by Gail Tverberg

Oil and other commodity prices have recently been dropping. Is this good news, or bad?

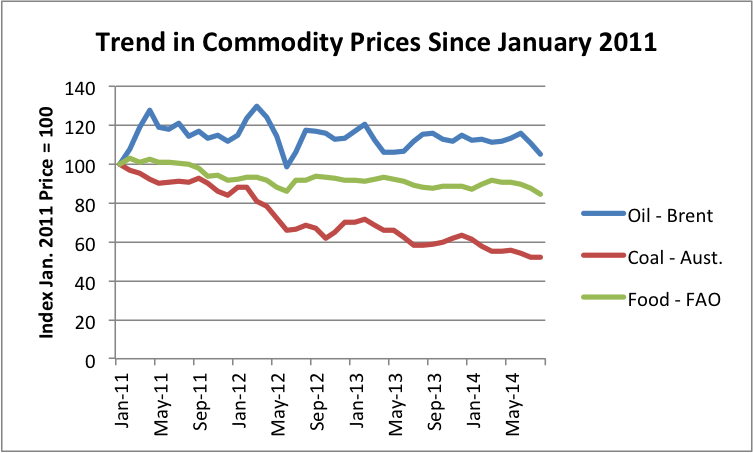

Figure 1. Trend in Commodity Prices since January 2011. Brent spot oil price from EIA; Australian Coal from World Bank Prink Sheet; Food from UN’s FAO.

I would argue that falling commodity prices are bad news. It likely means that the debt bubble which has been holding up the world economy for a very long–since World War II, at least–is failing to expand sufficiently. If the debt bubble collapses, we will be in huge difficulty.

Many people have the impression that falling oil prices mean that the cost of production is falling, and thus that the feared “peak oil” is far in the distance. This is not the correct interpretation, especially when many types of commodities are decreasing in price at the same time. When prices are set in a world market, the big issue is affordability. Even if food, oil and coal are close to necessities, consumers can’t pay more than they can afford.

A person can tell from Figure 1 that since the first part of 2011, the prices of Brent oil, Australian coal, and food have been trending downward. This drop in prices continues into September. For example, as I write this, Brent oil price is $97.70, while the average price for the latest month shown (August) is $105.27. It is this steeper, recent drop, which many are concerned about.

We are dealing with several confusing issues. Let me try to explain some of them.

Issue #1: Over the short term, commodity prices don’t reflect the cost of extraction; they reflect what buyers can afford.

Oil prices are set on a worldwide basis. The cost of extraction varies around the world. So it is clear that oil prices will not match the cost of extraction, or the cost of extraction plus a reasonable profit, for any particular producer.

If oil prices drop, there is a temptation to believe that this is because the cost of production has dropped. Over a long enough period, a drop in the cost of production might be expected to lead to lower oil prices. But we know that many oil producers are finding current oil prices too low. For example, the Wall Street Journal recently reported, “Royal Dutch Shell CEO: Can’t deny returns are too low. Ben van Beurden prepared to shrink company in order to boost returns, profitability.” I wrote about this issue in my post, Beginning of the End? Oil Companies Cut Back on Spending.

In the short term, low prices are likely to signal that less of the commodity can be sold on the world market. Commodities such as oil and food are very desirable products. Why would less be needed? The issue, unfortunately, is affordability. Affordability depends largely on (1) wages and (2) debt. Wages tend to be fairly stable. The likely culprit, if affordability is leading to lower demand for desirable products like oil and food, is less growth in debt.

Issue #2: Economic growth tends to produce a debt bubble.

Many economists believe that technological innovation is the key to economic growth. In my view, economies need a combination of the following to have economic growth of the type experienced in the last 100 years:1

(Increase in debt) + (cheap-to-extract fossil fuels) + (cheap-to-use non-fossil fuel resources) + (technological innovation)

In such a case, debt keeps increasing as an economy grows. Unfortunately, this economic growth is only temporary, because resources tend to become more expensive to use over time, making the “cheap” resources required for economic growth disappear.

The problem underlying the rising cost of resources (both for fossil fuels and others) is that we tend to use the cheapest-to-extract resources first. Technological innovation continues to occur, but as diminishing returns hit both fossil fuels and other resources, there are larger and larger demands on technology to keep costs in line with what workers can afford. Eventually, the cost of resources (net of technological improvements) rises too much, and economic growth is cut off. By this time, a huge mountain of debt has been built up.

Let me explain further how this happens. Without fossil fuels, the world is pretty much stuck with the goods that can be made with wood, or from other basic resources such as animal skins, cotton, flax, or clay. A small quantity of metal and glass goods can be made, but deforestation quickly becomes a problem if an attempt is made to “scale up” the quantity of goods that require heat in their production.2

Once inexpensive coal became available, its availability opened the door to technological innovation, because it provided heat in quantity that had not been available previously. While ideas such as the steam engine had been around for a long time, the availability of inexpensive coal made the production of metals needed for the steam engine, plus train tracks and railroad cars, available at reasonable cost.

With the ability to make steel and concrete in quantity (both requiring heat) came the ability to make hydroelectric dams and electrical transmission lines, thus enabling electricity for public consumption. Oil, as a liquid fuel, paved the way for widespread use of additional innovations, such as private passenger automobiles, mechanized farm equipment, and airplanes. Between coal and oil, many workers could leave farming and begin jobs in other sectors of the economy.

The transformation that took place was huge: from wooden tools and human or animal labor to a modern industrial society. How could such a big change take place? Before the change, the ability to generate a profit that might be used for future capital investment was very limited. Also, the would-be purchasers of products made in an industrial economy were very poor. I would argue that the only way of bridging this gap was debt. See my earlier posts, Why Malthus Got His Forecast Wrong and The United States’ 65-Year Debt Bubble.

The use of debt has several advantages:

Because of these issues, debt and cheap fossil fuels have a symbiotic relationship.

(1) The combination of debt, inexpensive fossil fuels, and inexpensive resources of other kinds allows the production of affordable goods that raise the standard of living of those using them. The result is what we think of as “economic growth.”

(2) The economic growth provides the additional income needed to pay back the debt with interest. The way this happens is indirectly, through what is sometimes described as “greater productivity of workers.” This greater productivity is really human productivity enhanced with devices made possible by fossil fuels, such as sewing machines, electric milking machines, and computers that allow workers to become more productive. Indirectly, the higher productivity of workers benefits both businesses and governments, through higher sales of goods to consumers and through higher taxes. In this way, businesses and governments can also repay debt with interest.

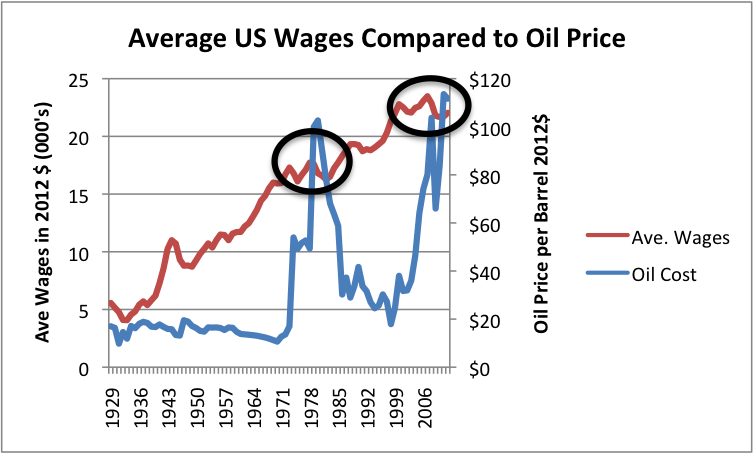

Higher-priced resources are a problem. Higher-priced resources of any kind tend to “gum up the works” of this payback cycle. Higher-priced oil in particular is a problem. In the United States, when oil prices rise above about $40 or $50 barrel, growth in wages stops.

Figure 2. Average wages in 2012$ compared to Brent oil price, also in 2012$. Average wages are total wages based on BEA data adjusted by the CPI-Urban, divided total population. Thus, they reflect changes in the proportion of population employed as well as wage levels.

