By Jordan Roy-Byrne, CMT, Daily Commodities

Commodities are a very volatile asset class and unlike stocks, high prices will reduce demand while low prices will reduce production and supply. While buying breakouts and momentum in stocks often works well with the right risk controls, buying weakness rather than strength is more advisable in Commodities.

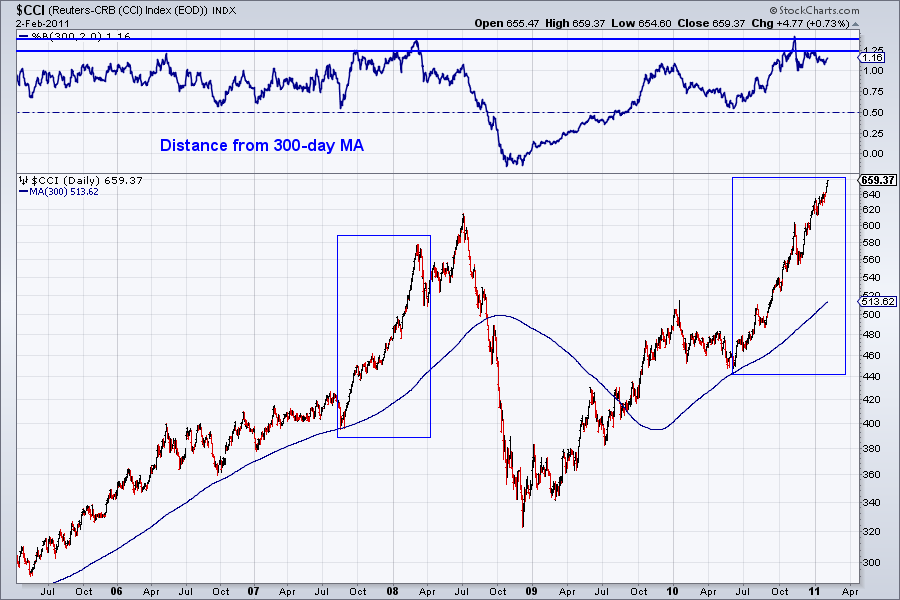

The continuous commodity index (CCI) recently hit an all-time high and has continued to make new highs. The energy and agriculture sectors have been red-hot. Two things concern us in regards to the CCI. First, the market has had a single 8% pullback in the last eight months. Other than that, no weakness for more than a few days at a time. Second, the market is trading well above the 300-day MA. At the top of the chart we show the market’s distance from its 300-day MA.

Also, quite a bit of retail money has suddenly flowed into commodity-related shares. The chart below (from sentimentrader.com) shows the assets in Rydex’ Energy Fund. About two months ago, assets in the fund were less than $50 Million. Now, the total is $152 Million.

The only aberration is the precious metals sector. We don’t show the chart but assets in that fund declined about 50% since the end of December. Moreover, we recently wrote about how the speculative money in the futures market remains heavily long all commodities (ex Gold & Silver).

We are in a long-term bull market and we believe commodities as an asset class will heat up in the coming years. That being said, commodities are very overbought here and the risk/reward for new longs is unfavorable. We see an intermediate top in the coming weeks or months. We’d advise lightening up on long positions and perhaps using stops to protect profits. This is a volatile asset class and if you exercise patience and use volatility to your advantage, you will likely find a few excellent long opportunities per year. This is not one of the times. [..]

No comments:

Post a Comment