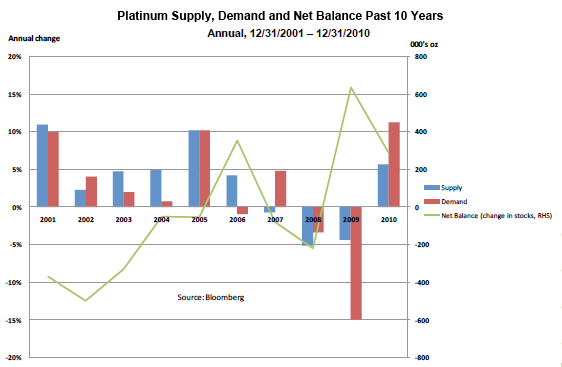

In platinum, 2009 demand contracted sharply, much more quickly than supply — which led to a market oversupply in 2010. Still, demand rebounded in 2010, which absorbed much of that oversupply, thus tempering any further price increase for the metal:

[Click all to enlarge]

Source: ETF Securities Platinum and Palladium - 2011 Outlook and Fundamentals

Without that oversupply created in 2009, platinum prices would have risen much higher last year — a scenario that played out in palladium:

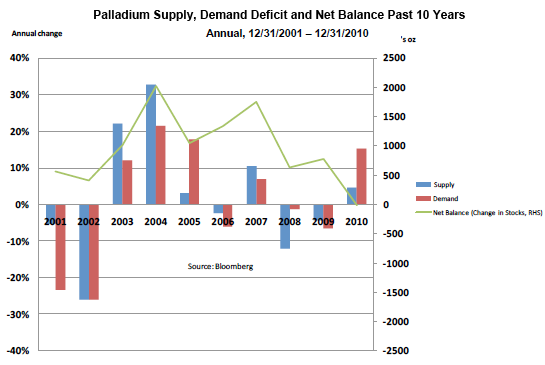

Source: ETF Securities Platinum and Palladium - 2011 Outlook and Fundamentals

Palladium supply contracted by over 10 percent in 2008, and dropped another 4 to 5 percent in 2009. Demand also contracted, but not as sharply as supply. Thus, when demand for palladium rebounded sharply in 2010, it quickly outpaced supply, and prices rose accordingly.

Supply Constraints

Supply of both metals comes primarily from mining output in South Africa and Russia, with South Africa producing roughly 76 percent of all platinum and 35 percent of all palladium. Russia, meanwhile, supplies only 13 percent of platinum, but is the world's major palladium producer, supplying 52 percent of the metal. Mining supply of both of these metals has been constrained for a variety of reasons.

In South Africa, one of the main problems has been power — or the lack thereof. There just hasn't been enough steady electricity to meet mining industry needs. A new power policy is expected to be in place in South Africa by April, but it will still be a number of years before new capacity comes online. Eskom executive Kannan Lakmeeharan said that the supply-demand margin for power in South Africa will remain slim for the next five to six years, with the next two years being particularly tight. Not good news for mining production in the short run.

For Russia, figuring out the supply picture is trickier, because much of the palladium coming out of the country has originated from national stockpiles — and stockpile levels are considered a state secret. However, to get some indication of Russian inventories, the industry instead watches what gets sold in Switzerland — it being one of two major cargo hubs for the metal — and signs there suggest Russian stockpiles might be getting low. Last year, shipments from Russia to Switzerland dropped 12 percent, falling to 500,000 ounces, according to customs data reported by Bloomberg.

With palladium stockpiles most likely decreasing in Russia, and mine production forecast to decrease over 5 percent in 2011, palladium's supply picture thus remains tight.

David Davis, a mining investment analyst at Standard Bank's SBG Securities (Pty) Ltd, was quoted in Bloomberg as saying, "The palladium market, excluding any Russian stockpiles coming in, is going into an ever-increasing deficit. It'll put upward pressure on the price."

But just how high can the metal go? That depends on tomorrow's demand.

PGM Demand Depends On Jewelry, Cars

While platinum remains heavily used for jewelry, demand from that sector dropped from 40 percent to 32 percent in 2010, due to higher platinum prices. Investment demand accounted for another 7 percent, with the remainder allocated to the autocatalyst sector and for other industrial uses. (Although both platinum and palladium are commonly used in fume-scrubbing catalytic converters for cars, platinum remains the preferred choice for diesel engines. Palladium is preferred for gasoline engines.)

Palladium demand remains more concentrated in the autocatalyst sector and industrial use sectors, with only 7 percent used by jewelers in 2010 (although that is up from 3 percent in 2001). Another 7 percent was attributed to investment demand (up from 1 percent in 2006).

In 2010, palladium demand hit its highest levels in 10 years, boosted by increased environmental standards around the world and China's strong vehicle sales — over 17 million cars sold in 2010. Chinese vehicles are primarily gasoline-powered cars, as opposed to diesel; thus they require more palladium than platinum.

Global auto sales are forecasted to only increase; J.D. Power and Associates expects global light vehicle sales to rise 6 percent in 2011, with Asia leading the increase in automobile demand. Analysts predict China will sell 11 percent more cars in 2011. While that prediction is much lower than the growth rates seen in the past (33 percent in 2009 and 48 percent in 2008), it's still quite healthy and will ensure steady demand for both platinum and palladium.

But with tight supply and rising demand, price increases in platinum and palladium may begin to change the way the metals are used. Should prices rise too far, automobile manufacturers will be motivated to look for technological advances to decrease — or even eliminate — platinum and palladium usage.

In fact, that may already be occurring. As Bloomberg recently quoted Wulf-Peter Schmidt, manager for sustainability, Ford Motor Co. (F): "The amount of precious metals in catalytic converters is reduced. It's already being done."

In all likelihood, this tight supply/demand situation defines a new normal for the platinum group metals. The futures markets seem to agree; on Friday, Nymex raised the margin for palladium futures. While that doesn't really have an impact on anyone except individual futures traders, it does signal that perhaps NYMEX sees current palladium prices as a new baseline; after all, they wouldn't bother increasing the margins (which are a fixed dollar amount per contract) if they thought these prices were simply part of a bubble.

No comments:

Post a Comment