With higher oil prices, the rise in the standard of living stops for most workers, and good-paying jobs become difficult to find. There are a couple of reasons we would expect wages to stagnate with higher oil prices:

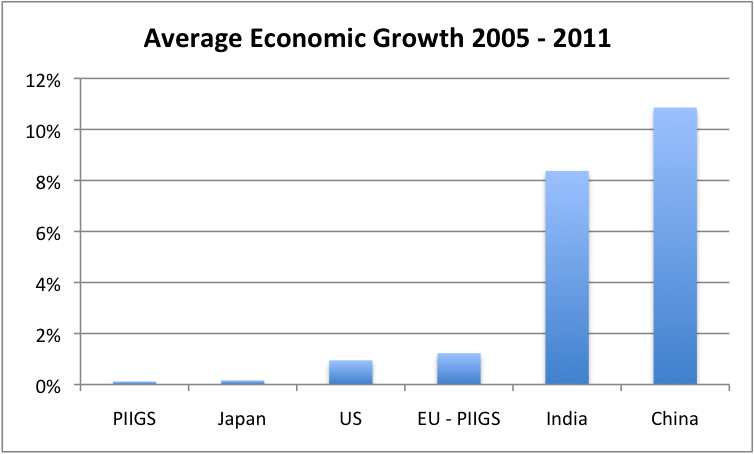

(1) Competition with cheaper energy sources. When oil prices rose, countries using a very high percentage of oil in their energy mix (such as the PIIGS in Europe, Japan, and United States) became less competitive in the world economy. They tended to fall behind China and India, countries that use much more coal (which is cheaper) in their energy mix.

Figure 3. Average percent growth in real GDP between 2005 and 2011, based on USDA GDP data in 2005 US$.

(2) Need to keep the price of goods flat. Businesses need to keep the total price of their products close to “flat” despite rising oil prices, if they are to continue to sell as much of their product after the oil price increase as previously. Oil is one major cost of production; wages are another. An obvious way to offset rising oil prices is to reduce wages. This can be done in several ways: outsourcing work to a lower cost country, greater automation, or caps on wages. Any of these approaches will tend to produce the flattening in wages observed in Figure 2.

Based on Figure 2, an oil price above $40 or $50 per barrel seems to put a cap on wages, and indirectly leads to much less economic growth. Even if we didn’t hit this oil price limit–for example, if we had discovered a liquid fuel that could be produced in quantity for less than $40 barrel–we would eventually hit some kind of growth limit. For example, the limit might be climate change or too much population for food production capability. Even too much debt can be a limit, if citizens’ incomes don’t rise in a corresponding manner. At some point, it becomes impossible even to make interest payments if the debt level is too high. Indirectly, citizens wages even support business and government debt, because business revenues and tax revenues depend indirectly on wages.

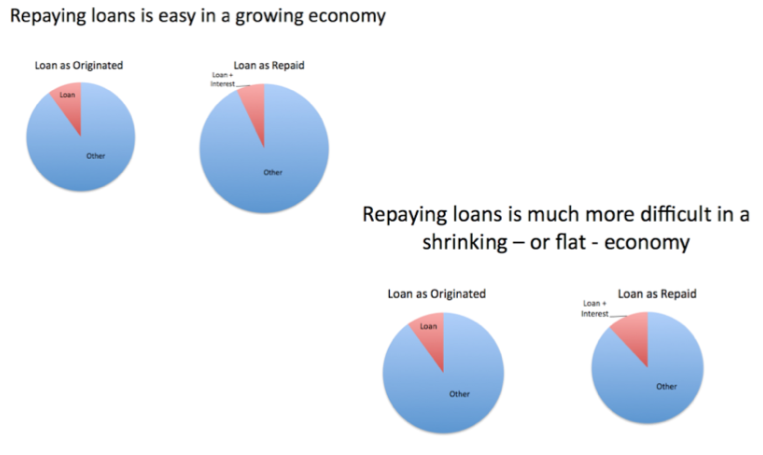

Issue #3: Repaying debt is very difficult in a flat or declining economy.

Once growth stops (or slows down too much), the debt bubble tends to crash, because it is much more difficult to repay debt with interest in a shrinking economy than in a growing one.

Figure 4. Repaying loans is easy in a growing economy, but much more difficult in a shrinking economy.

The government can hide this issue for a very long time by rolling over old debt with new debt and by reducing interest rates to practically zero. At some point, however, the system seems certain to fail.

Not all debt is equivalent. Debt that simply blows bubbles in stock market prices has little impact on commodity prices. In order to keep commodity prices high enough for producers to want to continue to produce them, the debt really has to get back into the hands of the potential buyers of the commodities.

Also, any changes that tend to reduce world trade push the world economy toward contraction, and make it harder to repay debt with interest. Thus, sanctions against Russia, and Russia’s sanctions against the US and Europe, tend to push the world toward debt collapse more quickly.

Issue #4: Rising oil and other commodity prices are a problem, especially for countries that are importers of those commodities.

Most of us are already aware of this issue. If oil prices rise, or if food prices rise, our salaries do not rise by a corresponding amount. We end up cutting back on discretionary purchases. This cutback in discretionary purchases leads to layoffs in these sectors. We end up with the scenario we had in the 2007-2009 recession: falling home prices (since higher-priced homes are discretionary purchases), failing banks, and many without jobs. See my article Oil Supply Limits and the Continuing Financial Crisis.

The reason that low oil and other commodity prices are welcomed by many people now is because the opposite–high oil and other commodity prices–are so terrible.

Issue #5: Falling oil and other commodity prices are a problem, if the cost of production is not dropping correspondingly.

If commodity prices drop for any reason–even if it is because a debt bubble is popping–it is going to affect how much companies are willing to produce. There is going to be a tendency to cut back in new production. If prices drop too far, it is even possible that some companies will leave the market altogether.

Even if it doesn’t look like a country “needs” the current high oil price, there may still be a problem. Oil exporters depend on the high taxes that they are able to obtain when oil prices are high. If they cannot collect these taxes, they may need to cut back on programs such as food subsidies and new desalination plants. Without these programs, civil disorder may lead to cutbacks in oil production.

Issue #6: The growth in oil sales to China and to other emerging markets has been fueled by debt growth. This debt growth now seems to be stalling.

Growth in oil consumption has mostly been outside of the United States, the European Union, and Japan, in the recent past. China and other emerging market countries kept demand for oil high.

Figure 5. Oil consumption by part of the world updated through 2013, based on BP Statistical Review of World Energy 2014 data.

Ambrose Evans-Pritchard reports, China’s terrifying debt ratios poised to breeze past US levels. He shows the following chart of China’s growth in debt from all sources, including shadow banking:

Figure 6. China’s total debt, based on chart displayed in Ambrose Evans-Pritchard article.

This rise in debt now seems to be slowing, based on a Wall Street Journal report. A person wonders whether this stalling debt growth is affecting world oil and other commodity prices.

Figure 7. Figure from WSJ article PBOC Struggles as Chinese Borrowers Hold Back.

Other emerging markets also seem to be experiencing cutbacks. Since 2008, the United States, Europe, and Japan have had very easy money policies. Some of the money available at low interest rates was invested in emerging markets. Now the WSJ reports, Fed Dims Emerging Markets’ Allure. According to the article investors, investors are taking a more cautious stance on new investment because of fear of rising US interest rates.

Of course, other issues affect debt and world commodity demand as well. If interest rates rise, they many have a tendency to shrink new lending, in general, because loans become less affordable. Sanctions of one country against another, such as the US against Russia, and vice versa, also tend to reduce demand.

Issue #7: Debt bubbles have been a problem in past collapses.

According to Jesse Colombo, the Depression was to a significant result the result of debt bubbles that built up during the roaring twenties. Another, longer-term cause would seem to be the loss of farm jobs that occurred when coal allowed tasks that were previously done by farm workers to be done by either electricity or by horses pulling metal plows. The combination of a debt bubble and loss of jobs seems to have parallels to our current situation.

Many believe the subprime housing bubble crash contributed to the Great Recession. The oil price spike of 2007 and 2008 played a major role as well.

Issue #8: If we are facing the collapse of a debt bubble, it is quite possible that prices of many commodities will fall. This could possibly lead to a collapse in the supply of many types of energy products, more or less simultaneously.

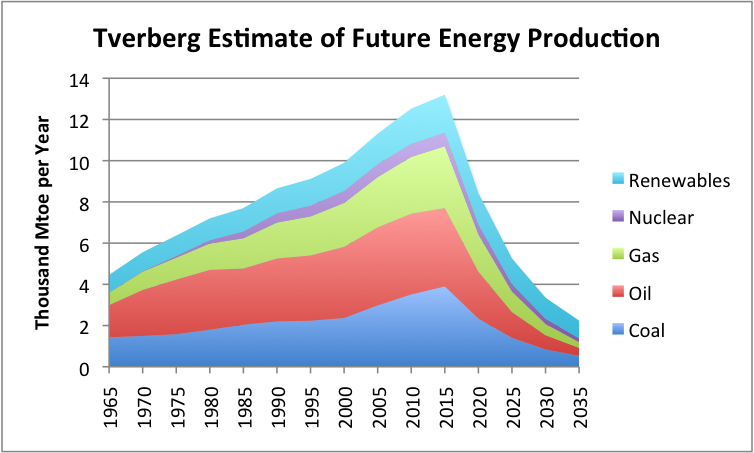

Figure 8, shown below, is a very rough estimate of the kind of decline in energy use we could be facing if a debt collapse leads to very low prices of many types of fuels simultaneously. Prices of many commodities crashed in 2008, and it was only with massive intervention that prices were propped up to 2011 levels. After the beginning of 2011, prices began sinking again, as shown in Figure 1.

