By Walter Kurtz

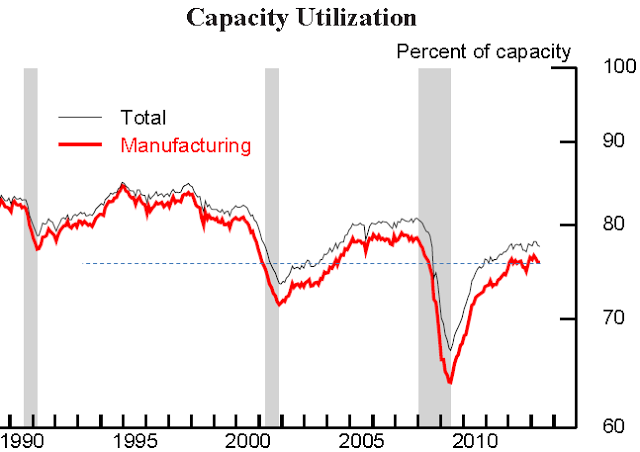

In another sign of recent weakness in the manufacturing sector, capacity utilization in the US has stalled, as demand remains soft. US industries are producing significantly below their capacity and “5.5 percentage points below long-run average” according to the Fed. We are certainly far under the 82-85% level at which economists believe that the traditional measures of inflation are expected to rise (see figure 1).

24/7 Wall St.: – … [US] manufacturing base still matters, as the United States remains one of the top exporters in the world. And a disturbing trend may be forming that signals some underlying weakness in the old core economy. This could be bad news for employment, growth, exports, revenue, capital spending and just about everything else.

Industrial production came in flat for the month of May rather than a 0.2% expected gain. The reading on capacity utilization posted an unexpected drop to 77.6%, versus a Bloomberg expectation for a 0.1% gain to 77.9%. To make matters worse, the 77.8% from April was revised to 77.7%. The peak cycle was 78.3% in March, which makes things look even worse.

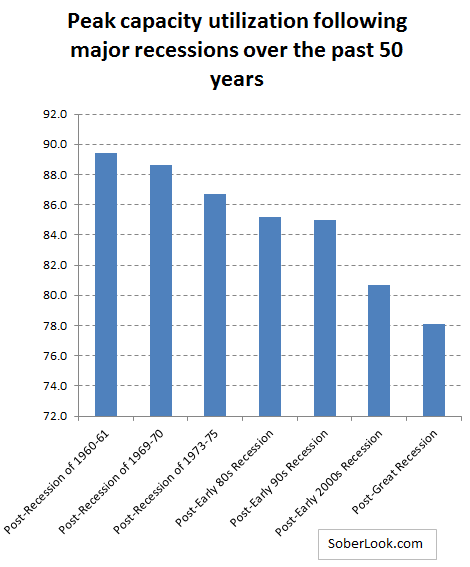

Moreover, the long-term trend in capacity utilization in the US shows a secular decline. After each major recession over the past 50 years, capacity utilization peaked at a lower level than after the previous recession (see figure 2). So far in the post-Great Recession recovery, this trend has not been violated, as the nation struggles from chronic excess capacity.

(Figure 1 – Capacity Utilization)

(Figure 2 – Peak Capacity Utilization)

No comments:

Post a Comment