Figure 8. Estimate of future energy production by author. Historical data based on BP adjusted to IEA groupings.

Clearly governments will try to prevent another sharp crash in commodity prices. The question is whether they will be successful in propping up commodity prices, and for how long they will be successful. In a finite world, fossil fuel energy production eventually must decline, but we don’t know over precisely what timeframe.

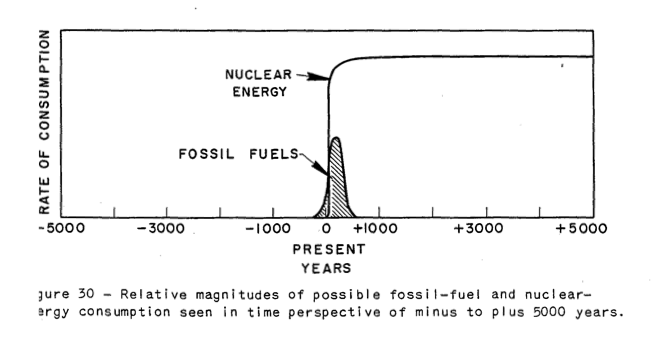

Issue #9: My steep decline contrasts with the “best case” forecast of future oil consumption given by M. King Hubbert.

M. King Hubbert wrote about a scenario where another type of fuel completely takes over, before oil and other fossil fuels are phased out. He even discusses the possibility of making liquid fuels using very cheap nuclear energy. The way he represents the situation is the following:

Figure 9. Figure from Hubbert’s 1956 paper, Nuclear Energy and the Fossil Fuels.

In such a scenario, it is possible that oil supply will begin to decline when approximately 50% of resources are exhausted, and the down slope of the curve will follow a symmetric “Hubbert curve.” This situation seems to represent a best possible case; it doesn’t seem to represent the case we are facing today. If a debt collapse occurs, much of the remaining fuel is likely to stay in the ground.

Issue #10: Our economy is a networked system. Increasing debt is what keeps the economy inflated. If wages fail to keep pace with debt growth, the system seems likely to eventually crash.

In previous posts, I have represented the economy as a self-organized networked system, consisting of businesses, consumers, governments (with laws, regulations, and taxes), financial system, and international trade.

Figure 10. Dome constructed using Leonardo Sticks

One reason the economy is represented as hollow is because the economy loses its capability to make goods that are no longer needed–such as buggy whips and rotary dial phones. Another reason why it might be represented as hollow is because debt is used to “puff it up” to its current size. Once the amount of debt starts shrinking, it makes it very difficult for the economy to maintain its stability.

Many “peak oilers” believe that if we have a problem with the financial system, all we have to do is start over with a new one–perhaps without debt. Everything I can see says that debt is an essential part of the current system. We could not extract fossil fuels in any significant quantity, without an ever-rising quantity of debt. The problem we are encountering now is that once resource costs get too high, the debt-based system no longer works. A new debt-based financial system likely won’t work any better than the old one.

If we try to build a new system without fossil fuels, we will be really starting over, because even today’s “renewables” are part of the fossil fuel system.3 We will have to go back to things that can be made directly from wood and other natural products without large amounts of heat, to have truly renewable resources.

Notes:

[1] This is really a simplification of the real issues. As world population grows, it is necessary to obtain an increasing amount of food from the same arable land. Thus, it is necessary to find new processes to increase food production, at the same time that soil is quite possibly degrading. Soil is in a sense a “resource other than fossil fuels,” but I have not mentioned this issue specifically.

Growing pollution problems are in some sense an indirect cost of extracting fossil fuels and other resources. These represent another growing cost that I have not specifically identified. Furthermore, there are indirect expenses that do not fit neatly into any category, such as required desalination plants to handle growing populations in areas where water is scarce. We may need to consider mitigation expenses of all types as part of the “cost of resource extraction.”

My point is that it becomes increasingly difficult to offset these many cost increases with technological innovations. Furthermore, if no changes are made, a larger and larger share of both the workforce and resources are required for maintaining the status quo, leaving fewer workers and a smaller quantity of resources to “grow” the economy.

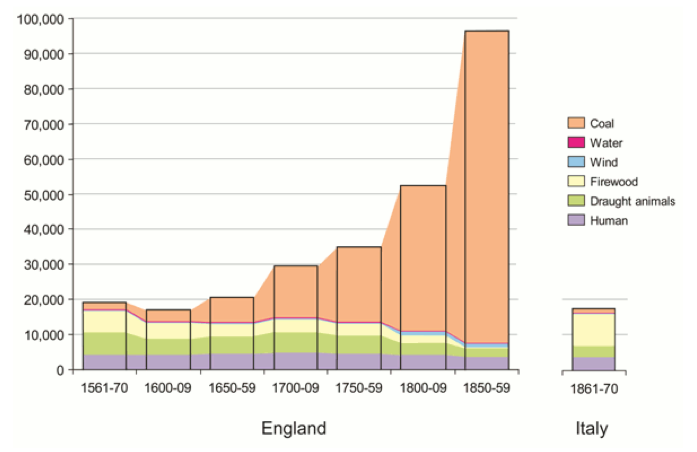

[2] Wind and water are additional sources of energy, but they are sources of mechanical energy, not heat energy, so are not helpful unless they can be converted first to electricity, and then to heat. In quantity, they never were very large in pre-fossil fuel days.

Figure 11. Annual energy consumption per head (megajoules) in England and Wales 1561-70 to 1850-9 and in Italy 1861-70. Figure by Tony Wrigley from Opening Pandora’s Box. Figure originally from Energy and the English Industrial Revolution, also by Tony Wrigley.

[3] Of course, any existing “renewable” will continue to work until it needs repairs that are unavailable. Other parts of the system (such as electric transmission lines, batteries, inverters, and attached devices such as pumps) may fail more quickly than the renewables themselves.

by Charles Hugh Smith

As things get dicier globally, assets in periphery nations typically get dumped as mobile capital flees risk and migrates to lower risk core nations and currencies.

I received many thoughtful comments on Why the Dollar May Remain Strong For Longer Than We Think. Given the many weaknesses of the U.S.--ballooning social-welfare and crony-capitalist liabilities, free money for financiers monetary policies, etc.--a strengthening dollar (USD) strikes many as counter-intuitive.

The dynamic complexities of fiscal and monetary policies, global capital flows and the foreign exchange (FX) market complicate any inquiry, so I try to keep it simple.

In my view, the USD serves both transactional (global trade) markets and the global need for currency reserves (i.e. as a store-of-value). Sorting out the various influences on its relative value in each capacity is complex enough, but there is also the X Factor--the hard-to-quantify components of any currency's relative value.

For the USD, the X Factor is hegemony, which includes financial dominance based on debt issued/denominated in USD and what might be called the real-world assets of the issuing nation: that nation's food, energy and water security (what I call the FEW resources), its proximity to potential enemies, its external environmental costs, its overseas financial assets, the strength of its legal system in protecting private assets,its demographic profile and of course its ability to project power to defend its interests.

By these basic measures, the U.S. scores pretty well. We can get some perspective on this by putting ourselves in the shoes of wealthy people in periphery nations where the risks of capital controls, currency devaluation, etc. are perceived to be high, or in the shoes of corrupt elites in countries where they fear their ill-gotten gains might not survive blowback (hence the almost universal desire of elites to leave China with their loot).

The strength of the USD is attractive to at-risk capital, even if transferring at-risk wealth into dollars requires a significant foreign-exchange haircut. Better to preserve 75% of your wealth in USD than leave it exposed to confiscation, capital control, etc. This is the basic flight-to-safety mechanism.

Ubiquity also counts. The USD is the proxy global currency. A $100 USD bill is recognized as money virtually everywhere. If you're stranded just about anywhere, USD will buy you food, transport, official "assistance" via bribes, etc. No other paper currency is even close to ubiquity/recognition. (Clean, crisp $100 USD bills are recommended--dirty crumpled bills are not highly esteemed.)

It's also critical to look at the relative scale of the money-printing that erodes the value of currencies: -China's credit expansion is much larger as a percentage of its economy and financial system than the Fed's money-printing as a percentage of the U.S. financial system.

Then there's the scramble-for-yield issue: imagine you're managing $10 billion. You need to preserve this wealth but you also need to earn a yield, or you'll be fired at the end of the quarter. Since FX (foreign exchange) is a much larger market than stocks or bonds, you're highly attuned to FX so you don't get blindsided by a shift in FX that wipes out your yield. You might wisely build an "insurance" position in precious metals, but because you need yield then you have exposure to bonds, stocks and as a result, FX.

As things get dicier globally, assets in periphery nations typically get dumped as mobile capital flees risk and migrates to lower risk core nations and currencies.

For money managers, the USD is an FX safe haven--especially since the capital flowing out of the riskier periphery pushes the USD higher. This makes for a secondary yield--as the USD rises, any asset denominated in USD will gain in relative value. So there's a self-reinforcing feedback loop: as the USD value rises, it attracts more of the money fleeing risk.

In a way, the USD acts as a currency equivalent of the English language. There are many languages and many currencies, but at present the indispensable language/currency in the global economy is English/USD.

How can we summarize this discussion?

1. FX is the "master market" of the global financial system.

2. The flow of mobile capital out of the periphery into the core will turn into a flood as global risks rise.

Both of these conditions favor the USD.

by Sober Look

The take-up of the ECB's TLTRO program announced back in June was materially lower than expected. About €83bn worth of cheap long-dated loans was picked up by the area's banking system. Many had expected €150bn and even greater. Part of the reason is that banks that are not quite ready to deploy the funds don't want to sit on cash with negative rates. As a result some have concluded that the Eurozone's credit contraction will worsen from here and economic conditions will deteriorate further.

As views of doom and gloom envelop the Eurozone, it may be time time for a contrarian view: the euro area's economy is turning the corner. Yes, it's difficult to imagine such a thing and we are sure to get numerous angry emails and comments. Ultimately it's about the data.

First of all we start with the Eurozone's inflation expectations which continue to fall. That combined with a weaker than expected TLTRO take-up will keep the ECB highly active in its easing efforts, potentially even considering QE.

Market-implied inflation expectations 5 years out (source: DB)

It's important to keep in mind that the ECB is trying to replace at least in part the 3yr LTRO and MRO loans that banks have been repaying. These repayments have resulted in an unprecedented reduction in the central bank (Eurosystem) balance sheet since the beginning of last year.

Eurosystem (central bank) balance sheet (source: ECB)

Without a strong take-up in the TLTRO, the ECB will consider other options to expand the balance sheet. The planned ABS purchases will hardly make a dent because the new Basel Accord has all but destroyed that market. Therefore there will be pressure on the ECB to do something else in order to stem the decline in its balance sheet. Plus we are already seeing EU institutions calling on the BIS to loosen regulatory capital rules for structured credit issuance. All of this is positive for the Eurozone banks and will likely expand liquidity in the system. That's in part why we've had a nice pop in euro area bank shares recently.

FTSEurofirst 300 Banks Index Index Price (source: MarketWatch)

Interestingly, a number of analysts have been pointing out that the Eurozone bank deleveraging is over. Credit contraction in the area is ending. One can see glimpses of this in the area's money supply measures which have stabilized recently.

Euro area M3 money supply (source: ECB)

To some extent Mario Draghi has already generated some degree of stimulus for the area's economy by repricing the euro (via negative domestic deposit rates). This is a gift for German and other exporters who can now more effectively compete on the international markets.

EUR/USD (source: TradingView)

We may already be witnessing the impact of weaker euro, as German trade balance jumped recently, resulting in better than expected German industrial production report.

Source: Investing.com

Improved German exports (see chart) combined with several other factors have resulted in higher than expected growth in industrial production for the Eurozone as a whole.

Source: Investing.com

There is no question that the Eurozone's economy continues to struggle. Issues such as the recession in Italy, manufacturing stagnation in France, and massive unemployment across the area are not going away anytime soon. China's economy and the situation in Ukraine continue to pose risks. Surveys still show worsening business and consumer sentiment. But the expectations around the area's performance have been so bad lately, surprises to the upside are increasingly likely (see example). The ECB's aggressive easing stance as well as stronger trade and industrial activity data tell us that for now the worst of the euro area slowdown may be over.

By John Mauldin

In 1633 Galileo Galilei, then an old man, was tried and convicted by the Catholic Church of the heresy of believing that the earth revolved around the sun. He recanted and was forced into house arrest for the rest of his life, until 1642. Yet “The moment he [Galileo] was set at liberty, he looked up to the sky and down to the ground, and, stamping with his foot, in a contemplative mood, said, Eppur si muove, that is, still it moves, meaning the earth” (Giuseppe Baretti in his book the The Italian Library, written in 1757).

Flawed from its foundation, economics as a whole has failed to improve much with time. As it both ossified into an academic establishment and mutated into mathematics, the Newtonian scheme became an illusion of determinism in a tempestuous world of human actions. Economists became preoccupied with mechanical models of markets and uninterested in the willful people who inhabit them….

Some economists become obsessed with market efficiency and others with market failure. Generally held to be members of opposite schools – “freshwater” and “saltwater,” Chicago and Cambridge, liberal and conservative, Austrian and Keynesian – both sides share an essential economic vision. They see their discipline as successful insofar as it eliminates surprise – insofar, that is, as the inexorable workings of the machine override the initiatives of the human actors. “Free market” economists believe in the triumph of the system and want to let it alone to find its equilibrium, the stasis of optimum allocation of resources. Socialists see the failures of the system and want to impose equilibrium from above. Neither spends much time thinking about the miracles that repeatedly save us from the equilibrium of starvation and death.

– George Gilder, Knowledge and Power: The Information Theory of Capitalism and How It is Revolutionizing Our World

And to that stirring introduction let me just add a warning up front: today’s letter is not exactly a waltz in the park. Longtime readers will know that every once in a while I get a large and exceptionally aggressive bee in my bonnet, and when I do it’s time to put your thinking cap on. And while you’re at it, tighten the strap under your chin so it doesn’t blow off. There, now, let’s plunge on.

Launched by Larry Summers last November, a meme is burning its way through established academic economic circles: that we have entered into a period of – gasp! – secular stagnation. But while we can see evidence of stagnation all around the developed world, the causes are not so simple that we can blame them entirely on the free market, which is what Larry Summers and Paul Krugman would like to do: “It’s not economic monetary policy that is to blame, it’s everything else. Our theories worked perfectly.” This finger-pointing by Keynesian monetary theorists is their tried and true strategy for deflecting criticism from their own economic policies.

Academic economists have added a great deal to our understanding of how the world works over the last 100 years. There have been and continue to be remarkably brilliant papers and insights from establishment economists, and they often do prove extremely useful. But as George Gilder notes above, “[As economics] ossified into an academic establishment and mutated into mathematics, the Newtonian scheme became an illusion of determinism in a tempestuous world of human actions.”

Ossification is an inherent tendency of the academic process. In much of academic economics today, dynamic equilibrium models and Keynesian theory are assumed a priori to be correct, and any deviation from that accepted economic dogma – the 21st century equivalent of the belief by the 17th century Catholic hierarchy of the correctness of their worldview – is a serious impediment to advancement within that world. Unless of course you are from Chicago. Then you get a sort of Protestant orthodoxy.

It’s About Your Presuppositions

A presupposition is an implicit assumption about the world or a background belief relating to an utterance whose truth is taken for granted in discourse. For instance, if I asked you the question, “Have you stopped eating carbohydrates?” The implicit assumption, the presupposition if you will, is that you were at one time eating carbohydrates.

Our lives and our conversations are full of presuppositions. Our daily lives are based upon quite fixed views of how the world really works. Often, the answers we come to are logically predictable because of the assumptions we make prior to asking the questions. If you allow me to dictate the presuppositions for a debate, then there is a good chance I will win the debate.

The presupposition in much of academic economics is that the Keynesian, and in particular the neo-Keynesian, view of economics is how the world actually works. There has been an almost total academic capture of the bureaucracy and mechanism of the Federal Reserve and central banks around the world by this neo-Keynesian theory.

What happens when one starts with the twin presuppositions that the economy can be described correctly using a multivariable dynamic equilibrium model built up on neo-Keynesian principles and research founded on those principles? You end up with the monetary policy we have today. And what Larry Summers calls secular stagnation.

First, let’s acknowledge what we do know. The US economy is not growing as fast as anyone thinks it should be. Sluggish is a word that is used. And even our woeful economic performance is far superior to what is happening in Europe and Japan. David Beckworth (an economist and a professor, so there are some good guys here and there in that world) tackled the “sluggish” question in his Washington Post “Wonkblog”:

The question, of course, is why growth has been so sluggish. Larry Summers, for one, thinks that it’s part of a longer-term trend towards what he calls “secular stagnation.” The idea is that, absent a bubble, the economy can’t generate enough spending anymore to get to full employment. That’s supposedly because the slowdowns in productivity and labor force growth have permanently lowered the “natural interest rate” into negative territory. But since interest rates can’t go below zero and the Fed is only targeting 2 percent inflation, real rates can’t go low enough to keep the economy out of a protracted slump.

Rather than acknowledge the possibility that the current monetary and government policy mix might be responsible for the protracted slump, Summers and his entire tribe cast about the world for other causes. “The problem is not our theory; the problem is that the real world is not responding correctly to our theory. Therefore the real world is the problem.” That is of course not exactly how Larry might put it, but it’s what I’m hearing.

It’s been more than five years since the global financial crisis, but developed economies aren’t making much progress. As of today, the United States, Canada, Germany, France, Japan, and the United Kingdom have all regained their pre-crisis peaks in real GDP, but with little else to show for it.

Where orthodox neo-Keynesian policies like large-scale deficit spending and aggressive monetary easing have been resisted – as in Japan years ago or in the Eurozone debtor countries today – lingering depressions are commonly interpreted as tragic signs that “textbook” neo-Keynesian economic policy could have prevented the pain all along and that weak economic conditions persist because governments and central banks are not doing enough to kick-start aggregate demand and stimulate credit growth at the zero lower bound.

In places like the United States and Japan, where neo-Keynesian thought leaders have already traded higher public debt levels and larger central bank balance sheets for unspectacular economic growth and the kinds of asset bubbles that always lead to greater instability in the future, their policies have failed to jump-start self-accelerating recoveries. Even in the United States, when QE3 has been fully tapered off, I would expect to see the broader economy start to lose momentum once again.

We’ve tried countercyclical deficit spending to resist recessions, procyclical (and rather wasteful) deficit spending to support supposed recoveries, and accommodative monetary easing all along the way (to lower real interest rates and ease the financing of those pesky deficits); but growth has been sluggish at best, inflation has been hard to generate, and labor market slack is making it difficult to sustain inflation even when real interest rates are already negative.

Call me a heretic, but I take a different view than the economists in charge. To my mind, the sluggish recovery is a sign that central banks, governments, and, quite frankly, the “textbook” economists (despite their best intentions) are part of the problem. As Detlev Schlichter commented in his latest blog post (“Keynes was a failure in Japan – No need to embrace him in Europe”), “To the true Keynesian, no interest rate is ever low enough, no ‘quantitative easing’ program ever ambitious enough, and no fiscal deficit ever large enough.” It’s apparently true even as debt limits draw closer.

While the academic elites like to think of economics as a reliable science (with the implication that they can somehow control a multi-trillion-dollar economy), I have repeatedly stressed the stronger parallel of economics to religion, in the sense that it is all too easy to get caught up in the dogma of one tradition or another. And all too often, a convenient dogma becomes a justification for those in power who want to expand their control, influence, and spending.

Whereas an Austrian or monetarist approach would suggest less government and a very light handle on the monetary policy tiller, Keynesian philosophy gives those who want greater government control of the economy ample reasons to just keep doing more.

Schlichter expands his critique of the logic of pursuing more of the same debt-driven policies and highlights some of the obvious flaws in the pervasive Keynesian thinking:

Remember that a lack of demand is, in the Keynesian religion, the original sin and the source of all economic troubles. “Aggregate demand” is the sum of all individual demand, and all the individuals together are not demanding enough. How can such a situation come about? Here the Keynesians are less precise. Either people save too much (the nasty “savings glut”), or they invest too little, maybe they misplaced their animal spirits, or they experienced a Minsky moment, and took too much risk on their balance sheets, these fools. In any case, the private sector is clearly at fault as it is not pulling its weight, which means that the public sector has to step in and, in the interest of the common good, inject its own demand, that is [to] “stimulate” the economy by spending other people’s money and print some additional money on top. Lack of “aggregate demand” is evidently some form of collective economic impotence that requires a heavy dose of government-prescribed Viagra so the private sector can get its aggregate demand up again.

Generations of mismanagement have left major economies progressively weaker, involving

But rather than recognizing real-world causes and effects, neo-Keynesian ideologues are making dangerous arguments for expanding the role of government spending in places where government is already a big part of the problem.

We are going to delve a little deeper into this thesis of “secular stagnation” posited last year by Larry Summers and eagerly adopted by Paul Krugman, among others; and then we’ll take a trip around the rich world to assess the all-too-common trouble with disappointing growth, low inflation, and increasingly unresponsive labor markets. Then I’ll outline a few reasons why I think the new Keynesian mantra of “secular stagnation” is nothing more than an excuse for more of the same failed policies.

I think we’ll see a consistent theme: fiscal and monetary stimulus alone cannot generate “financially stable growth with full employment.” In fact, such policies only make matters worse. And funny things happen in the Keynesian endgame.

USA: Secular Stagnation or Public Sector Drag?

This latest theory – “secular stagnation” – argues that powerful and inherently deflationary forces like shrinking populations…

… and potentially slowing productivity growth (as posited by Northwestern University professor Bob Gordon)…

… are adding to the deleveraging headwinds that always follow debt bubbles. According to the “stagnation” theory, structural forces have been bearing down on the natural rate of interest and weighing on the full-employment level of economic growth since the early 1980s; but the slowdown in trend GDP growth has been masked by a series of epic bubbles in technology stocks and housing.

Even before the 2008 crisis, the argument goes, the real interest rate required to restart the business cycle had been trending lower and lower for years, and the average level of growth experienced during business cycles has fallen.

Moreover, it has taken longer and longer to recoup the jobs that were lost in each of the last three recoveries.

It’s hard to argue with the data, but it’s really a matter of how we interpret it. While the five-year-old “recovery” is still the weakest business cycle in modern US history…

… I quite frankly still believe the effects on growth are temporary. Difficult and long-lasting, for sure (as Jonathan Tepper and I outlined in our books Endgame and Code Red), but temporary nonetheless as private-sector deleveraging continues. We have encountered a massive debt crisis and still have a long way to go in dealing with the sovereign debt bubbles that are being created in Europe and Japan – with the potential of one’s ballooning out of control in the US unless we turn ourselves around.

It may take a crisis, but the forces that plague rich-world economies will eventually shake out and usher in a new era of technology-driven growth. In other words, this too shall pass… but continuing with the same old policies is highly likely to create another crisis through which we all must pass first.

Yes, shrinking workforces, private-sector debt overhangs, and technological innovation are making it difficult to achieve “financially stable growth with full employment” (quoting Summers); but governments and central banks are themselves becoming an increasing drag on rich-world economies. Our governments have saddled us with excessive public debt, onerous overregulation, oppressive tax codes, and their attendant distorted market signals; while our central banks have engaged in currency manipulation and monetary-policy overmanagement. Those in power who rely on Keynesian policies almost always find it inconvenient to cut back in times of relative economic strength (as Keynes would have had them do). And if, according to their arguments, the economy is still too weak even in periods of growth to enable the correction of government balance sheets, then perhaps their reluctance has something to do with debt piling up, market signals being distorted, and governments being empowered to encroach on every aspect of the lives of their productive citizens .

My friend Grant Williams used this chart in a speech yesterday. It shows that we have come to need ever more debt just to produce the same amount of GDP. With a deleveraging in the private sector underway, it is no wonder that growth is under pressure.

Debt is simply future consumption brought forward. Another way to think about it is that debt is future consumption denied. But there comes a point when debt has to be repaid, and by definition, from that point forward there is going to be a period of slower growth. I have called that point the Endgame of the Debt Supercycle, and it was the subject of my book Endgame.

As a result of central bank and governmental machinations, Keynesian growth is ultimately debt-fueled growth (either through the swelling of public debt via deficit spending or the accumulation of private debt via credit expansion); and eventually, public and private balance sheets run out of room to expand anymore. It has taken decades for cracks to show up in the prevailing theory, but now the cracks are everywhere.

One place where the crack-up is especially evident is Japan, where an uber-Keynesian combination of aggressive fiscal deficits and a planned doubling in the monetary base started to lift real GDP and inflation numbers last year before falling back into a deflationary trap. Yet the Japanese experience has seemingly convinced ECB President Mario Draghi that similar policies should be implemented across the Eurozone.

Last quarter, the Japanese economy shrank by an annualized 7.1%; business investment fell by 5.1%; and residential spending was down 10%. This is after one of the most massive Keynesian quantitative easing efforts in the history of the world.

So, let’s go to Japan, which may now have to retitle itself “the land of the setting sun,” since it is facing the steepest expected decline in population and in workforce-to-population ratio on the planet.

Japan’s long-awaited “recovery” is already losing steam without the effective implementation of Prime Minister Shinzo Abe’s “third arrow” of structural reform, which to my mind was always the most critical element of his entire “Abenomics” project (and of course the most politically difficult). Despite massive fiscal and monetary stimulus and a desperate attempt to boost tax revenues by hiking the sales tax this past April, Japanese GDP collapsed in Q2:

Let’s review how Japan got there.

Prime Minister Abe took office in late December 2012 and, together with his (initially reluctant) colleagues at the Bank of Japan, quickly fired the first two fiscal and monetary policy arrows, which aimed to propel the world’s third-largest economy out of its deflationary trap. The third arrow has yet to fly.

Source: Wall Street Journal, March 2013

Since January 2013 the Bank of Japan has expanded its balance sheet by 78% (42% on an annualized basis)…

… and pushed the USD/JPY exchange rate to a six-year low of a fraction under 109 yen per dollar as of the market close yesterday.

In true Keynesian form, the Japanese government ran a massive fiscal deficit in 2013, equivalent to 8.4% of GDP. This was its 22nd consecutive year of deficit spending, starting in mid-1992…

… despite the fact that the Japanese public-sector debt-to-GDP ratio is quickly approaching 250%:

While inflation has popped to its highest level since the early 1990s…

… headline CPI has been decelerating since May and could quickly revert to deflation in the event of continued economic weakness, as was the case after the 1997 tax hike… which would then bring on even more “money-financed” deficit spending.

Abe advisor Etsuro Honda was very clear on this point: “Regardless of the next sales tax hike, it could be that additional monetary easing might be called for if inflation and demand fail to pick up and the output gap doesn’t narrow…. I can fully see the possibility that such a situation will occur.”

Of course, the party cannot go on forever. More than twenty years of constant deficit spending and public-sector debt growth have finally led to a situation where debt service and entitlements are crowding out the government’s general budget.

And now the situation is turning dangerous. Japan has been flirting with current account deficits for the past few years, and the trend looks decidedly negative over the coming decade. That, in turn, could force the Abe administration to look for foreign investment to fund its ongoing operations, pushing interest rates up dramatically to the point that debt service and entitlements could consume more than half the annual operating budget.

Bottom line: Abenomics has delivered a bounce in economic growth and inflation, but it’s failing to push Japan into a self-sustaining recovery. Without a detour through structural reforms (which would be quite painful), this road leads to higher public debt balances and even more dysfunction in the medium term, leaving Japan only a shock away from disaster. As predicted here three years ago, I continue to believe that the yen will be over 200 to the dollar by the end of the decade, and possibly much sooner.

Keynesians argue that Abe had the right idea, he just didn’t spend enough and will need to spend a lot more in the near future. In other words, fiscal and monetary stimulus can lift inflation and boost growth in the short term… but the problem is that you can’t have that stimulus if you want to consolidate the national debt and boost tax revenues at the same time.

Some economists would argue that Abe’s policies don’t necessarily have to add to the debt load, as long as the government has a firm commitment from the central bank to monetize the debt along the way. The fact that that would destroy the buying power of the yen doesn’t seem to be a consideration for them. The elderly on fixed incomes might disagree.

So with their highly leveraged banking system and already crushing sovereign debt loads, why wouldn’t the Europeans embrace the same model?

I’ve written extensively on the Eurozone in recent months, so I will keep this section brief.

Much of Southern Europe has been mired in depression, with hopelessly slow or negative growth rates, low inflation or outright deflation, and extremely high levels of unemployment (especially among young workers), for several years.

It’s a toxic situation for a multi-country monetary system that still lacks the underpinning of banking or fiscal unions. Demonstrations in the Catalonia region of Spain, inspired by this week’s Scottish referendum, reveal the very real political risks that are only growing with voter frustration.

Perhaps it was just talk, but Mario Draghi laid out a three-point plan similar to Abe’s in his presentation at the recent Jackson Hole meeting of central bankers. It quickly acquired the sobriquet “Draghinomics.”

Draghi recently cut the ECB’s already-negative interest rates and has promised a large round of quantitative easing. But the core problems facing Europe are not interest rates or a lack of liquidity but rather a structurally unwieldly labor market, too many regulations being dreamed up in Brussels, a lack of capital available to small businesses, and major regulatory headwinds for business startups.

Compound all that with the significant structural imbalances between Northern and Southern Europe, dramatically overleveraged banks, and an obvious sovereign debt bubble, and you have all the elements of a major crisis in the making.

That the Eurozone is a fragile and politically unstable union will come as no surprise to Thoughts from the Frontline readers who have been diligently perusing my letters for the past several years, but it is a critical point that we cannot ignore. How, I wonder, can Draghi even hope for a successful European implementation of a three-point plan like Japan’s – where a leader who started with very strong approval ratings has burned through most of his political capital before structural reforms have even gotten off the ground?

Draghi simply does not have the political power to make the changes that are necessary. All he can do is prop up a failing system with liquidity and low rates, which will ultimately create even more serious problems.

The Failure of Monetary Policy

There are many economists, with Paul Krugman at their fore, who believe that Keynesian monetary policy is responsible for the United States doing better than Europe. I beg to differ. The United States is outshining Europe due to the combined fortuitous circumstances of massive new discoveries of unconventional oil and gas, new technologies, and an abundance of risk-taking entrepreneurs. Indeed, take away the oil boom and the technology boom centered in Silicon Valley, and the US would be as sclerotic as Europe is.

None of the above has anything to do with monetary policy. In fact, I would argue that current monetary, fiscal, and regulatory policy is getting in the way of that growth.

Robert A. Hefner III, chairman of The GHK Companies and the author of The Grand Energy Transition: The Rise of Energy Gases, Sustainable Life and Growth, and the Next Great Economic Expansion, wrote a wonderful piece in last month’s Foreign Affairs, entitled “The United States of Gas” (hat tip, Dennis Gartman).

Consider how much can change in one year alone. In 2013, on properties in Oklahoma in which the GHK Companies hold interests covering 150 square miles, one large U.S. independent company drilled and completed over 100 horizontal wells. Had those wells been drilled vertically, they would have exposed only about 1,000 feet of shale, whereas horizontal drilling allowed nearly 100 miles to be exposed. And rather than performing the 100 injections of fracking fluid that a vertical well would have made possible, the company was able to perform between 1,000 and 2,000 of them. The company’s engineers also tinkered with such variables as the type of drill bits used, the weight applied while drilling, the rotation speed of the drill, and the size and number of fracking treatments.

Thanks to that continuous experimentation, plus the savings from scale (for example, ordering tubular steel in bulk), the company managed to slash its costs by 40 percent over 18 months and still boost its productivity. The result: in 2014, six or seven rigs will be able to drill more wells and produce as much oil and gas as 12 rigs were able to the year before. Since the shale boom began, over a decade ago, companies have drilled about 150,000 horizontal wells in the United States, a monumental undertaking that has cost approximately $1 trillion. The rest of the world, however, has drilled only hundreds of horizontal wells. And because each borehole runs horizontally for about one mile (and sometimes even two miles) and is subjected to ten or more fracking injections, companies in the United States have fracked about 150,000 miles of shale about two million times. That adds up to around a thousand times as much shale exposed inside the United States as outside it.

There is a divide in the United States, and indeed in the world, between those who believe (and the emphasis is on believe) that government in all its various shapes and sizes is the font of all growth and progress and those who believe that it is individual effort and free markets that “move the ball down the field” of human progress. Count me in the latter group.

Government is necessary to the extent that we need to maintain a level playing field and proper conduct, but with the recognition that wherever government is involved there are costs for that service that must be paid by the private market and producers. For example, almost everyone thinks that the government’s being involved in student loans is a public good. We should help young people with education, right? Except that John Burns released a report this week that shows that student loans will cost the real estate industry 414,000 home sales. Young people are so indebted they can’t afford to buy new homes. Collateral damage?

The unintended consequences of government policies and manipulation of the markets are legendary. But often unseen.

Monetary policy as it is currently constructed is only marginally helping private markets and producers. Monetary policy as it is currently practiced is an outright war on savers, which sees them as collateral damage in the Keynesian pursuit of increased consumer demand.

It is trickle-down monetary policy. It has inflated the prices of stocks and other income-producing securities and assets, enriching those who already have assets, but it has done practically nothing for Main Street. It has enabled politicians to avoid making the correct decisions to create sustainable growth and a prosperous future for our children, let alone an environment in which the Boomer generation can retire comfortably.

It is a pernicious doctrine that refuses to recognize its own multiple failures because it starts with the presupposition that its theory cannot fail. It starts with the presuppositions that final consumer demand is the end-all and be-all, that increased indebtedness and leverage enabled by lower rates are good things, and that a small room full of wise individuals can successfully direct the movement of an entire economy of 300 million-plus people.

The current economic thought leaders are not unlike the bishops of the Catholic Church of 16th-century Europe. Their world was constructed according to a theory that they held to be patently true. You did not rise to a position of authority unless you accepted the truth of that theory. Therefore Galileo was wrong. They refused to look at the clear evidence that contradicted their theory, because to do so would have undermined their power.

Current monetary and fiscal policy is leading the developed world down a dark alley where we are all going to get mugged. Imbalances are clearly building up in almost every corner of the market, encouraged by a low-interest-rate regime that is explicitly trying to increase the risk-taking in the system. Our Keynesian masters know their policies and theories are correct – we must only give them time to more perfectly practice them. That the results they’re getting are not what they want cannot be their fault, because the theory is correct. Therefore the problem has to lie with the real world, full of imperfect people like you and me.

What our leaders need is a little more humility and a little less theory.

Washington DC, Dallas, Chicago, Athens (Texas), and Boston

I find myself in the Hill Country north of San Antonio, Texas, attending the Casey Research Summit, where I speak tomorrow. I’m surrounded by many friends in very pleasant circumstances. And when I hit the send button, I will have two days of fascinating conversations ahead of me. I am doing a number of videos with various interesting personalities, which we will post on the Mauldin Economics site in the coming weeks. More on that later.

On Monday I fly back to Dallas, where I will stay until the end of the month, then head off to Washington DC. In the middle of October I’ll visit Chicago, Athens (Texas), and Boston, all in one week.

I can't hit the send button without noting that Jack Ma, the Chinese ultra-billionaire founder of Alibaba, was at the New York Stock Exchange for the launch of his IPO and sought out my friend Art Cashin, saying “I can't leave without a picture with Art Cashin.” As one of Art's friends subsequently wrote on our round-robin group email, Jack is clearly a man who understands who is really running things. The incident also shows that anyone can be a groupie. But what really intrigues me is that here is one of the richest men in the world, a force in China, obsessively focused on creating a merchandising machine, and yet he is so in touch with the world of investment and business that he watches CNBC enough to know who Art is. And to appreciate the character and class that Art has shown us for years – and want to meet him. Jeff Bezos may have his work cut out for him in the coming years.

By Chris Ebert

The best time to prepare for a Bear market, as with any foreseeable disaster, is long before it strikes. If one waits for word of a Bear market to be broadcast on the evening news, chances are good that it is already too late to prepare.

It’s too late to build a storm cellar when the tornado sirens are blaring, too late to get off the volcano when the pyroclastic flows have begun, and too late to buy bread and milk when the blizzard winds are howling. The best one can normally hope for, when a disaster is already underway, is to mitigate the damage; and that includes stock market crashes.

The problem with preparing for disaster is that there is a natural tendency to become desensitized to warnings that later prove inaccurate. As television’s Simpsons character Troy McClure observed many years ago, in 1995, “phony tornado alarms reduce readiness”. So to do phony predictions of coming stock market crashes reduce readiness.

Many have viewed the widely circulated charts showing the similarities of the current stock market to that of the Crash of 1929. While it is conceivable that such similarities could indeed mean we are headed for another stock market crash, the truth is that so many similar predictions have failed in the past that even if this one proves to be true it will likely be ignored, quite like phony tornado alarms.

As with any indicator, including stock market indicators, the value of the indicator depends on its ability to avoid as many false alarms as possible, while retaining the ability to send all valid alarms with enough advance notice to allow for time to prepare. Too many issued false alarms, too many missed valid alarms, or too many valid alarms issued too late, make any indicator useless.

With those constraints in mind, here is a nearly foolproof means of analyzing stock options in order to warn of a Bear market affecting the stocks in the S&P 500 while there is still time to prepare.

You are here – Bull Market Stage 1 – the “Digesting Gains” Stage.

On the chart above there are 3 categories of option trades: A, B and C. For this past week, ending September 6, 2014, this is how the trades performed on the S&P 500 index ($SPY):

Using the chart above, it can be seen that the combination, A+ B+ C-, occurs whenever the stock market environment is at Bull Market Stage 2, known here as the digesting gains stage. This stage gets its name from the tendency for stocks to experience periods of gains interspersed with significant pullbacks, as if traders are taking time to digest each individual gain. Digestion is often bullish, but not nearly as bullish as the recent lottery fever of Stage 1 which occurred in late August and early September.

A chart describing all of the different Options Market Stages is available by clicking the link at the left.

What is a Bear market?

In order to sound the alarm signaling the presence of a Bear market, the first step is to define exactly what a Bear market is. Such a task may seem simple enough, but it is not.

Take a typical definition of a Bear market being a 20% decline in stock prices. If every 20% decline in stock prices represented a Bear market, there would be no need to analyze the market further; a trader could become wealthy simply by buying stocks and holding them, only to dump them the moment a 20% decline came about.

The problem with rigid numerical definitions (e.g. a 20% decline) is that such rigidity does not allow for sufficient flexibility to avoid false alarms of a Bear market while simultaneously capturing every true Bear market with enough advance notice to allow for preparations (e.g. selling stocks).

Perhaps a better method of defining a Bear market is to simply state that it is a stock market in which the risk of owning stock is greater than the perceived reward.

The risk is tangible, and easily calculated; the reward is not. Stock prices can only fall to zero, at worst, so the risk of stock ownership is always known. The reward, on the other hand, is not known. Since stock prices have no upper limit, the potential reward of stock ownership cannot be defined, thus the potential reward is nothing more than the perception among traders of how high the stock price will go.

When stock prices are going up, the consensus among traders is generally that there is a reward. Traders may disagree on the amount of the potential reward, nevertheless they usually agree that there is a potential to profit from a continuation of the upward trend in prices.

If stock prices climb too far, too fast, the consensus can quickly shift. A perception that stock prices have reached a limit and have little potential upside can lead to a sell-off. Quite simply, the risk of loss (that stocks could go to zero) outweighs the perception of reward (that there is little chance of upside profits), stock prices can tumble until either the risk decreases, or the perceived reward increases, or both. When stock prices fall to a point at which an equilibrium is reached – when weighted risk equals the perceived reward – that’s when prices stop falling and begin to rise once more.

Sometimes, however, prices do not reach equilibrium, at least not for many weeks or months. In a cascading effect, falling stock prices sometimes do not represent bargains,

In the most extreme example possible, if stock prices were to fall to zero in a Bear market there would be no risk in stock ownership but there would be a perception of a potential reward. Therefore, individual stock prices rarely go all the way to zero, even when a the company that issued the stock has gone bankrupt, as long as a glimmer of hope remains, no matter how faint.

Stock indexes, such as the Dow Jones, Nasdaq or S&P 500 are even less likely to go to zero than the individual stocks they contain, for the simple reason that the closer the index gets to zero, the lower the risk. Thus, the tiniest glimmer of hope for potential reward can outweigh the risk of going to zero, especially as the index gets closer to zero. Equilibrium, even in the most severe of Bear markets, will be reached long before a major stock market index reaches zero.

Importance of Option Traders in Bear Markets

The reward for an option trader is often quite different than the reward for a stock owner. Option traders can and do earn profits when stock prices fall. The fact that it’s possible for some option traders to profit from a Bear market, however, is an oft overlooked useful bit of information that can be used to identify a Bear market.

If chosen carefully, the profitability of certain options can serve as an early-warning Bear-market alarm for all traders, stock market traders included. Unlike the profitability of short-selling stocks, which occurs whenever stock prices fall regardless of whether the price decline constitutes a Bear market, certain specific options only profit during a Bear market.

Since every option contract has a buyer and a seller, the profit of every option owner is always equal to the loss of the seller and vice versa. The options market is truly a zero-sum game. Options neither create nor destroy wealth, but merely move wealth from one place to another. That’s a stark contrast to the stock market, in which wealth can be created as well as destroyed.

It is important to note the inability of options to have any net effect on total wealth, because any analysis of options that only includes positions that experience an increase in wealth must exclude all positions that experience a decrease. The profits and losses of individual option positions are meaningless unless the net positions are known. Individual options themselves are therefore often poor indicators of the stock market, however, combinations of options and stock positions often provide very meaningful data.

For example, a trader may buy 100 shares of stock and sell 1 standard Call option. The stock price may subsequently rise above the strike price of the option and the Call option owner may exercise the option. In this case the Call buyer may experience a profit, since exercising the Call option allows him to buy 100 shares of stock at the strike price of the option and then sell those 100 shares of stock at a higher price on the open market.

The Call seller may also experience a profit, as long as the purchase price of the stock was less than the net sales price, when accounting for the Call option premium received. Both the Covered Call seller and the buyer of that particular Call option can each make a profit at the same time, on the same stock.

In order to use options to determine whether a Bear market is underway, it is necessary to study only those options which would give stock owners a perceived reward that is greater than the risk of loss. This narrows down the list of potentially hundreds of possible combinations that would serve as a Bear market indicator, to just two:

The presence of a Bear market, as outlined earlier, is evident whenever the risk of owning a stock is greater than the perceived reward potential. Also as previously outlined, not every decrease in stock prices results in a Bear market. Only those decreases in stock price that cause the risk of stock ownership to be greater than the perceived reward are bearish; declines that do not tip the risk/reward scale can often be healthy Bull market corrections.

A stock owner always has risk. The only way to eliminate risk completely is to sell the stock; and the only reason to eliminate risk completely is because of a perception that the potential reward is not worth the risk. As long as risk can be limited to a reasonable level by buying Put options, there is no immediate need to sell stocks that are owned.

Stock owners who buy Protective Puts can and do experience losses, but as long as Puts are cheap, the risk is relatively small. In a Bull market, when implied volatility is low, as is commonly indicated when the VIX is low (below 20), Puts are relatively inexpensive. It is unlikely if not impossible for a Bear market to begin while Put options are cheap – when the VIX is low.

No matter how deep a sell-off, no matter how severe a correction, as long as stock owners can limit risk with inexpensive Puts, the perceived reward of stock ownership will always be greater than the risk. A Bear market simply cannot take hold until the VIX is elevated, until Put premiums become so high that the risk of protecting stocks with Puts outweighs any potential perceived reward.

Even when option premiums rise, there is an alternative to stock owners. Rather than buy Puts for protection, they can sell Covered Calls against their existing stock positions. The higher the implied volatility (the higher the VIX) the higher the Call premiums; so the reward of stock ownership remains intact even during a decline in stock prices, thanks to the options market.

The only way the risk of stock ownership can become so great that it exceeds the perceived reward potential is for a stock owner to run out of suitable option alternatives. The stock owner can buy Protective Puts, and if that doesn’t offer enough reward for the risk, sell Covered Calls. If Covered Calls don’t offer enough reward for the risk, then there are very few suitable alternatives.

How much reward for the risk is acceptable? That’s certainly debatable. However, when there is zero reward for the risk, there is not really much left for debate. When a stock owner cannot limit risk to an acceptable level with at-the-money (ATM) Put options, or can’t create any reward at all selling at-the-money (ATM) Covered Call options, it’s time to sell the stock.

Sure, it’s possible the stock owner could use in-the-money (ITM) options and might be able to eke out a profit. But is it worth it? Buying ITM Protective Puts or selling ITM Covered Calls is a little like chasing a bus, and the profits, if there are any, are often not worth the effort, much less the risk of loss. That doesn’t mean all ITM options are bad choices; but when ITM options are the only ones a stock owner can use successfully, it might be better for a stock owner to just sell the stock and sit on the sidelines for a while.

Historical Success Identifying Bear Markets

The following chart shows the profitability of several common types of option strategies applied to the S&P 500 index as a whole. Above the yellow line, in the blue and green zones, stock owners who protect their positions by buying ATM Put options earn a profit. There’s no way a Bear market can begin if stock owners can buy Put options and still earn a profit; it’s simply not possible.

An expanded 10-year historical chart is now available.

Below the yellow line, in the yellow zone, stock owners may experience a loss if they protect their positions with Puts, however, stock owners who did not buy Puts can still earn a profit. Not every stock owner buys Puts for protection; some choose to trade without a safety net. Those traders will profit from rising stock prices, even when the increase is very small, since they are not spending anything on option premiums for protection. A Bear market is highly unlikely to begin when stock prices are still rising.

Below the orange line, in the orange zone, stock owners may experience losses, but not if they sold ATM Covered Calls against their existing stock positions. It is highly unlikely a Bear market could begin when stock prices fall, as long as it is possible for stock owners to continue to profit from their stocks, by selling Call options.

Below the red line, in the red zone, stock owners cannot experience a gain by buying ATM Put options or by selling ATM Covered Calls against their existing positions. Below the red line, the stock owner has run out of options… literally. The red line therefore defines the point, at any time, past or present, at which the risk of stock ownership outweighs the perceived reward.

A Bear market is almost a certainty below the red line, and almost certainly impossible above it. For historical perspective, the following chart shows the level of the S&P 500 relative to the red line. In other words, this chart shows how for the S&P would need to fall for a Bear market to begin (if a Bull market is underway) or how far the S&P would need to rise for a Bear market to end (if a Bear market is underway).

The chart below is formed by viewing the S&P 500 from the vantage point of the red line as depicted on the chart above. For the week ending September 20, 2014, the most recent date for which data was available, the red line in the chart above is located at the 1903 level for the S&P 500, so on the chart below the S&P is approximately 5.3% higher than the red line, at the 2010 level. 2010 (the current S&P level) = 1903 (the current red line level) + 5.3%.

For example, if the S&P 500 is 5% above a Bear market, a level of 2000 for the S&P would indicate that a decline of more than 5%, or 100 points, would likely cause a Bear market. A decline of 5% or less, 100 points or less, would be considered a Bull market correction. This gives traders an opportunity to place stop-loss orders in order to avoid losses caused by a Bear market.

The chart shows that Bear market alarms produced using the above methods are rare, yet the alarm never fails to sound when a Bear market is underway. No speculation, no comparison to disasters such as the Crash of ’29, just advance warning when it’s needed most.

A few areas of interest on the chart include:

Weekly 3-Step Options Analysis:

On the chart of “Stocks and Options at a Glance”, option strategies are broken down into 3 basic categories: A, B and C. Following is a detailed 3-step analysis of the performance of each of those categories.

STEP 1: Are the Bulls in Control of the Market?

The performance of Covered Calls and Naked Puts (Category A+ trades) reveals whether the Bulls are in control. The Covered Call/Naked Put Index (#CCNPI) measures the performance of these trades on the S&P 500 when opened at-the-money over several time frames.

Most important is the profitability of these trades opened 112 days prior to expiration, which balances sluggish responses of longer expirations with irrelevant noisy responses of shorter expirations.

Covered Call trading did not experience a single loss in 2013, and the streak endures so far in 2014, continuing a streak of nearly lossless trading extending all the way back to late 2011. That means the Bulls have been in control since late 2011 and remain in control here, nearly 3 full years later, in 2014.

As long as the S&P remains above 1903 over the upcoming week, Covered Call trading (and Naked Put trading) will remain profitable, indicating that the Bulls retain control of the longer-term trend. Below S&P 1903 this week, Covered Calls and Naked Puts will not be profitable, and since such trades only produce losses in a Bear market, it would suggest the Bears were in control.

The reasoning goes as follows:

• “If I can sell an at-the-money Covered Call or a Naked Put and make a profit, then prices have either been going up, or have not fallen significantly.” Either way, it’s a Bull market.

• “If I can’t collect enough of a premium on a Covered Call or Naked Put to earn a profit, it means prices are falling too fast. If implied volatility increases, as measured by indicators such as the VIX, the premiums I collect will increase as well. If the higher premiums are insufficient to offset my losses, the Bulls have lost control.” It’s a Bear market.

• “If stock prices have been falling long enough to have caused extremely high implied volatility, as measured by indicators such as the VIX, and I can collect enough of a premium on a Covered Call or Naked Put to earn a profit even when stock prices fall drastically, the Bears have lost control.” It’s probably very near the end of a Bear market.

STEP 2: How Strong are the Bulls?

The performance of Long Calls and Married Puts (Category B+ trades) reveals whether bullish traders’ confidence is strong or weak. The Long Call/Married Put Index (#LCMPI) measures the performance of these trades on the S&P 500 when opened at-the-money over several time frames.

Most important is the profitability of these trades opened 112 days prior to expiration which balances sluggish responses of longer expirations with irrelevant noisy responses of shorter expirations.